CarMax 1999 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 1999 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

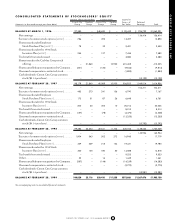

|

|

Receivables relating to the securitization facilities consist of

the following at February 28:

(Amounts in thousands)

1999 1998

Managed receivables ....................... $2,957,132 $2,749,793

Receivables/residual interests held

by the Company:

For sale ....................................... (39,948) (44,622)

For investment............................ (161,996) (203,921)

Net receivables sold......................... $2,755,188 $2,501,250

Net receivables sold

with recourse.............................. $ 322,000 $ 726,000

Program capacity............................. $3,127,000 $3,075,000

Private-label credit card receivables are financed through

securitization programs employing a master trust structure. As of

February 28, 1999, this securitization program had a capacity of

$1.38 billion. The agreement has no recourse provisions.

During fiscal 1998, a bank card master trust securitization

facility was established and issued two series from the trust.

Provisions under the master trust agreement provide recourse to

the Company for any cash flow deficiencies on $322 million of

the receivables sold. The finance charges from the transferred

receivables are used to fund interest costs, charge-offs, servicing

fees and other related costs. The Company believes that as of

February 28, 1999, no liability existed under these recourse provi-

sions. The bank card securitization program has a total program

capacity of $1.75 billion.

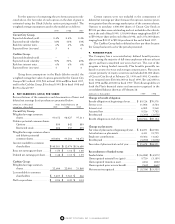

The net gain on sales of receivables totaled $2.3 million for

fiscal 1999, $21.8 million for fiscal 1998 and $3.2 million for fiscal

1997. The finance operation’s servicing revenue, including gains on

sales of receivables, totaled $200.6 million for fiscal 1999, $195.7

million for fiscal 1998 and $197.0 million for fiscal 1997. Rights

recorded for future interest income from serviced assets that exceed

the contractually specified servicing fees are carried at fair value and

amounted to $27.3 million at February 28, 1999, $25.0 million at

February 28, 1998, and $3.2 million at February 28, 1997, and are

included in net accounts receivable. The servicing fees specified in

the credit card securitization agreements adequately compensate

the finance operation for servicing the accounts. Accordingly, no

servicing asset or liability has been recorded.

In determining the fair value of retained interests, the

Company estimates future cash flows from finance charge collec-

tions, reduced by net defaults, servicing cost and interest cost.

The Company employs a risk-based pricing strategy that increases

the stated annual percentage rate for accounts that have a higher

predicted risk of default. Accounts with a lower risk profile also

may qualify for promotional financing.

The private-label card programs, excluding promotional bal-

ances, range from 21 percent to 24 percent APR, with default rates

varying based on portfolio composition, but generally aggregat-

ing from 6 percent to 10 percent. Principal payment rates vary

widely both seasonally and by credit terms but are in the range of

9 percent to 12 percent.

The bank card APRs are based on the prime rate and generally

range from 7 percent to 22 percent, with default rates varying by

portfolio composition, but generally aggregating from 8 percent to

12 percent. Principal payment rates vary widely both seasonally

and by credit terms but are in the range of 5 percent to 8 percent.

Interest cost paid by the master trusts varies between series

and ranges from 5.0 percent to 6.3 percent.

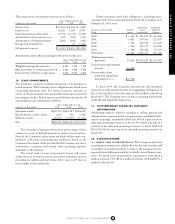

(B) AUTOMOBILE LOAN SECURITIZATION:

In fiscal 1996, the

Company entered into a securitization agreement to finance the

consumer installment credit receivables generated by its automo-

bile loan finance operation. Proceeds from the automobile loan

securitization transaction were $271 million during fiscal 1999,

$123 million during fiscal 1998 and $58 million during fiscal 1997.

Receivables relating to the securitization facility consist of

the following at February 28:

(Amounts in thousands)

1999 1998

Managed receivables.............................. $589,032 $291,294

Receivables held by the Company:

For sale.............................................. (14,690) (5,816)

For investment* ................................ (35,342) (17,478)

Net receivables sold............................... $539,000 $268,000

Program capacity................................... $575,000 $300,000

*Held by a bankruptcy remote special purpose company

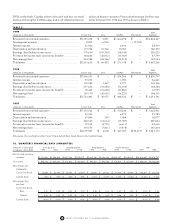

The finance charges from the transferred receivables are used

to fund interest costs, charge-offs and servicing fees. A restructur-

ing of the facility during fiscal 1997 resulted in the recourse provi-

sions being eliminated.

The net gain on sales of receivables totaled $7.9 million for

fiscal 1999, $3.7 million for fiscal 1998 and $3.1 million for fiscal

1997. Rights recorded for future interest income from serviced

assets that exceed the contractually specified servicing fees are

carried at fair value and amounted to $14.7 million at February 28,

1999, $6.8 million at February 28, 1998, and $3.1 million at

February 28, 1997, and are included in net accounts receivable.

The finance operation’s servicing revenue, including gains on sales

of receivables, totaled $28.2 million for fiscal 1999, $11.2 million

for fiscal 1998 and $8.7 million for fiscal 1997. The servicing fee

specified in the auto loan securitization agreement adequately

compensates the finance operation for servicing the accounts.

Accordingly, no servicing asset or liability has been recorded.

In determining the fair value of retained interests, the

Company estimates future cash flows from finance charge collec-

tions, reduced by net defaults, servicing cost and interest cost.

The Company employs a risk-based pricing strategy that

increases the stated APR for accounts that have a higher predicted

risk of default. Accounts with a lower risk profile also may qualify

for promotional financing.

42 CIRCUIT CITY STORES, INC. 1999 ANNUAL REPORT