Nordstrom 2009 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2009 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

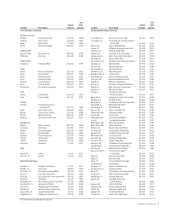

|

|

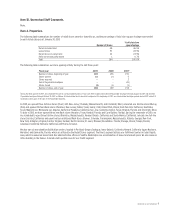

6

Item 1A. Risk Factors.

(Dollars in millions)

Our business faces many risks. We believe the risks described below outline the items of most concern to us. However, these are not the only risks we

face. Additional risks and uncertainties, not presently known to us or that we currently consider immaterial, may also impair our business operations.

DETERIORATION OF ECONOMIC CONDITIONS

The deterioration in economic conditions over the past two years has hurt our business in several ways. Rising unemployment, tightening of consumer

credit and the decline in the housing market in the United States have all contributed to a reduction in consumer spending. This has had a significant

negative impact on our revenues. We sell high-quality apparel, shoes, cosmetics and accessories, which many consumers consider to be discretionary

items. During economic downturns, fewer customers may shop in our stores and on our Web site, and those who do shop may limit the amount of their

purchases, all of which may lead to lower sales, higher markdowns and increased marketing and promotional spending in response to lower demand.

The deterioration of economic conditions has also adversely affected our credit customers’ payment patterns and delinquency rates, increasing our

bad debt expense. While some macroeconomic indicators suggest that a modest economic recovery has begun, key factors such as employment levels,

consumer credit and housing market conditions remain weak. A sluggish economic recovery or a renewed downturn could have a significant adverse

effect on our business.

ABILITY TO RESPOND TO THE BUSINESS ENVIRONMENT AND FASHION TRENDS

We strive to ensure the merchandise we offer remains current and compelling to our customers. We make decisions regarding inventory purchases well

in advance of the season in which it will be sold. Therefore, our ability to predict or respond to changes in fashion trends, consumer preferences and

spending patterns, and to match our merchandise levels and mix to sales trends and consumer tastes, significantly impacts our sales and operating

results. If we do not identify and respond to emerging trends in consumer spending and preferences quickly enough, we may be forced to sell our

merchandise at higher average markdown levels and lower average margins, which could harm our business. Conversely, if we fail to purchase enough

merchandise, we may lose opportunities for additional sales and damage our relationships with our customers.

CONSUMER CREDIT

Our credit card operations help drive sales in our stores, allow our stores to avoid third-party transaction fees and generate additional revenues by

extending credit. Our credit card revenues and profitability are subject in large part to economic and market conditions that are beyond our control,

including, but not limited to, interest rates, consumer credit availability, consumer debt levels, unemployment trends and other matters. Increases in

unemployment have corresponded with rising credit card delinquencies and write-offs, which may continue in the future. Further, these economic

conditions could impair our ability to assess the creditworthiness of our customers if the criteria and/or models we use to underwrite and manage our

customers become less predictive of future losses, which could cause our losses to rise and have a negative impact on our results of operations.

REGULATORY ENVIRONMENT AND FINANCIAL SYSTEM REFORMS

Current economic conditions, particularly in the financial markets, have resulted in increased legislative and regulatory actions. The Credit Card

Accountability, Responsibility and Disclosure Act of 2009 (the “Credit CARD Act”) included new rules and restrictions on credit card pricing, finance

charges and fees, customer billing practices and payment application. These provisions are likely to affect our credit business practices and could

have a negative impact on our revenues and profitability.

In addition, Congress and the Obama Administration are currently considering various proposals for reform of the financial system. Proposed reforms

include the elimination of the thrift charter and all retailer-owned bank charters, creation of a new federal agency to supervise and enforce consumer

lending laws and regulations, and expanded state authority over consumer lending. The final details of financial system reform legislation, if any, are

highly uncertain at this time. Depending on the nature and extent of any reforms, our credit business could be significantly adversely affected.

LEADERSHIP DEVELOPMENT AND SUCCESSION PLANNING

The training and development of our future leaders is important to our long-term growth. If we do not effectively implement our strategic and business

planning processes to attract, retain, train and develop future leaders, our long-term growth may suffer. We rely on the experience of our senior

management, who have specific knowledge relating to us and our industry that is difficult to replace. If unexpected leadership turnover occurs without

adequate succession plans, the loss of the services of any of these individuals, or any negative perceptions of our business as a result of those losses,

could damage our brand image and our business.

INFORMATION SECURITY AND PRIVACY

The protection of our customer, employee and company data is important to us. The regulatory environment surrounding information security and

privacy is increasingly demanding, with new and constantly changing requirements across our business units. In addition, our customers have a high

expectation that we will adequately protect their personal information. A significant breach of customer, employee or company data could damage our

reputation and result in lost sales, fines and lawsuits. In addition, a security breach could require that we expend significant additional resources

related to our information security systems and could result in disruption of our operations, particularly our online sales operations.

BRAND AND REPUTATION

We have a well-recognized brand that many consumers believe offers a high level of customer service and quality merchandise. Any significant damage

to our brand or reputation could negatively impact sales, reduce employee morale and productivity, and diminish customer trust, any of which would

harm our business.