CarMax 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

18

CARMAX

2004

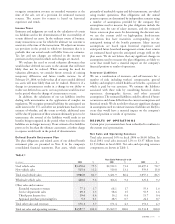

Fiscal 2004 Highlights

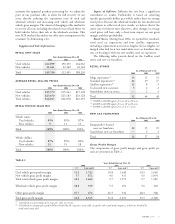

In fiscal 2004, net sales and operating revenues increased 16%

to $4.60 billion from $3.97 billion and net earnings increased

23% to $116.5 million, or $1.10 per share, from $94.8

million, or $0.91 per share. Sales and earnings were affected

by the following items:

■We opened nine used car superstores, including five standard-

sized stores in new markets and four satellite stores in existing

markets, including one replacement store in Los Angeles.

■Total used units increased 18%.

■Comparable store used units increased 6%. The expected

cannibalization resulting from the addition of satellite stores

occurred somewhat faster than originally projected;

however, we do not believe the ultimate amount of

cannibalization will be higher than originally planned. We

are achieving our net incremental sales objectives in the

markets where satellites have been added.

■Gross profit benefited from a change in our appraisal cost

recovery methodology, which is allowing us to more fully

recover the cost of our buying and wholesaling operations with

no adverse effect on the acceptance rate for our appraisal offers.

■CarMax Auto Finance income increased 3% in fiscal 2004,

as the benefit of the growth in our portfolio of CAF loans

was largely offset by the return to more normalized spreads

in the second half of the year. During fiscal 2002, fiscal

2003, and the first half of fiscal 2004, CAF benefited from

the unusually low interest rate environment, with consumer

rates falling more slowly than our cost of funds.

■Selling, general, and administrative expenses as a percent of

sales (the “SG&A ratio”) increased to 10.2% in fiscal 2004

from 9.9% in fiscal 2003. Excluding separation costs, the

fiscal 2003 SG&A ratio was 9.7%. The increase in the

SG&A ratio reflects both the growth penalty associated

with our resumption of geographic expansion and the

higher costs of being an independent company following

the separation from Circuit City. New stores generally have

higher SG&A ratios during the approximately four years it

takes to reach mature levels of revenues.

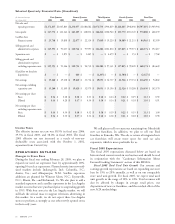

Net cash provided by operations increased to $148.5 million

in fiscal 2004 from $72.0 million in fiscal 2003, driven by the

increase in earnings and a slight reduction in inventory, despite

adding nine used car superstores during fiscal 2004. The decrease

in inventory reflects both higher-than-normal inventories at the

end of fiscal 2003 resulting from weather-impeded sales in

February 2003 and the disposal of four new car franchises during

the current fiscal year. During fiscal 2004, we completed three

sale-leaseback transactions covering a total of nine stores for total

proceeds of $107.0 million and we completed two public

securitizations of CAF receivables totaling $1.11 billion.

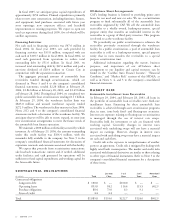

CRITICAL ACCOUNTING POLICIES

Our results of operations and financial condition, as reflected in

the company’s consolidated financial statements, have been

prepared in accordance with accounting principles generally

accepted in the United States of America. Preparation of

financial statements requires management to make estimates

and assumptions affecting the reported amounts of assets,

liabilities, revenues, expenses, and the disclosures of contingent

assets and liabilities. We use our historical experience and other

relevant factors when developing our estimates and assumptions.

We continually evaluate these estimates and assumptions. Note 2

to the company’s consolidated financial statements includes a

discussion of significant accounting policies. The accounting

policies discussed below are the ones we consider critical to an

understanding of the company’s consolidated financial

statements because their application places the most significant

demands on our judgment. Our financial results might have

been different if different assumptions had been used or other

conditions had prevailed.

Calculation of the Fair Value of Retained Interests

in Securitization Transactions

We use a securitization program to fund substantially all of the

automobile loan receivables originated by CAF. The fair value of

retained interests in securitization transactions includes the

present value of the expected residual cash flows generated by the

securitized receivables, the restricted cash on deposit in various

reserve accounts, and an undivided ownership interest in the

receivables securitized through a warehouse facility and certain

public securitizations. The present value of the expected residual

cash flows generated by the securitized receivables is determined

by estimating the future cash flows using management’s

assumptions of key factors, such as finance charge income,

default rates, prepayment rates, and discount rates appropriate

for the type of asset and risk. These assumptions are derived from

historical experience and projected economic trends.

Adjustments to one or more of these assumptions may have a

material impact on the fair value of retained interests. The fair

value of retained interests may be affected by external factors,

such as changes in the behavior patterns of customers, changes in

the strength of the economy, and developments in the interest

rate markets. Note 2(C) to the company’s consolidated financial

statements includes a discussion of accounting policies related to

securitizations. Note 4 to the company’s consolidated financial

statements includes a discussion of securitizations and provides a

sensitivity analysis showing the hypothetical effect on the

retained interests if there are variations from the assumptions

used. In addition, see the “CarMax Auto Finance Income”

section of this MD&A for a discussion of the current year impact

of changing our assumptions.

Revenue Recognition

We recognize revenue when the earnings process is complete,

generally either at the time of sale to a customer or upon

delivery to a customer. The majority of our revenue is generated

from the sale of used vehicles. We recognize vehicle revenue

when a sales contract has been executed and the vehicle has

been delivered, net of a reserve for returns. A reserve for vehicle

returns is recorded based on historical experience and trends.

The estimated reserve for these returns could be affected if

future occurrences differ from historical averages.

We also sell extended warranties on behalf of unrelated third

parties to customers who purchase a vehicle. Because these third

parties are the primary obligors under these warranties, we