CVS 2007 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2007 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

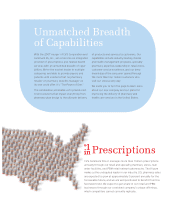

Unmatched Breadth

of Capabilities

With the 2007 merger of CVS Corporation and

Caremark Rx, Inc., we’ve become an integrated

provider of prescriptions and related health

services with an unmatched breadth of capa-

bilities. We’re the market leader in multiple

categories and able to provide payors and

patients with solutions that no pharmacy

retailer or pharmacy benets manager on

its own could offer. It’s “The Power of One.”

The combination will enable us to provide end-

to-end solutions that impact everything from

pharmacy plan design to the ultimate delivery

of products and services to customers. Our

capabilities include industry-leading clinical

and health management programs, specialty

pharmacy expertise, leadership in retail clinics,

customer service excellence, and our deep

knowledge of the consumer gained through

the more than four million customers who

visit our stores every day.

We invite you to turn the page to learn more

about our new company and our plans for

improving the delivery of pharmacy and

health care services in the United States.

Prescriptions

CVS Caremark lls or manages more than 1 billion prescriptions

annually through our retail and specialty pharmacy stores, mail

order facilities, and PBM retail network pharmacies. That gure

makes us the undisputed leader in our industry. U.S. pharmacy sales

are expected to grow at approximately 5 percent annually for the

foreseeable future, and we are well positioned to benet from this

favorable trend. We expect to gain share in our retail and PBM

businesses through our combined company’s unique offerings,

which competitors cannot currently replicate.

#1

in

#1

in