CarMax 2004 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2004 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52

|

|

44

CARMAX

2004

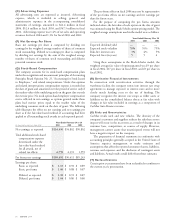

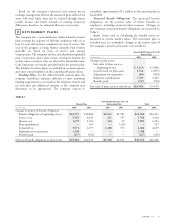

CONTINGENT LIABILITIES

(A) Litigation

In the normal course of business, the company is involved in

various legal proceedings. Based upon the company’s evaluation

of the information presently available, management believes

that the ultimate resolution of any such proceedings will not

have a material adverse effect on the company’s financial

position, liquidity, or results of operations.

(B) Other Matters

In accordance with the terms of real estate lease agreements, the

company generally agrees to indemnify the lessor from certain

liabilities arising as a result of the use of the leased premises,

including environmental liabilities and repairs to leased

property upon termination of the lease. Additionally, in

accordance with the terms of agreements entered into for the

sale of our properties, the company generally agrees to

indemnify the buyer from certain liabilities and costs arising

subsequent to the date of the sale, including environmental

liabilities and liabilities resulting from the breach of

representations or warranties made in accordance with the

agreements. The company does not have any known material

environmental commitments, contingencies, or other

indemnification issues arising from these arrangements.

As part of its customer service strategy, the company

guarantees the vehicles it sells with a 30-day limited warranty. A

vehicle in need of repair within 30 days of the customer’s

purchase will be repaired free of charge. As a result of this

guarantee, each vehicle sold has an implied liability associated

with it. As such, the company records a provision for repairs

during the guarantee period for each vehicle sold based on

historical trends. The liability for this guarantee was $1.4 million

at February 29, 2004, and $1.3 million at February 28, 2003,

and is included in accrued expenses and other current liabilities

in the consolidated balance sheets.

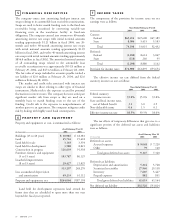

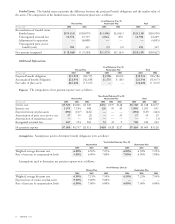

RECENT ACCOUNTING

PRONOUNCEMENTS

In May 2003, the FASB issued SFAS No. 150, “Accounting

for Certain Financial Instruments with Characteristics of

Both Liabilities and Equity.” This statement establishes

standards for how an issuer classifies and measures certain

financial instruments with characteristics of both liabilities

and equity. SFAS No. 150 is effective for financial

instruments entered into or modified after May 31, 2003, and

otherwise is effective at the beginning of the first interim

period beginning after June 15, 2003. The application of the

provisions of SFAS No. 150 has not and is not expected to

have a material impact on the company’s financial position,

results of operations, or cash flows.

14

13

In December 2003, the FASB issued SFAS No. 132 (revised

2003), “Employers’ Disclosures about Pensions and Other

Postretirement Benefits.” This revised statement retains the

disclosures required by the original SFAS No. 132, which

standardized employers’ disclosures about pensions and other

postretirement benefits, and requires additional disclosures

concerning the economic resources and obligations related to

pension plans and other postretirement benefits. The

provisions of the original SFAS No. 132 remain in effect until

the provisions of this revised statement are adopted. This

revised statement is effective for fiscal years ending after

December 15, 2003. The company has revised its disclosures

to meet the requirements under this revised standard for the

financial statements currently presented.

In December 2003, the FASB issued FASB Interpretation

(“FIN”) No. 46 (revised December 2003), “Consolidation of

Variable Interest Entities.” This revised interpretation retains

the original FIN No. 46 requirements for consolidating

variable interest entities by the primary beneficiary of the

entity if the equity investors in the entity do not have the

characteristics of a controlling financial interest or do not have

sufficient equity at risk for the entity to finance its activities

without additional subordinated financial support from other

parties. The revised interpretation adds the requirement for

consolidating an entity where the equity investors’ voting rights

are not proportionate to their economic interests and where the

activities of the entity involve or are conducted on behalf of an

investor with a disproportionately small voting interest. This

revised interpretation is effective for all entities no later than

the end of the first reporting period that ends after March 15,

2004. However, for reporting periods ending after December 15,

2003, a company must apply either the original or this revised

interpretation to those entities that are considered to be special-

purpose entities. A company that has already applied the

original FIN No. 46 to an entity may continue to do so until

the effective date of the revised interpretation. The company

has applied the revised FIN No. 46, which has not had a

material impact on the company’s financial position, results of

operations, or cash flows.