CVS 2007 Annual Report Download - page 34

Download and view the complete annual report

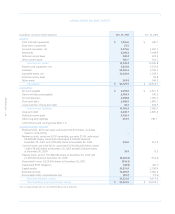

Please find page 34 of the 2007 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

30 I CVS Caremark

may be redeemed at any time, in whole or in part at a defined

redemption price plus accrued interest. Net proceeds from the

2006 Notes were used to repay a portion of the outstanding

commercial paper issued to finance the Standalone Drug

Business. To manage a portion of the risk associated with

potential changes in market interest rates, during the second

quarter of 2006 we entered into forward starting pay fixed rate

swaps (the “Swaps”), with a notional amount of $750 million.

The Swaps settled in conjunction with the placement of the long-

term financing. As of December 29, 2007 and December 30,

2006, we had no freestanding derivatives in place.

Our credit facilities, unsecured senior notes and ECAPS contain

customary restrictive financial and operating covenants. These

covenants do not include a requirement for the acceleration of

our debt maturities in the event of a downgrade in our credit

rating. We do not believe the restrictions contained in these

covenants materially affect our financial or operating flexibility.

As of December 29, 2007, our long-term debt was rated “Baa2”

by Moody’s and “BBB+” by Standard & Poor’s, and our commer-

cial paper program was rated “P-2” by Moody’s and “A-2” by

Standard & Poor’s. Upon completion of the Caremark Merger,

Standard & Poor’s raised the Company’s credit watch outlook

from negative to stable. On May 21, 2007, Moody’s also raised

the Company’s credit watch from negative to stable. In assessing

our credit strength, we believe that both Moody’s and Standard &

Poor’s considered, among other things, our capital structure and

financial policies as well as our consolidated balance sheet, our

acquisition of the Standalone Drug Business, the Caremark

Merger and other financial information. Although we currently

believe our long-term debt ratings will remain investment grade,

we cannot guarantee the future actions of Moody’s and/or

Standard & Poor’s. Our debt ratings have a direct impact on our

future borrowing costs, access to capital markets and new store

operating lease costs.

Off-Balance Sheet Arrangements

In connection with executing operating leases, we provide a

guarantee of the lease payments. We finance a portion of our

new store development through sale-leaseback transactions,

which involve selling stores to unrelated parties and then leasing

the stores back under leases that qualify and are accounted for

as operating leases. We do not have any retained or contingent

the November ASR agreement. Pursuant to the terms of the

November ASR agreement, on November 7, 2007, we paid

$2.3 billion to Lehman in exchange for Lehman delivering

37.2 million shares of common stock to us, which were placed

into our treasury account upon delivery. On November 26, 2007,

upon establishment of the minimum number of shares to be

repurchased, Lehman delivered an additional 14.4 million shares

of common stock to us. As of December 29, 2007, the aggregate

51.6 million shares of common stock received pursuant to the

November ASR agreement had been placed into our treasury

account. We may receive up to 5.7 million additional shares of

common stock, depending on the market price of the common

stock, as determined under the November ASR agreement, over

the term of the November ASR agreement, which is currently

expected to conclude during the first quarter of 2008.

Accordingly, the $5.0 billion share repurchase program authorized

by our Board of Directors has been completed pending the final

settlement of the November ASR agreement discussed previously.

We will, however, continue to evaluate alternatives for optimizing

our capital structure on an ongoing basis.

On May 22, 2007, we issued $1.75 billion of floating rate senior

notes due June 1, 2010, $1.75 billion of 5.75% unsecured senior

notes due June 1, 2017, and $1.0 billion of 6.25% unsecured

senior notes due June 1, 2027 (collectively the “2007 Notes”).

Also on May 22, 2007, we entered into an underwriting

agreement with Lehman Brothers, Inc., Morgan Stanley & Co.

Incorporated, Banc of America Securities LLC, BNY Capital

Markets, Inc., and Wachovia Capital Markets, LLC, as representa-

tives of the underwriters pursuant to which we agreed to issue

and sell $1.0 billion of Enhanced Capital Advantaged Preferred

Securities (“ECAPS”) due June 1, 2062 to the underwriters.

The ECAPS bear interest at 6.302% per year until June 1, 2012

at which time they will pay interest based on a floating rate. The

2007 Notes and the ECAPS pay interest semi-annually and may

be redeemed at any time, in whole or in part at a defined redemp-

tion price plus accrued interest. The net proceeds from the 2007

Notes and ECAPS were used to repay the bridge credit facility and

a portion of the outstanding commercial paper borrowings.

On August 15, 2006, we issued $800 million of 5.75% unsecured

senior notes due August 15, 2011 and $700 million of 6.125%

unsecured senior notes due August 15, 2016 (collectively the

“2006 Notes”). The 2006 Notes pay interest semi-annually and