JetBlue Airlines 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

instruments entirely as debt. FSP APB 14-1 is effective for financial statements issued for fiscal years

beginning after December 15, 2008 and interim periods within those fiscal years. We have considered the

impact of our adoption of FSP APB 14-1 on our consolidated financial statements, and we estimate that our

$250 million aggregate principal amount of 33⁄4% convertible unsecured debentures due 2035 will have an

approximate initial measurement of a $200 million liability component and a $50 million equity component.

We estimate we would have had an additional $10 million in interest expense in each of the years ended

December 31, 2006, 2007, and 2008.

In March 2008, the FASB issued SFAS 161, Disclosures about Derivative Instruments and Hedging

Activities, an amendment of FASB Statement No. 133, which enhances the disclosure requirements related to

derivative instruments and hedging activity to improve the transparency of financial reporting, and is effective

for fiscal years and interim periods beginning after November 15, 2008. We are currently evaluating the

impact of adoption of SFAS 161.

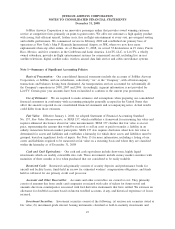

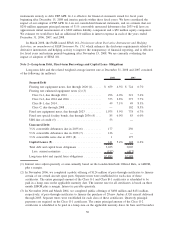

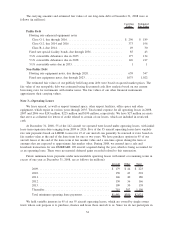

Note 2—Long-term Debt, Short-term Borrowings and Capital Lease Obligations

Long-term debt and the related weighted average interest rate at December 31, 2008 and 2007 consisted

of the following (in millions):

2008 2007

Secured Debt

Floating rate equipment notes, due through 2020 (1)...... $ 659 4.5% $ 724 6.7%

Floating rate enhanced equipment notes (2) (3)

Class G-1, due through 2016 ..................... 296 4.0% 321 5.6%

Class G-2, due 2014 and 2016 .................... 373 2.8% 373 5.7%

Class B-1, due 2014............................ 49 7.1% 49 8.3%

Class C, due through 2008 ....................... — 102 8.5%

Fixed rate equipment notes, due through 2023 .......... 1,075 5.9% 778 6.7%

Fixed rate special facility bonds, due through 2036 (4) .... 85 6.0% 85 6.0%

UBS line of credit (5) ............................ 53 —

Unsecured Debt

33⁄4% convertible debentures due in 2035 (6) ........... 177 250

51⁄2% convertible debentures due in 2038 (7) ........... 126 —

31⁄2% convertible notes due in 2033 (8) . . . ............ 1 175

Capital Leases (9) .............................. 141 5.4% 148 6.2%

Total debt and capital lease obligations . . . ............ 3,035 3,005

Less: current maturities ......................... (152) (417)

Long-term debt and capital lease obligations ........... $2,883 $2,588

(1) Interest rates adjust quarterly or semi-annually based on the London Interbank Offered Rate, or LIBOR,

plus a margin.

(2) In November 2006, we completed a public offering of $124 million of pass-through certificates to finance

certain of our owned aircraft spare parts. Separate trusts were established for each class of these

certificates. The entire principal amount of the Class G-1 and Class B-1 certificates is scheduled to be

paid in a lump sum on the applicable maturity date. The interest rate for all certificates is based on three

month LIBOR plus a margin. Interest is payable quarterly.

(3) In November 2004 and March 2004, we completed public offerings of $498 million and $431 million,

respectively, of pass-through certificates to finance the purchase of 28 new Airbus A320 aircraft delivered

through 2005. Separate trusts were established for each class of these certificates. Quarterly principal

payments are required on the Class G-1 certificates. The entire principal amount of the Class G-2

certificates is scheduled to be paid in a lump sum on the applicable maturity dates. In June and November

50