CarMax 1999 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 1999 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

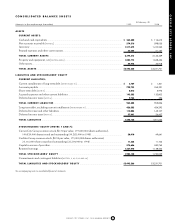

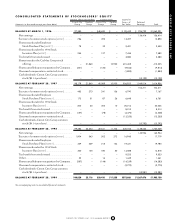

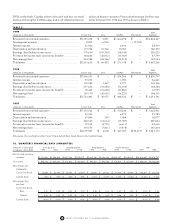

In May 1995, the Company entered into a five-year,

$175,000,000, unsecured bank term loan. Principal is due in full at

maturity with interest payable periodically at LIBOR plus 0.35

percent. At February 28, 1999, the interest rate on the term loan

was 5.67 percent.

In June 1996, the Company entered into a five-year,

$130,000,000, unsecured bank term loan. Principal is due in full at

maturity with interest payable periodically at LIBOR plus 0.35

percent. At February 28, 1999, the interest rate on the term loan

was 5.29 percent.

The Company maintains a multi-year, $150,000,000, unse-

cured revolving credit agreement with four banks. The agreement

calls for interest based on both committed rates and money mar-

ket rates and a commitment fee of 0.13 percent per annum. The

agreement was entered into as of August 31, 1996, and terminates

August 31, 2002. No amounts were outstanding under the revolv-

ing credit agreement at February 28, 1999 or 1998.

The Industrial Development Revenue Bonds are collateral-

ized by land, buildings and equipment with an aggregate carrying

value of approximately $10,740,000 at February 28, 1999, and

$10,879,000 at February 28, 1998.

In November 1998, CarMax entered into a four-year, unse-

cured $5,000,000 promissory note. Principal is due annually with

interest payable periodically at 8.25 percent.

In fiscal 1999, CarMax entered into a $200,000,000 one-

year, renewable inventory financing arrangement with an asset-

backed commercial paper conduit. The arrangement will provide

funding for the acquisition of vehicle inventory through the use of

a non-affiliated special purpose company. During fiscal 1999, no

inventory was financed by CarMax under this arrangement.

The scheduled aggregate annual principal payments on long-

term obligations for the next five fiscal years are as follows: 2000 -

$2,707,000; 2001 - $177,344,000; 2002 - $132,485,000; 2003 -

$102,594,000; 2004 - $1,507,000.

Under certain of the debt agreements, the Company must

meet financial covenants relating to minimum tangible net worth,

current ratios and debt-to-capital ratios. The Company was in

compliance with all such covenants at February 28, 1999 and 1998.

Short-term debt is funded through committed lines of credit

and informal credit arrangements, as well as the revolving agree-

ment. Amounts outstanding and committed lines of credit avail-

able are as follows:

Years Ended February 28

(Amounts in thousands)

1999 1998

Average short-term debt outstanding ........... $ 54,505 $ 48,254

Maximum short-term debt outstanding........ $463,000 $414,000

Aggregate committed lines of credit............. $370,000 $410,000

The weighted average interest rate on the outstanding short-

term debt was 5.1 percent during fiscal 1999, 5.7 percent during

fiscal 1998 and 5.4 percent during fiscal 1997.

The Company capitalizes interest in connection with the

construction of certain facilities and software developed or

obtained for internal use. In fiscal 1999, interest capitalized

amounted to $5,423,000 ($9,638,000 in fiscal 1998 and

$6,970,000 in fiscal 1997).

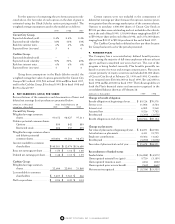

6. INCOME TAXES

The Company files a consolidated federal income tax return. The

components of the provision for income taxes are as follows:

Years Ended February 28

(Amounts in thousands)

1999 1998 1997

Current:

Federal ......................................... $59,134 $46,475 $55,673

State............................................. 7,833 2,406 6,964

66,967 48,881 62,637

Deferred:

Federal ......................................... 20,013 12,801 19,839

State............................................. 619 2,251 1,134

20,632 15,052 20,973

Provision for income taxes................ $87,599 $63,933 $83,610

The effective income tax rate differed from the Federal statu-

tory income tax rate as follows:

Years Ended February 28

1999 1998 1997

Federal statutory income

tax rate............................................. 35.0% 35.0% 35.0%

State and local income taxes,

net of Federal benefit....................... 3.0%3.0%3.0%

Effective income tax rate...................... 38.0% 38.0% 38.0%

In accordance with SFAS No. 109, the tax effects of tempo-

rary differences that give rise to a significant portion of the

deferred tax assets and liabilities at February 28, 1999 and 1998,

are as follows:

(Amounts in thousands)

1999 1998

Deferred tax assets:

Deferred revenue ........................................ $ 8,332 $ 1,360

Inventory capitalization.............................. 2,578 4,976

Accrued expenses........................................ 27,080 42,554

Other .......................................................... 5,430 3,638

Total gross deferred tax assets................. 43,420 52,528

Deferred tax liabilities:

Depreciation and amortization ................... 48,035 45,118

Gain on sales of receivables......................... 14,990 11,439

Other prepaid expenses .............................. 12,062 10,569

Other .......................................................... 15,758 12,195

Total gross deferred tax liabilities........... 90,845 79,321

Net deferred tax liability................................... $47,425 $26,793

Based on the Company’s historical and current pretax earn-

ings, management believes the amount of gross deferred tax assets

will be realized through future taxable income; therefore, no valu-

ation allowance is necessary.

CIRCUIT CITY STORES, INC.

CIRCUIT CITY STORES, INC. 1999 ANNUAL REPORT 37