Cisco 2002 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2002 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

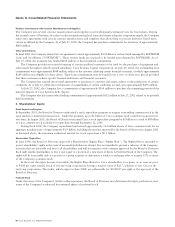

Notes to Consolidated Financial Statements

30 Cisco Systems, Inc. 2002 Annual Report

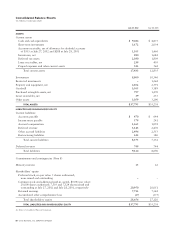

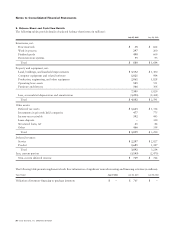

The Company makes certain sales to two-tier distribution channels. These distributors are given privileges to return a portion of

inventory, receive credits for changes in selling prices, and participate in various cooperative marketing programs. The Company

recognizes revenue to two-tier distributors based on information provided by its distributors and also maintains accruals and

allowances for all cooperative marketing and other programs. The Company accrues for warranty costs, sales returns, and other

allowances based on its historical experience.

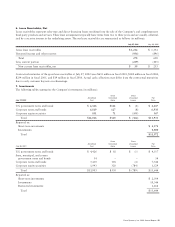

Lease Receivables The Company provides a variety of lease financing services to its customers to build, maintain, and upgrade their

networks. Lease receivables primarily represent the principal balance remaining in sales-type and direct-financing leases under these

programs, net of reserves. These leases typically have two- to three-year terms and are usually collateralized by a security interest in

the underlying assets.

Advertising Costs The Company expenses all advertising costs as incurred.

Software Development Costs Software development costs required to be capitalized pursuant to Statement of Financial Accounting

Standards No. 86, “Accounting for the Costs of Computer Software to Be Sold, Leased, or Otherwise Marketed,” have not been

material to date. Software development costs for internal use required to be capitalized pursuant to Statement of Position No. 98-1,

“Accounting for the Costs of Computer Software Developed or Obtained for Internal Use,” have also not been material to date.

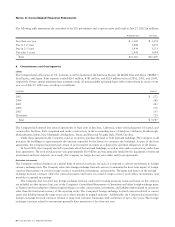

Depreciation and Amortization Property and equipment are stated at cost less accumulated depreciation and amortization. Depreciation

and amortization are computed using the straight-line method over the estimated useful lives of the assets. Estimated useful lives of

25 years are used for buildings. Estimated useful lives of 30 to 36 months are used for computer equipment and related software and

5 years for furniture and fixtures. Estimated useful lives of up to five years are used for production, engineering, and other equipment.

Depreciation of operating lease assets is computed based on the respective lease terms, which range up to three years. Depreciation

and amortization of leasehold improvements are computed using the shorter of the remaining lease terms or five years.

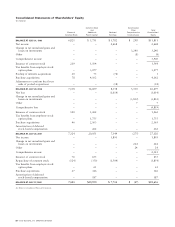

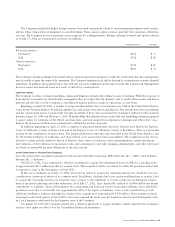

Goodwill and Purchased Intangible Assets In July 2001, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial

Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (“SFAS 142”). SFAS 142 requires goodwill to be tested

for impairment on an annual basis and between annual tests in certain circumstances, and written down when impaired, rather than

being amortized as previous accounting standards required. Furthermore, SFAS 142 requires purchased intangible assets other

than goodwill to be amortized over their useful lives unless these lives are determined to be indefinite.

SFAS 142 is effective for fiscal years beginning after December 15, 2001; however, the Company elected to early-adopt the

accounting standard effective the beginning of fiscal 2002. In accordance with SFAS 142, the Company ceased amortizing goodwill

totaling $3.2 billion as of the beginning of fiscal 2002, including $55 million of acquired workforce intangible previously classified

as purchased intangible assets, net of related deferred tax liabilities. Based on the impairment tests performed, there was no

impairment of goodwill in fiscal 2002. There can be no assurance that future goodwill impairment tests will not result in a charge

to earnings.

Purchased intangible assets are carried at cost less accumulated amortization. Amortization is computed over the estimated

useful lives of the respective assets, generally two to five years.

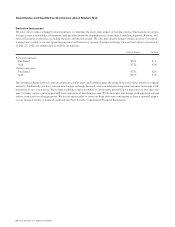

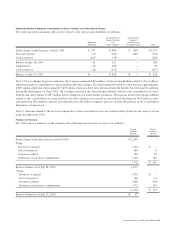

The following table presents the impact of SFAS 142 on net income (loss) and net income (loss) per share had the accounting

standard been in effect for fiscal 2001 and 2000 (in millions, except per-share amounts):

Years Ended July 27, 2002 July 28, 2001 July 29, 2000

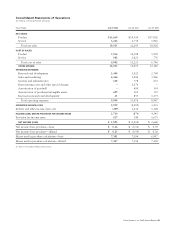

Net income (loss)—as reported $1,893 $ (1,014) $ 2,668

Adjustments:

Amortization of goodwill –690 154

Amortization of acquired workforce intangible previously

classified as purchased intangible assets –13 5

Income tax effect –(102) (21)

Net adjustments –601 138

Net income (loss)—adjusted $1,893 $ (413) $ 2,806

Basic net income (loss) per share—as reported $0.26 $ (0.14) $ 0.39

Basic net income (loss) per share—adjusted $0.26 $ (0.06) $ 0.41

Diluted net income (loss) per share—as reported $0.25 $ (0.14) $ 0.36

Diluted net income (loss) per share—adjusted $0.25 $ (0.06) $ 0.38