CVS 2007 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2007 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

|

|

58 I CVS Caremark

effective December 15, 2006. SFAS No. 158 requires an employer

to recognize in its statement of financial position an asset for a

plan’s overfunded status or a liability for a plan’s underfunded

status, measure a plan’s assets and its obligations that determine

its funded status as of the end of the employer’s fiscal year, and

recognize changes in the funded status of a defined benefit

postretirement plan in the year in which the changes occur.

Those changes are reported in comprehensive income and in a

separate component of shareholders’ equity. The adoption of

this statement did not have a material impact on the Company’s

consolidated results of operations, financial position or cash flows.

Stock Incentive Plans

On January 1, 2006, the Company adopted SFAS No. 123(R),

“Share-Based Payment”, using the modified prospective transi-

tion method. Under this method, compensation expense is

recognized for options granted on or after January 1, 2006

as well as any unvested options on the date of adoption.

Compensation expense for unvested stock options outstanding

at January 1, 2006 is recognized over the requisite service period

based on the grant-date fair value of those options and awards

as previously calculated under the SFAS No. 123(R) pro forma

disclosure requirements. As allowed under the modified prospec-

tive transition method, prior period financial statements have not

been restated. Prior to January 1, 2006, the Company accounted

for its stock-based compensation plans under the recognition and

measurement principles of APB Opinion No. 25, “Accounting for

Stock Issued to Employees,” and related interpretations. As such,

no stock-based employee compensation costs were reflected in

net earnings for options granted under those plans since they had

an exercise price equal to the fair market value of the underlying

common stock on the date of grant.

Compensation expense related to stock options, which

includes the 1999 Employee Stock Purchase Plan (“1999 ESPP”)

and the 2007 Employee Stock Purchase Plan (“2007 ESPP” and

collectively the “ESPP”) totaled $84.5 million for 2007, compared

to $60.7 million for 2006. The recognized tax benefit was

$26.9 million and $18.0 million for 2007 and 2006, respectively.

Compensation expense related to restricted stock awards totaled

$12.1 million for 2007, compared to $9.2 million for 2006.

Compensation costs associated with the Company’s share-

based payments are included in selling, general and

administrative expenses.

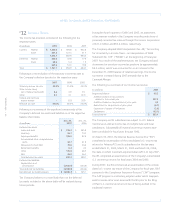

The following table includes the effect on net earnings and

earnings per share if stock compensation costs had been

determined consistent with the fair value recognition provisions

of SFAS No. 123(R) for 2005:

In millions, except per share amounts 2005

Net earnings, as reported $ 1,224.7

Add: Stock-based employee compensation

expense included in reported net earnings,

net of related tax effects(1) 4.8

Deduct: Total stock-based employee compensation

expense determined under fair value based method

for all awards, net of related tax effects 48.6

Pro forma net earnings $ 1,180.9

Basic EPS: As reported $ 1.49

Pro forma 1.44

Diluted EPS: As reported $ 1.45

Pro forma 1.40

(1) Amounts represent the after-tax compensation costs for restricted

stock grants and expense related to the acceleration of vesting of

stock options on certain terminated employees.

The 1999 ESPP provides for the purchase of up to 14.8 million

shares of common stock. As a result of the 1999 ESPP not

having sufficient shares available for the program to continue

beyond 2007, the Board of Directors adopted, and shareholders

approved, the 2007 ESPP. Under the 2007 ESPP, eligible employ-

ees may purchase common stock at the end of each six-month

offering period, at a purchase price equal to 85% of the lower

of the fair market value on the first day or the last day of

the offering period and provides for the purchase of up to

15.0 million shares of common stock. During 2007, 1.9 million

shares of common stock were purchased, under the provisions of

the 1999 ESPP, at an average price of $25.10 per share. As of

December 29, 2007, 14.1 million shares of common stock have

been issued under the 1999 ESPP. As of December 29, 2007, no

common stock had been issued under the 2007 ESPP.

The fair value of stock compensation expense associated with

the Company’s ESPP is estimated on the date of grant (i.e.,

the beginning of the offering period) using the Black-Scholes

Option Pricing Model and is recorded as a liability, which is

adjusted to reflect the fair value of the award at the end of

each reporting period until settlement date.

#10