Seagate 2004 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2004 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Table of Contents

Risk Factors

Risks Related to Our Business

Competition—Our industry is highly competitive and our products have experienced significant price erosion and market share

variability.

Even during periods when demand is stable, the disc drive industry is intensely competitive and vendors typically experience substantial

price erosion over the life of a product. Our competitors have historically offered existing products at lower prices as part of a strategy to gain

or retain market share and customers, and we expect these practices to continue. We may need to reduce our prices to retain our market share,

which could adversely affect our results of operations. Based on our recent experience in the industry with respect to new product

introductions, we believe that the rate of growth in areal density, or the storage capacity per square inch on a disc, is slowing from its previous

levels. This trend may contribute to increased average price erosion. To the extent that historical price erosion patterns continue, product life

cycles may lengthen, our competitors may have more time to enter the market for a particular product and we may be unable to offset these

factors with new product introductions at higher average prices. A second trend that may contribute to increased average price erosion is the

growth of sales to distributors that serve producers of non-branded products in the personal storage sector. These customers generally have

limited product qualification programs, which increase the number of competing products available to satisfy their demand. As a result,

purchasing decisions for these customers are based largely on price and terms. Any increase in our average price erosion would have an

adverse effect on our result of operations.

Moreover, a significant portion of our success in the past has been a result of increasing our market share at the expense of our

competitors. Our market share for our products can be negatively affected by our customers’

diversifying their sources of supply as the slowing

rate of growth in areal density has resulted in longer product cycles and more time for our competitors to enter the market for particular

products. When our competitors successfully introduce product offerings, which are competitive with our recently introduced new products,

our customers may quickly diversify their sources of supply. Any significant decline in our market share would adversely affect our results of

operations.

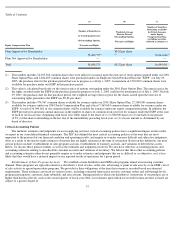

Principal Competitors—We compete with both independent manufacturers, whose primary focus is producing technologically

advanced disc drives, and captive manufacturers, who do not depend solely on sales of disc drives to maintain their profitability.

We have experienced and expect to continue to experience intense competition from a number of domestic and foreign companies,

including other independent disc drive manufacturers and large captive manufacturers such as:

The term “independent” in this context refers to manufacturers that primarily produce disc drives as a stand-alone product, and the term

“captive” refers to disc drive manufacturers who themselves or through affiliated entities produce complete computer or other systems that

contain disc drives or other information storage products. Captive manufacturers are formidable competitors because they have the ability to

determine pricing for complete systems without regard to the margins on individual components. Because components other than disc drives

generally contribute a greater portion of the operating margin on a complete computer system than do disc drives, captive manufacturers do not

necessarily need to realize a profit on the disc drives included in a computer system and, as a result, may be willing to sell disc drives to third

parties at very low margins. Many captive manufacturers are also formidable competitors because they have more substantial resources than we

do. In addition, Hitachi Global Storage Technologies (together with affiliated entities) and Samsung Electronics Incorporated also sell other

products to our customers, including critical components like flash memory,

40

Independent

Captive

Maxtor Corporation

Fujitsu Limited

Western Digital Corporation

Hitachi Global Storage

Technologies

Cornice Inc.

Samsung Electronics Incorporated

GS Magicstor Inc.

Toshiba Corporation