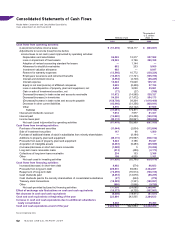

Mazda 2009 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2009 Mazda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

Review of OperationsMessages from Management Mazda’s Environmental and

Safety Technology

Corporate Information Financial Section

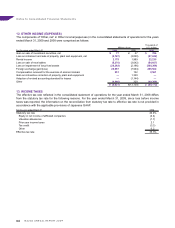

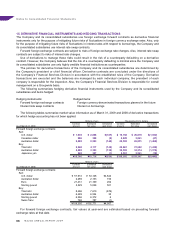

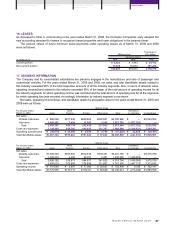

In addition, adjustments for the following six items specified in PITF No. 18 from IFRS or U.S. GAAP to Japanese

GAAP should be made as necessary in the consolidation process unless the impact is immaterial:

(a) If the amortization of goodwill is not implemented, adjustments should be made to amortize it;

(b) If actuarial gains and losses of defined-benefit retirement plans are recognized outside profit and loss, adjustments

should be made to recognize them in the income statement;

(c) If expenditures for research and development activities are capitalized, adjustments should be made to

immediately expense them;

(d) If fair value measurement of investment properties is adopted or revaluation of property, plant and equipment and

intangible assets is adopted, adjustments should be made for recording the depreciation expense calculated by

applying the regular depreciation method;

(e) If retrospective treatment of a change in accounting policies is adopted, adjustments should be made to recognize

the amount as profit and loss in the current fiscal year; and

(f ) If minority interests are included in the current net income, adjustments should be made to exclude the minority

interests from net income.

As a transition requirement of PITF No. 18, the balance of consolidated retained earnings as of April 1, 2008 was

reduced by ¥1,554 million ($15,857 thousand). Also, in the consolidated statement of operations for the year ended

March 31, 2009, while the effect of adopting PITF No. 18 on operating loss was immaterial, loss before income taxes

was increased by ¥3,119 million ($31,827 thousand).

Also, in connection with adopting PITF No. 18, incentive expenses of consolidated foreign subsidiaries that were

recognized in selling, general and administrative expenses in the prior periods are now recognized as a reduction to

net sales. For the year ended March 31, 2009, such incentive expenses amounted to ¥146,697 million ($1,496,908

thousand), and the effects of this change on the consolidated statement of operations for the year ended March 31,

2009 were to decrease net sales, gross profit on sales, and selling, general and administrative expenses each by the

same amount.

Also, the effects of adopting PITF No. 18 on segment information are discussed in the applicable section of the

notes to the consolidated financial statements.

Accounting standard for measurement of inventories

Commencing in the year ended March 31, 2009, the Domestic Companies adopted ASBJ Statement No. 9,

Accounting Standards for Measurement of Inventories, issued by the ASBJ on July 5, 2006. As permitted under the

superseded accounting standard, the Domestic Companies previously stated inventories at cost. The new accounting

standard requires that inventories held for sale in the ordinary course of business be measured at the lower of cost

or net realizable value, which is defined as selling price less estimated additional manufacturing costs and estimated

direct selling expenses.

The effects of adopting the new standard on the consolidated statement of operations for the year ended March

31, 2009 were to increase operating loss and loss before income taxes each by ¥2,461 million ($25,112 thousand).

Also, the effects of adopting the new standard on segment information are discussed in the applicable section of

the notes to the consolidated financial statements.

Change in accounting for materials sold to and purchased back from suppliers after fabrication

Prior to the year ended March 31, 2009, in the consolidated statements of operations, the Company accounted for

materials sold to suppliers for the purpose of purchasing back from them after fabrication in such a manner that the

transactions were recognized in both net sales and cost of sales, as the Company was emphasizing the contractual

condition that the ownership title to the materials transfers through the transactions. Commencing in the year ended

March 31, 2009, the Company changed accounting for these transactions to exclude the amounts from both net

sales and cost of sales, as the Company now emphasizes the substance of the transactions that the materials are

purchased back after fabrication.

The effects of this accounting change on the consolidated statement of operations for the year ended March 31,

2009 were to decrease net sales and cost of sales each by ¥152,097 million ($1,552,010 thousand) with no effects on

operating loss and loss before income taxes.

Also, the effects of this accounting change on segment information are discussed in the applicable section of the

notes to the consolidated financial statements.

57