CVS 2007 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2007 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

23 I 2007 Annual Report

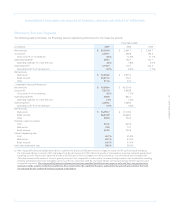

Net revenues. As you review our Retail Pharmacy Segment’s

performance in this area, we believe you should consider the

following important information:

• During 2006, total net revenues were significantly affected

by the acquisition of the Standalone Drug Business on June 2,

2006. Revenues from the Standalone Drug Business increased

total net revenues by approximately 4.9% and 8.7% during 2007

and 2006, respectively.

• During 2005, total net revenues were significantly affected by

the July 31, 2004 acquisition of certain assets and assumption

of certain liabilities from J.C. Penney Company, Inc. and certain

of its subsidiaries, including Eckerd Corporation (“Eckerd”). This

acquisition included more than 1,200 Eckerd retail drugstores

and Eckerd Health Services, which included Eckerd’s mail order

and pharmacy benefit management businesses (collectively, the

“2004 Acquired Businesses”). Revenues from the 2004 Acquired

Businesses increased total net revenues by approximately 11.2%

during 2005. Beginning in August 2005, same store sales include

the acquired Eckerd stores, which increased total same store

sales by approximately 110 basis points during 2006.

• Total net revenues from new stores accounted for approximately

130 basis points of our total net revenue percentage increase in

2007 and 2006 compared to 160 basis points in 2005.

• Total net revenues continued to benefit from our active

relocation program, which moves existing in-line shopping

center stores to larger, more convenient, freestanding locations.

Historically, we have achieved significant improvements in

customer count and net revenue when we do this. As such,

our relocation strategy remains an important component of

our overall growth strategy. As of December 29, 2007, approxi-

mately 64% of our existing stores were freestanding, compared

to approximately 61% and 59% at December 30, 2006 and

December 31, 2005, respectively.

• Pharmacy revenue growth continued to benefit from new

market expansions, increased penetration in existing markets,

the introduction of a prescription drug benefit under Medicare

Part D in 2006, our ability to attract and retain managed care

customers and favorable industry trends. These trends include

an aging American population; many “baby boomers” are now

in their fifties and sixties and are consuming a greater number

of prescription drugs. In addition, the increased use of pharma-

ceuticals as the first line of defense for individual healthcare

also contributed to the growing demand for pharmacy services.

We believe these favorable industry trends will continue.

• Pharmacy revenue dollars continue to be negatively impacted in

all years by the conversion of brand named drugs to equivalent

generic drugs, which typically have a lower selling price. In

addition, our pharmacy growth has also been adversely affected

by the growth of the mail order channel, a decline in the number

of significant new brand named drug introductions, higher

consumer co-payments and co-insurance arrangements and by

an increase in the number of over-the-counter remedies that

were historically only available by prescription. We may choose

not to participate in certain prescription benefit programs that

mandate filling maintenance prescriptions through a mail order

service facility or that implement pharmacy reimbursement rates

that fall below our minimum profitability standards. In the event

we elect to, for any reason, withdraw from current programs

and/or decide not to participate in future programs, we may not

be able to sustain our current rate of sales growth.

Gross profit, which includes net revenues less the cost of

merchandise sold during the reporting period and the related

purchasing costs, warehousing costs, delivery costs and actual

and estimated inventory losses, as a percentage of net revenues

was 29.1% in 2007. This compares to 28.0% in 2006 and 27.4%

in 2005.

As you review our Retail Pharmacy Segment’s performance in

this area, we believe you should consider the following important

information:

• Front store revenues increased as a percentage of total revenues

during 2007. On average our gross profit on front store revenues

is higher than our average gross profit on pharmacy revenues.

Pharmacy revenues as a percentage of total revenues were 67.8%

in 2007, compared to 68.4% in 2006 and 68.6% in 2005.

• Front store gross profit rate benefited from improved product

mix and benefits from our ExtraCare loyalty program.

• Our pharmacy gross profit rate benefited from a portion of the

significant purchasing synergies resulting from the Caremark

Merger. We expect the benefit from purchasing synergies to

continue to positively impact our pharmacy gross profit rate

through fiscal 2008.