JCPenney 2002 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2002 JCPenney annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

J. C. Penney Company, Inc. 2002 annual report14

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Merchandise Inventory

Total LIFO inventory was $4,945 million in 2002 compared with

$4,930 million in 2001. FIFO merchandise inventory for

Department Stores and Catalog was $3,030 million at the end of

2002, an increase from last year of 1.7%. While inventories are

higher than last year’s levels, they are well-balanced and focused

on current and future seasons. Inventory turns for Department

Stores and Catalog have improved from 3.0 to 3.4 over the past

three years. Eckerd FIFO merchandise inventory was $2,318 million

at the end of 2002, a decrease of 0.5% from the prior year. Major

improvements have been made in the management of drugstore

inventory. Over the last three years, inventory turns have

improved from 4.0 to 4.8.

Debt-to-Capital Ratio

2002 2001 2000

Debt-to-capital 30.2% 34.9% 43.2%

Debt-to-capital, including

leases and securitization

of receivables 50.7% 53.5% 56.8%

The Company manages its capital structure to ensure financial

flexibility and access to capital, at a competitive cost, necessary to

accomplish its business strategies. Historically, the Company has

targeted a debt-to-capital ratio in the 50% to 55% range, including

off-balance sheet debt. Over the remaining turnaround time

frame of 2003-2005, the Company currently expects that its debt-

to-capital ratio will remain in this target range.

The Company manages its financial position by considering all

on- and off-balance sheet debt, including operating leases and

receivable securitizations. Management believes this view is the

most realistic depiction of financial leverage. The debt-to-capital

ratio is also shown as calculated in the more traditional manner of

on-balance sheet debt for comparison purposes.

Total debt, net of short-term investments, but including the

present value of operating leases and securitized receivables, was

$6,541 million, $7,038 million and $8,232 million at the end of

2002, 2001 and 2000, respectively. The $1.7 billion decline in total

debt and the resulting improvement in the debt-to-capital ratio

over this period was achieved from the positive free cash flow

generated and the sale of DMS. See page 41 for more discussion.

During 2002, approximately $920 million principal amount of

notes matured and was paid. Also in 2002, JCP exchanged three

existing debt issues totaling $227.2 million principal amount for

new 9.0% Notes Due 2012 with a principal amount of $230.2 mil-

lion as discussed on page 12. The transaction effectively extended

the maturity on amounts represented by the exchanged notes

and strengthened the Company’s liquidity as the turnaround of

the businesses continues to be executed.

During 2001, $250 million principal amount of notes matured

and was paid. JCP issued $650 million of 5% convertible subordi-

nated notes in a private placement in October 2001.

Key Business Risks

The Company believes that its key business risk is that the

five-year turnaround plan, which is entering its third year, will

progress on target and will be achieved. Company manage-

ment has established the following business strategies to

ensure that the turnaround of its businesses is successful and

progresses on target:

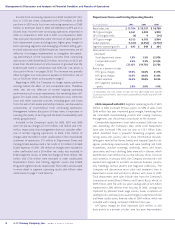

Contractual Obligations and Commitments

Aggregated information about the Company’s contractual obligations and commitments as of January 25, 2003, are presented in the

following tables. (This information is also disclosed in other parts of this Annual Report.)

Contractual Obligations

After

($ in millions) Total 2003 2004 2005 2006 2007 5 years

Long-term debt $ 5,169 $ 394 $ 238 $ 624 $ 187 $ 554 $ 3,172

Short-term debt 13 13—————

Capital lease obligations 51 17 16 12 4 2 —

Operating leases 6,903 671 611 544 494 455 4,128

Tot al $ 12,136 $ 1,095 $ 865 $ 1,180 $ 685 $ 1,011 $ 7,300

Commitment Expiration per Period

After

($ in millions) Total 2003 2004 2005 2006 2007 5 years

Standby and import letters of credit(1) $206$206$—$—$—$—$—

Surety bonds(2) 9898—————

Guarantees(3) 277 26 54 29 40 27 101

Tot al $ 581 $ 330 $ 54 $ 29 $ 40 $ 27 $ 101

(1) Standby letters of credit ($156 million at year-end) are issued as collateral to a third-party administrator for self-insured workers’ compensation and general liability claims.

(2) Surety bonds are primarily for previously incurred and expensed obligations related to workers’ compensation and general liability claims.

(3) Includes guarantees of $185 million on building and equipment leases operated by third parties, $43 million on loans related to a real estate investment trust, $29 million on

certain leases related to stores that were sold in 1997, of which $22 million is recorded in other liabilities and $20 million related to a third party reinsurance guarantee.