CarMax 2004 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2004 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

CARMAX

2004 23

CAF originates automobile loans to CarMax customers at

competitive market rates of interest. The majority of the profit

contribution from CAF is generated by the spread between the

interest rate charged to the customer and the cost of funds.

Substantially all of the loans originated by CAF each month are

sold in securitization transactions as described in Note 4 to the

company’s consolidated financial statements. A gain, recorded

at the time of the securitization transaction, results from

recording a receivable equal to the present value of the expected

residual cash flows generated by the securitized receivables. The

cash flows are calculated taking into account expected

prepayment and default rates.

CarMax Auto Finance income as a percentage of total net

sales and operating revenues decreased in fiscal 2004. The

decrease was attributable to spreads returning to more

normalized levels during the second half of fiscal 2004. During

fiscal 2002, fiscal 2003, and the first half of fiscal 2004, we

benefited from higher than normal spreads due to consumer

loan rates falling more slowly than our cost of funds. The fiscal

2003 increase in CAF income as a percentage of net sales and

operating revenues was primarily the result of the $11.8 million

increase in the gains on sales of loans and the increase in other

income related to our managed portfolio. The gains on sales of

loans increase resulted from an increase in loans sold driven by

a higher sales volume and higher CAF penetration, partially

offset by a marginal decline in yield spreads. The increase in

other income and total direct expenses was proportionate to the

increase in the managed receivables for all fiscal years presented.

We are at risk for the performance of the securitized

receivables managed to the extent that we maintain a retained

interest in the receivables. Supplemental information on our

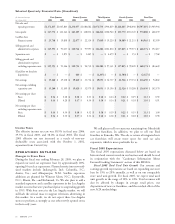

portfolio of managed receivables is shown in the following tables:

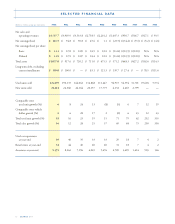

As of February 29 or 28

(In millions)

2004 2003 2002

Loans securitized $2,200.4 $1,859.1 $1,489.4

Loans held for sale

or investment 48.2 19.6 13.9

Ending managed receivables $2,248.6 $1,878.7 $1,503.3

Accounts 31+ days past due $31.4 $ 27.6 $ 22.3

Past due accounts as a

percentage of ending

managed receivables 1.40% 1.47% 1.48%

Years Ended February 29 or 28

(In millions)

2004 2003 2002

Average managed

receivables $2,099.4 $1,701.0 $1,393.7

Credit losses on managed

receivables $21.1 $ 17.5 $ 12.9

Credit losses as a

percentage of average

managed receivables 1.01% 1.03% 0.93%

Credit losses as a percentage of average managed receivables

for fiscal years 2004 and 2003 were comparable. The increase

in losses as a percentage of average managed receivables for

fiscal 2003 compared with fiscal 2002 was primarily due to

depressed wholesale vehicle values which led to lower recovery

rates on repossessed vehicles. The recovery rate was 42% in

fiscal 2004, 43% in fiscal 2003, and 45% in fiscal 2002. The

recovery rate represents the average percentage of the

outstanding principal balance CarMax receives when a vehicle

is repossessed and liquidated.

If the managed receivables do not perform in accordance

with the assumptions used in determining the fair value of the

retained interests, earnings could be impacted. Past due

accounts as a percentage of ending managed receivables were

comparable for all fiscal years presented. In fiscal 2004, we

adjusted the cumulative default rate assumptions for certain

pools of receivables. We increased the loss rates for two of our

older pools of receivables to reflect slightly higher losses at the

end of the pools’ lives. We also increased the loss rate on current

originations from 1.85% to 2.00%, reflecting current

economic conditions, including weak recovery rates that

stabilized at historically low levels. There was no change in the

credit quality of the receivables, which was at the high end of

our historical range. The changes resulted in no material impact

on earnings or the fair value of retained interests. Details

concerning the assumptions used to value the retained interests

and the sensitivity to adverse changes in the performance of the

managed receivables are included in Note 4 to the company’s

consolidated financial statements.

Selling, General and Administrative Expenses

The SG&A ratio was 10.2% of net sales and operating revenues

in fiscal 2004, 9.9% in fiscal 2003, and 9.5% in fiscal 2002.

The SG&A ratio for fiscal 2003 and 2002 included one-time

costs of $7.8 million and $0.4 million, respectively, associated

with the separation of CarMax from Circuit City. Excluding

these costs, the SG&A ratio would have been 9.7% in fiscal

2003 and 9.5% in fiscal 2002.

The fiscal 2004 and fiscal 2003 SG&A ratios reflect the

expected higher level of operating expenses associated with

being a stand-alone company following the October 1, 2002,

separation from Circuit City. We estimated stand-alone costs

were approximately $13.5 million higher in fiscal 2004 than in

fiscal 2003, and approximately $9.0 million higher in fiscal

2003 than in fiscal 2002. A majority of these costs related to

employee benefits and insurance.

As anticipated, the fiscal 2004 SG&A ratio was adversely

affected by the resumption of our store growth plan and the

increase in the number of store openings. New stores typically

experience higher SG&A ratios than stores with mature sales

levels, reflecting the sales ramp that occurs over time. Higher

total pre-opening expenses and costs related to building our

management team bench strength to support future store

growth also contributed to the higher current year SG&A ratio.