Holiday Inn 2011 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2011 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

40 IHG Annual Review and Summary Financial Statement 2011

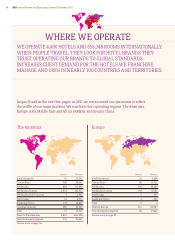

GROUP RESULTS

Revenue increased by 8.6% to $1,768m

and operating profit before exceptional

items increased by 25.9% to $559m

during the 12 months ended

31 December 2011.

The 2011 results reflect continued

revenue per available room (RevPAR)

growth, with an overall RevPAR increase

of 6.2%, including a 2.5% increase in

average daily rate. The results also

benefit from overall system size growth

of 1.7% year on year to 658,348 rooms.

RevPar growth remained strong

throughout the year across the Group

although there was some deterioration

in Europe in the fourth quarter reflecting

macroeconomic conditions.

Central overheads increased from $139m

in 2010 to $147m in 2011, driven by

increased investment to support growth

in the business, offsetting non-recurring

bonus costs.

As a result of growth in the business,

together with strong cost control,

operating profit margin was 40.6%, up

4.9 percentage points on 2010, after

adjusting for owned and leased hotels,

The Americas and Europe managed

leases and significant liquidated damages

received in 2011. This growth approximates

to one percentage point after adjusting

for a number of one-off benefits.

During 2011, the IHG global system

increased by 43 hotels (11,187 rooms).

Openings of 241 hotels (44,265 rooms)

were driven by continued expansion in

the US, in particular within the Holiday

Inn brand family and Greater China.

These openings offset the removal of

198 hotels (33,078 rooms). Removals

in the US included 43 hotels (6,994 rooms)

which were removed from the system

as part of the renegotiation of the

management contract with Hospitality

Properties Trust, a major US owner

group. Other openings included the

Venetian and Palazzo resorts, under an

InterContinental Alliance relationship,

(6,986 rooms, included in franchised) as

well as 25 hotels (4,796 rooms) managed

on US army bases.

At the end of 2011, the pipeline totalled

1,144 hotels (180,484 rooms). The

continued global demand for IHG brands

is demonstrated by over 50% of pipeline

rooms being outside of The Americas

region, including 28% in Greater China.

Signings of 356 hotels (55,424 rooms)

represented an increase in the number

of hotels signed from 2010 levels (319

hotels). Momentum for the Hotel Indigo

brand continued into 2011 with 19 signings,

including entry into the Russian market,

as well as the first Hotel Indigo resort in

Phuket, Thailand.

During 2011, the opening of 44,265 rooms

contributed to a net pipeline decline of

24,375 rooms. Active management out

of the pipeline of deals that have become

dormant or no longer viable, resulted in

a further reduction of 35,534 rooms.

AMERICAS RESULTS

Revenue and operating profit before

exceptional items increased by $23m

(2.9%) to $830m and by $82m (22.2%)

to $451m respectively.

Franchised revenue increased by $37m

(8.0%) to $502m. Royalties growth of

8.5% was driven by RevPAR gains across

the estate of 7.2%, including 7.9% for

Holiday Inn Express, and was further

boosted by continued improvement in

the royalty rate achieved. Operating

profit increased by $39m (9.9%) to $431m

also benefiting from lower bad debt

experience.

Managed revenue increased by $5m

(4.2%) to $124m and operating profit

increased by $31m (147.6%) to $52m.

Excluding properties structured for legal

reasons as operating leases but with the

same characteristics as management

contracts, as well as the benefit of a

$10m liquidated damages receipt in 2011

and a $10m year-on-year benefit from

the conclusion of a specific guarantee

negotiation relating to one hotel, revenue

grew by $7m. Growth was driven by a

RevPAR increase of 8.8% across the

estate. Although year-end system size

was 6.0% lower than at the end of 2010,

due to the phasing of removals towards

the end of the year, rooms available

during the year actually grew by 4.5%.

Operating profit grew by $11m on the

same basis, also benefiting from

increased joint venture distributions.

Owned and leased revenue declined by

$19m (8.5%) and operating profit grew

by $4m (30.8%) to $17m. Excluding the

year-on-year impact of hotel disposals,

owned and leased revenue grew by

$8m (4.2%) and operating profit by

$7m (77.8%) reflecting RevPAR growth

of 10.3%, including 11.2% at the

InterContinental New York Barclay.

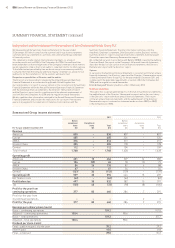

SUMMARY FINANCIAL STATEMENT

We delivered a 26% growth in operating profit before exceptional items and a five percentage

point increase in operating margin over last year. These results were driven by the strength of our

preferred brands, underpinned by our global systems and scale, resulting in 6.2% RevPAR growth,

beating the industry in key markets such as the US and Greater China, and a 2% increase in hotel

room count.