CVS 2014 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2014 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

Management’s Discussion and Analysis

of Financial Condition and Results of Operations

34

CVS Health

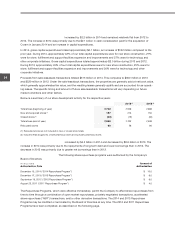

revenues in 2014 and 2013 was primarily driven by increased pharmacy margins due to the positive impact of

increased generic dispensing rates and increased front store margins, partially offset by continued reimbursement

pressure. The increase in gross profit as a percentage of net revenues in 2014 was also driven by the removal of

tobacco products from our stores.

As you review our Retail Pharmacy Segment’s performance in this area, we believe you should consider the follow-

ing important information:

• Gross profit dollars and margin for the year ended December 31, 2014 were positively impacted by $53 million

related to the favorable resolution of previously proposed retroactive reimbursement rate changes in the State of

California’s Medicaid program.

• Sales to customers covered by third party insurance programs are a large component of our total pharmacy

business. On average, our gross profit on third party pharmacy revenues is lower than our gross profit on cash

pharmacy revenues. Third party pharmacy revenues were 98.6% of pharmacy revenues in 2014, compared to

97.9% and 97.5% of pharmacy revenues in 2013 and 2012, respectively.

• Front store revenues as a percentage of total net revenues for the years ended December 31, 2014, 2013 and

2012 were 28.8%, 30.5% and 31.2%, respectively. The decline in front store revenues as a percentage of total net

revenues in 2014 was largely due to the removal of tobacco products and the estimated associated basket sales.

On average, our gross profit on front store revenues is generally higher than our gross profit on pharmacy reve-

nues. Pharmacy revenues as a percentage of total net revenues increased approximately 120, 60 and 50 basis

points in the years ended December 31, 2014, 2013 and 2012, respectively. This shift in sales to the pharmacy

had a negative effect on our overall gross profit for the years ended December 31, 2014, 2013 and 2012, respec-

tively. The negative effect was offset by increasing generic drug dispensing rates and increased store brand

penetration.

• During the year ended December 31, 2014, our front store gross profit as a percentage of net revenues increased

compared to the prior year. The increase is primarily related to a change in the mix of products sold, including the

removal of tobacco products from our stores, and higher store brand sales.

• Our pharmacy gross profit rates have been adversely affected by the efforts of managed care organizations,

pharmacy benefit managers and governmental and other third party payors to reduce their prescription drug

costs. In the event this trend continues, we may not be able to sustain our current rate of revenue growth and

gross profit dollars could be adversely impacted. The increased use of generic drugs has positively impacted

our gross profit margins but has resulted in third party payors augmenting their efforts to reduce reimbursement

payments to retail pharmacies for prescriptions. This trend, which we expect to continue, reduces the benefit

we realize from brand to generic product conversions.

• ACA made several significant changes to Medicaid rebates and to reimbursement. One of these changes was

the proposed revision of the definition of Average Manufacturer Price (“AMP”) and the reimbursement formula for

multi-source drugs. Changes in reporting of AMP or other adjustments that may be made regarding the reim-

bursement of drug payments by Medicaid and Medicare could impact our pricing to customers and other payors

and/or could impact our ability to negotiate discounts or rebates with manufacturers, wholesalers, PBMs or retail

and mail pharmacies. See “Efforts to reduce reimbursement levels and alter health care financing practices” in

Part I, Item 1A, Risk Factors within our 2014 Form 10-K, for additional information.

Operating expenses

in our Retail Pharmacy Segment include store payroll, store employee benefits, store

occupancy costs, selling expenses, advertising expenses, depreciation and amortization expense and certain

administrative expenses.