JCPenney 2002 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2002 JCPenney annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48

|

|

2002 annual report J. C. Penney Company, Inc. 37

Notes to the Consolidated Financial Statements

Management’s assessment is that the character and nature of

future taxable income may not allow the Company to realize cer-

tain tax benefits of state net operating losses (NOLs) within the

prescribed carryforward period. Accordingly, a valuation allowance

has been established for the amount of deferred tax assets gener-

ated by state NOLs which may not be realized.

U.S. income and foreign withholding taxes were not provided

on certain unremitted earnings of international affiliates that the

Company considers to be permanent investments.

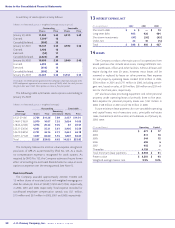

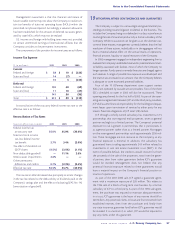

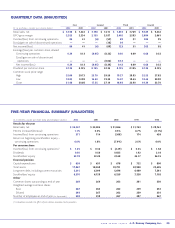

The components of the provision for income taxes are as follows:

Income Tax Expense

($ in millions) 2002 2001 2000

Current

Federal and foreign $58$ 10 $ (223)

State and local 14 (7) —

72 3 (223)

Deferred

Federal and foreign 130 68 (68)

State and local 11 18 (27)

141 86 (95)

Tot al $ 213 $ 89 $ (318)

A reconciliation of the statutory federal income tax rate to the

effective rate is as follows:

Reconciliation of Tax Rates

(percent of pre-tax income) 2002 2001 2000

Federal income tax

at statutory rate 35.0% 35.0% (35.0%)

State and local income

tax, less federal income

tax benefit 2.7% 3.4% (2.0%)

Tax effect of dividends on

ESOP shares (4.5%) (3.5%) (1.1%)

Non-deductible goodwill —11.1% 2.6%

Mexico asset impairments 2.6% ——

Other permanent

differences and credits 0.7% (2.3%) (0.4%)

Effective tax rate 36.5% 43.7% (35.9%)

The tax rate in 2002 decreased due principally to recent changes

in the tax law related to the deductibility of dividends paid to the

Company’s savings plan and the effects of adopting SFAS No. 142

(amortization of goodwill).

19 LITIGATION, OTHER CONTINGENCIES AND GUARANTEES

The Company is subject to various legal and governmental pro-

ceedings involving routine litigation incidental to the business. This

includes the Company being a co-defendant in a class action lawsuit

involving the sale of insurance products by a former subsidiary of the

Company. While no assurance can be given as to the ultimate out-

come of these matters, management currently believes that the final

resolution of these actions, individually or in the aggregate, will not

have a material adverse effect on the annual results of operations,

financial position, liquidity or capital resources of the Company.

In 2002, management engaged an independent engineering firm to

evaluate the Company’s established reserves for potential environmen-

tal liability associated with facilities, most of which the Company no

longer operates. Funds spent to remedy these sites are charged against

such reserves. A range of possible loss exposure was developed and

the reserve was increased to an amount that the Company believes

is adequate to cover estimated potential liabilities.

Four of the 10 JCPenney department store support centers

(SSCs) are operated by outside service providers. Two of the three

SSCs scheduled to open in 2003 will also be outsourced. These

openings are planned for the first half of 2003. As part of the oper-

ating service agreement between JCP and the third party providers,

JCP shall assume financial responsibility for the building and equip-

ment leases upon termination of services by either party for any

reason. Potential obligations of JCP total $185 million.

JCP, through a wholly owned subsidiary, has investments in 15

partnerships that own regional mall properties, seven as general

partner and eight as a limited partner. The Company’s potential

exposure to risk is greater in partnerships that it participates in

as a general partner rather than as a limited partner. Mortgages

on the seven general partnerships total approximately $350 mil-

lion. These mortgages are non-recourse to the Company, so any

financial exposure is minimal. In addition, the subsidiary has

guaranteed loans totaling approximately $43 million related to

investments in one real estate investment trust (REIT). In the

event of possible default, the creditors would recover first from

the proceeds of the sale of the properties, next from the gener-

al partner, then from other guarantors before JCP’s guarantee

would be invoked. Management does not believe that any

potential financial exposure related to these guarantees would

have a material impact on the Company’s financial position or

results of operations.

As part of the 2001 DMS sale, JCP signed a guarantee agree-

ment with a maximum exposure of $20 million. This relates to

the 1994 sale of a block of long-term care business by a former

subsidiary of JCP to a third party. As part of the 1994 sale agree-

ment, the purchaser was required to maintain adequate reserves

in a trust. JCP’s guarantee is the lesser of any reserve shortfall or

$20 million. Any potential claims or losses are first recovered from

established reserves, then from the purchaser and finally from

any state insurance guarantee fund before JCP’s guarantee would

be invoked. It is uncertain if, or when, JCP would be required to

pay any claims under this guarantee.