ICICI Bank 2007 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2007 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

33

Annual Report 2006-2007

FINANCIAL SECTOR OVERVIEW

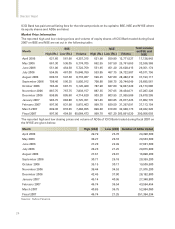

The financial sector mirrored the developments in the Indian economy. Credit growth was robust, given

the increase in economic activity. Non-food credit increased by 28.0% in fiscal 2007 compared to 30.8%

in fiscal 2006. Based on data published by RBI, during April-December 2006, industry accounted for

38.5% of non-food credit, retail credit for 26.4%, agriculture and allied activities for 12.2%, trade for

6.1%, real estate for 2.4% and other sectors for the balance 14.4%. The credit-deposit ratio increased

from about 70.0% in April 2006 to about 74.0% in March 2007. The incremental credit-deposit ratio was

about 86.0% for fiscal 2007 compared to about 102.0% for fiscal 2006, on account of robust growth in

deposits during fiscal 2007. Deposits of the banking system grew by Rs. 5,130.05 billion, or 24.2%, in

fiscal 2007 compared to 17.4% in fiscal 2006. In response to the increase in the cash reserve ratio and

the reverse repo rate and the liquidity conditions, banks have increased their lending and deposit rates.

The average yield on 10-year Government securities increased from 7.1% in fiscal 2006 to 7.8% in fiscal

2007.

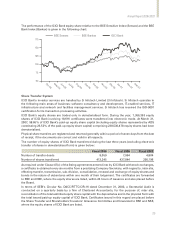

Growth in both the life and non-life insurance markets was significant. First year retail premium

underwritten in the life insurance sector recorded a growth of 91.9% (on weighted received premium

basis) to reach Rs. 402.77 billion in fiscal 2007 with the private sector’s retail market share (on weighted

received premium basis) increasing from 34.2% in fiscal 2006 to 35.5% in fiscal 2007. Gross premium in

the non-life insurance sector (excluding Export Credit Guarantee Corporation of India Limited) grew by

22.4% to Rs. 250.02 billion in fiscal 2007 with the private sector’s market share increasing from 26.6% in

fiscal 2006 to 34.9% in fiscal 2007. Total assets under management of mutual funds grew by 40.8% from

Rs. 2,318.62 billion at March 31, 2006 to Rs. 3,263.88 billion at March 31, 2007.

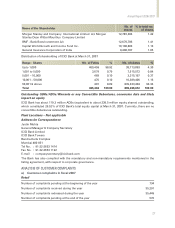

The banking sector witnessed several important regulatory developments. In April 2007, RBI issued final

guidelines for the implementation of a revised Basel II capital adequacy framework that would be effective

year-end fiscal 2008 for banks like us. The guidelines include an increase in the minimum Tier-I CAR from

4.5% to 6.0% and introduction of capital for operational risk. The guidelines prescribe a 75.0% weight

for retail credit exposure and rating based differential risk weights for other credit exposures, including

on undrawn commitments. During the fiscal year, RBI increased the general provisioning requirement

on standard advances in specific sectors to 1.0% from 0.4%. In January 2007, RBI further increased

the general provisioning requirement for real estate sector loans (excluding residential housing loans),

credit card receivables, loans and advances qualifying as capital market exposure, personal loans and

exposures to non-deposit taking systemically important non-banking financial companies to 2.0%. In

April 2007, RBI issued revised guidelines on lending to the priority sector. The guidelines are effective

fiscal 2008 and link priority sector lending targets to adjusted net bank credit. In April 2007, RBI issued

draft guidelines aimed at permitting banks and primary dealers to begin transactions in credit default

swaps. RBI also issued modified consolidated supervision norms limiting a bank’s consolidated capital

market exposure limit at 40.0% of its consolidated net worth and restricting direct exposure to 20.0% of

the consolidated net worth.

The Indian financial sector is rapidly moving towards international benchmarks, with increasing efficiency,

transparency and dynamism. Given the robust growth prospects in India, the financial sector has a

crucial role to play in the development of the economy. Broad-based reforms have made the banking

sector competitive and have positioned it well to support sustained economic growth.

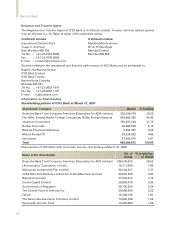

ORGANISATION STRUCTURE

Our organisation structure is designed to be flexible and customer-focused, while seeking to ensure

effective control and supervision and consistency in standards across the organisation and align all

areas of operations to overall organisational objectives. The organisation structure is divided into six

principal groups – Retail Banking, Wholesale Banking, International Banking, Rural, Micro-Banking and

Agri-Business, Government Banking and Corporate Centre.