Seagate 2004 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2004 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Table of Contents

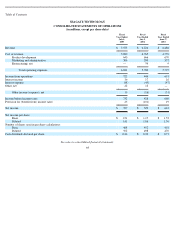

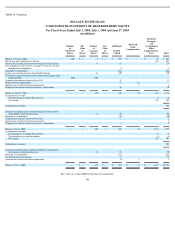

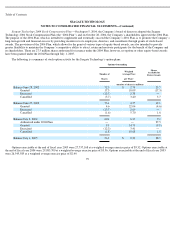

SEAGATE TECHNOLOGY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

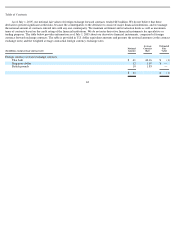

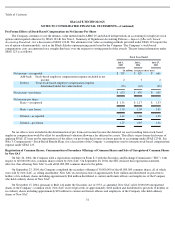

Pro Forma Effects of Stock-Based Compensation on Net Income Per Share

The Company continues to use the intrinsic value method under APBO 25 and related interpretations in accounting for employee stock

options until required otherwise by SFAS 123-R. See Note 1, Summary of Significant Accounting Policies— Impact of Recently Issued

Accounting Standards

, for a discussion of SFAS 123-R. The alternative fair-value accounting methods provided under SFAS 123 require the

use of option valuation models, such as the Black-Scholes option-pricing model used by the Company. The Company’s stock-based

compensation costs are amortized on a straight-line basis over the respective vesting periods of the awards. The pro forma information under

SFAS 123 is as follows:

No tax effects were included in the determination of pro forma net income because the deferred tax asset resulting from stock-based

employee compensation would be offset by an additional valuation allowance for deferred tax assets. The effects on pro forma disclosures of

applying SFAS 123 may not be representative of the effects on pro forma disclosures in future periods or accounting under SFAS 123-R. See

Note 3, Compensation

—Stock-Based Benefit Plans, for a discussion of the Company’s assumptions used to estimate stock-

based compensation

expense under SFAS 123.

Registration of Common Shares, Consummation of Secondary Offerings of Common Shares and Sale of Unregistered Common Shares

by New SAC

Fiscal Years Ended

July 1,

2005

July 2,

2004

June 27,

2003

(in millions, except per share data)

Net income

—

as reported

$

707

$

529

$

641

Add-back: Stock-based employee compensation expense included in net

income

2

3

2

Deduct: Total stock-based employee compensation expense

determined under fair value method

(76

)

(62

)

(38

)

Net income

—

pro forma

$

633

$

470

$

605

Net income per share:

Basic

—

as reported

$

1.51

$

1.17

$

1.53

Basic

—

pro forma

1.35

1.04

1.45

Diluted

—

as reported

1.41

1.06

1.36

Diluted

—

pro forma

1.27

0.95

1.30

On July 20, 2004, the Company filed a registration statement on Form S-3 with the Securities and Exchange Commission (“SEC”) with

respect to 60,000,000 of its common shares owned by New SAC. On September 20, 2004, the SEC declared this registration statement

effective, thus allowing New SAC to sell all 60,000,000 common shares to the public.

On September 23, 2004, the Company completed the secondary offering of 30,000,000 of the 60,000,000 common shares, all of which

were sold by New SAC, as selling shareholder. New SAC received proceeds of approximately $411 million and distributed its proceeds to

holders of its ordinary shares including approximately $66 million distributed to current and former officers and employees of the Company

who hold ordinary shares of New SAC.

On November 15, 2004, pursuant to Rule 144 under the Securities Act of 1933, as amended, New SAC sold 13,000,000 unregistered

shares of the Company’s common stock. New SAC received proceeds of approximately $182 million and distributed its proceeds to holders of

its ordinary shares including approximately $29 million to current and former officers and employees of the Company who hold ordinary

shares of New SAC.

72