CarMax 2004 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2004 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

10

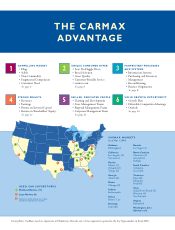

CARMAX 2004

FINANCE ORIGINATIONS

■CarMax has created a unique finance origination structure

that provides significant customer benefits and competi-

tive advantages.

•The sales consultant collects the customer’s credit infor-

mation and electronically submits the loan application to

CarMax Auto Finance (“CAF”) and a third-party prime

lender. If there are no prime offers, the application is auto-

matically routed to third-party, non-prime lenders.

•Customers see each offer directly from the lender, and,

where multiple offers exist, they may choose the offer

that best suits their needs.

•We provide a 3-day payoff option, which gives cus-

tomers up to three business days to replace the loan with

cash or an alternative lending source, free of penalty or

interest.

•The sales consultant receives no commission on the

finance process.

■This structure reduces or eliminates two of the three risks

inherent in used car lending.

•The consumer risk — the customer’s willingness and

ability to pay — is the basic risk borne by all lenders.

•The collateral risk — the risk of the vehicle — is mini-

mized by the consistent, high quality of our cars, the

large percentage of vehicles covered by extended service

plans, and the consistency of the relationship between

wholesale and retail values for CarMax vehicles. CAF

and our third-party lenders have found they can rely on

CarMax information to determine true vehicle worth.

•The “intermediary” risk — the risk introduced by the

person between the customer and the finance source —

is eliminated at CarMax. There is no commission-

driven finance manager to distort the facts on the

price or quality of the vehicle or the consumer credit

information. With the price of all components fixed,

value-oriented, and non-negotiable at CarMax, both

CAF and third-party lenders benefit from superior

information quality in making financing decisions.

■Having our own finance operation also reduces the sales

risk associated with changes in third-party credit availability.