Cisco 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

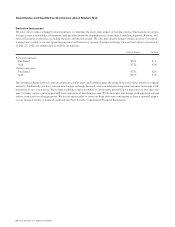

Management’s Discussion and Analysis of Financial Condition and Results of Operations

18 Cisco Systems, Inc. 2002 Annual Report

In the third quarter of fiscal 2001, we announced a restructuring program to prioritize our initiatives around a focus on profit

contribution, high-growth areas of our business, reduction of expenses, and improved efficiency. This restructuring program

included a worldwide workforce reduction, consolidation of excess facilities, and restructuring of certain business functions. For

additional information regarding the restructuring program, see Note 4 to the Consolidated Financial Statements. During the

third quarter of fiscal 2002, we increased the restructuring liabilities related to the consolidation of excess facilities and other

charges by $93 million due to changes in real estate market conditions. The increase in the restructuring liabilities related to the

consolidation of excess facilities and other charges was recorded as R&D ($39 million), sales and marketing ($42 million), and

G&A ($8 million) expenses and cost of sales ($4 million) in the Consolidated Statements of Operations.

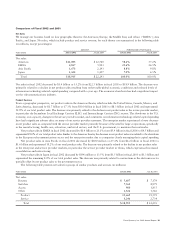

R&D, sales and marketing, and G&A expenses decreased in absolute dollars from the prior fiscal year primarily due to the

impact of the restructuring program and cost control measures to contain hiring and to reduce discretionary spending. Total R&D,

sales and marketing, and G&A expenses in the fourth quarter of fiscal 2002 decreased by approximately $600 million compared

with the quarter prior to the restructuring charge.

R&D expenses in fiscal 2002 were $3.4 billion, compared with $3.9 billion in fiscal 2001, a decrease of $474 million or 12.1%.

A significant portion of the decrease in R&D expenses was due to lower expenditures on prototypes, lower depreciation on lab

equipment, and reduced discretionary spending. We have continued to invest in R&D efforts in a wide variety of areas such as data,

voice, and video over IP; advanced access and aggregation technologies such as cable, wireless, and other broadband technologies;

advanced enterprise switching; optical transport; storage networking; content networking; security; network management; and

advanced core and edge routing technologies; among others. We have also continued to purchase or license technology in order

to bring a broad range of products to market in a timely fashion. If we believe that we are unable to enter a particular market in a

timely manner with internally developed products, we may license technology from other businesses or acquire businesses as an

alternative to internal R&D. All of our R&D costs have been expensed as incurred.

Sales and marketing expenses in fiscal 2002 were $4.3 billion, compared with $5.3 billion in fiscal 2001, a decrease of

$1.0 billion or 19.5%. The decrease in sales and marketing expenses was primarily due to a decrease in the size of our sales force

and marketing organization, reduced marketing and advertising investments, and reduced general promotional and marketing

program expenses.

G&A expenses in fiscal 2002 were $618 million, compared with $778 million in fiscal 2001, a decrease of $160 million or

20.6%. The decrease in G&A expenses was primarily related to the reductions in investments in infrastructure, personnel in support

and administrative functions, and discretionary spending.

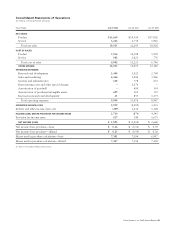

Amortization of Goodwill

We elected to early-adopt Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (“SFAS 142”),

effective the beginning of fiscal 2002. SFAS 142 requires goodwill to be tested for impairment on an annual basis and between

annual tests in certain circumstances, and written down when impaired, rather than amortized as previous accounting standards

required. In accordance with SFAS 142, we ceased amortizing goodwill. Based on the impairment tests performed, there was no

impairment of goodwill in fiscal 2002. There can be no assurance that future goodwill impairment tests will not result in a charge

to earnings. For additional information regarding SFAS 142, see Note 2 to the Consolidated Financial Statements.

Amortization of Purchased Intangible Assets

Amortization of purchased intangible assets included in operating expenses was $699 million in fiscal 2002, compared with

$365 million in fiscal 2001. The increase in the amortization of purchased intangible assets was primarily related to additional

amortization from recent acquisitions, accelerated amortization for certain technology and patent intangibles due to a reduction in

their estimated useful lives, and a write down of certain technology and patent intangibles. This write down totaled $159 million

and was due to the continued downturn in the optical market primarily related to the reduced demand for long haul products,

resulting in a significant adverse impact on the expected future cash flows of these purchased intangible assets. For additional

information regarding purchased intangible assets, see Note 3 to the Consolidated Financial Statements.

In-Process Research and Development

The amount expensed to in-process research and development (“in-process R&D”) was related to our purchase acquisitions and was

expensed upon acquisition because technological feasibility had not been established and no future alternative uses existed (see Note 3

to the Consolidated Financial Statements). The fair value of the existing purchased technology and patents, as well as the technology

under development, was determined using the income approach, which discounts expected future cash flows to present value.

The discount rates used in the present value calculations were typically derived from a weighted-average cost of capital analysis

and venture capital surveys, adjusted upward to reflect additional risks inherent in the development life cycle. We consider the pricing

model for products related to these acquisitions to be standard within the high-technology communications equipment industry.

However, we do not expect to achieve a material amount of expense reductions as a result of integrating the acquired in-process

technology. Therefore, the valuation assumptions do not include significant anticipated cost savings.