CVS 2014 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2014 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

46

CVS Health

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

Self-Insurance Liabilities

We are self-insured for certain losses related to general liability, workers’ compensation and auto liability, although

we maintain stop loss coverage with third party insurers to limit our total liability exposure. We are also self-insured

for certain losses related to health and medical liabilities.

The estimate of our self-insurance liability contains uncertainty since we must use judgment to estimate the

ultimate cost that will be incurred to settle reported claims and unreported claims for incidents incurred but not

reported as of the balance sheet date. When estimating our self-insurance liability, we consider a number of factors,

which include, but are not limited to, historical claim experience, demographic factors, severity factors and other

standard insurance industry actuarial assumptions. On a quarterly basis, we review our self-insurance liability to

determine if it is adequate as it relates to our general liability, workers’ compensation and auto liability. Similar

reviews are conducted semi-annually to determine if our self-insurance liability is adequate for our health and

medical liability.

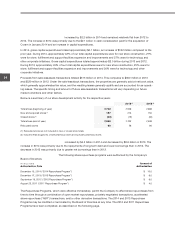

Our total self-insurance liability covered by this critical accounting policy was $628 million as of December 31,

2014. Although we believe we have sufficient current and historical information available to us to record reasonable

estimates for our self-insurance liability, it is possible that actual results could differ. In order to help you assess the

risk, if any, associated with the uncertainties discussed previously, a ten percent (10%) pre-tax change in our

estimate for our self-insurance liability, which we believe is a reasonably likely change, would increase or decrease

our self-insurance liability by about $63 million as of December 31, 2014.

We have not made any material changes in the accounting methodology used to establish our self-insurance liability

during the past three years.

Income Taxes

Income taxes are accounted for using the asset and liability method. Deferred tax liabilities or assets are estab-

lished for temporary differences between financial and tax reporting bases and are subsequently adjusted to

reflect changes in enacted tax rates expected to be in effect when the temporary differences reverse. The

deferred tax assets are reduced, if necessary, by a valuation allowance to the extent future realization of those

tax benefits is uncertain.

Significant judgment is required in determining the provision for income taxes and the related taxes payable and

deferred tax assets and liabilities since, in the ordinary course of business, there are transactions and calculations

where the ultimate tax outcome is uncertain. Additionally, our tax returns are subject to audit by various domestic

and foreign tax authorities that could result in material adjustments or differing interpretations of the tax laws.

Although we believe that our estimates are reasonable and are based on the best available information at the time

we prepare the provision, actual results could differ from these estimates resulting in a final tax outcome that may

be materially different from that which is reflected in our consolidated financial statements.

The tax benefit from an uncertain tax position is recognized only if it is more likely than not that the tax position will

be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits

recognized in the consolidated financial statements from such positions are then measured based on the largest

benefit that has a greater than 50% likelihood of being realized upon settlement. Interest and/or penalties related to

uncertain tax positions are recognized in income tax expense. Significant judgment is required in determining our

uncertain tax positions. We have established accruals for uncertain tax positions using our best judgment and adjust

these accruals, as warranted, due to changing facts and circumstances.