Foot Locker 2007 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2007 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

51

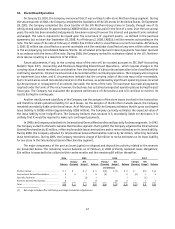

Of the unrecognized tax benefits, $68 million would, if recognized, affect the Company’s annual effective tax

rate. It is reasonably possible that the liability associated with the Company’s unrecognized tax benefits will increase

or decrease within the next twelve months. These changes may be the result of ongoing audits or the expiration

of statutes of limitations. Settlements could increase earnings in an amount ranging from $0 to $10 million based

on current estimates. Audit outcomes and the timing of audit settlements are subject to significant uncertainty.

Although management believes that adequate provision has been made for such issues, the ultimate resolution of such

issues could have an adverse effect on the earnings of the Company. Conversely, if these issues are resolved favorably

in the future, the related provision would be reduced, generating a positive effect on earnings. Due to the uncertainty

of amounts and in accordance with its accounting policies, the Company has not recorded any potential impact of these

settlements.

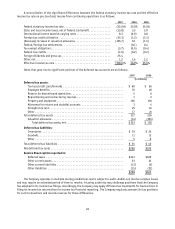

21. Financial Instruments and Risk Management

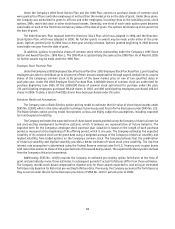

Foreign Exchange Risk Management — Derivative Holdings Designated as Hedges

The Company operates internationally and utilizes certain derivative financial instruments to mitigate its foreign

currency exposures, primarily related to third party and intercompany forecasted transactions.

For a derivative to qualify as a hedge at inception and throughout the hedged period, the Company formally

documents the nature of the hedged items and the relationships between the hedging instruments and the hedged items,

as well as its risk-management objectives, strategies for undertaking the various hedge transactions, and the methods

of assessing hedge effectiveness and hedge ineffectiveness. Additionally, for hedges of forecasted transactions, the

significant characteristics and expected terms of a forecasted transaction must be specifically identified, and it must

be probable that each forecasted transaction would occur. If it were deemed probable that the forecasted transaction

would not occur, the gain or loss would be recognized in earnings immediately. No such gains or losses were recognized

in earnings during 2007. Derivative financial instruments qualifying for hedge accounting must maintain a specified

level of effectiveness between the hedging instrument and the item being hedged, both at inception and throughout

the hedged period, which management evaluates periodically.

The primary currencies to which the Company is exposed are the euro, the British Pound, and the Canadian Dollar.

For option and forward foreign exchange contracts designated as cash flow hedges of the purchase of inventory, the

effective portion of gains and losses is deferred as a component of accumulated other comprehensive loss and is

recognized as a component of cost of sales when the related inventory is sold. The amount classified to cost of sales

related to such contracts was not significant in 2007. The ineffective portion of gains and losses related to cash flow

hedges recorded to earnings in 2007 was not significant. When using a forward contract as a hedging instrument,

the Company excludes the time value from the assessment of effectiveness. At each year-end, the Company had not

hedged forecasted transactions for more than the next twelve months, and the Company expects all derivative-related

amounts reported in accumulated other comprehensive loss to be reclassified to earnings within twelve months.

The Company has numerous investments in foreign subsidiaries, and the net assets of those subsidiaries are

exposed to foreign exchange-rate volatility. In 2005, the Company hedged a portion of its net investment in its

European subsidiaries. The Company entered into a 10-year cross currency swap, effectively creating a €100 million

long-term liability and a $122 million long-term asset. During the term of this transaction, the Company will remit

to and receive from its counterparty interest payments based on rates that are reset monthly equal to one-month

EURIBOR and one-month U.S. LIBOR rates, respectively. In 2006, the Company hedged a portion of its net investment in

its Canadian subsidiaries. The Company entered into a 10-year cross currency swap, creating a CAD $40 million liability

and a $35 million long-term asset. During the term of this transaction, the Company will remit to and receive from its

counterparty interest payments based on rates that are reset monthly equal to one-month CAD B.A. and one-month

U.S. LIBOR rates, respectively.

The Company has designated these hedging instruments as hedges of the net investments in foreign subsidiaries,

and will use the spot rate method of accounting to value changes of the hedging instrument attributable to currency

rate fluctuations. As such, adjustments in the fair market value of the hedging instrument due to changes in the spot

rate will be recorded in other comprehensive income and are expected to offset changes in the euro-denominated net

investment. Amounts recorded to foreign currency translation within accumulated other comprehensive loss will remain

there until the net investment is disposed of. The amount recorded within the foreign currency translation adjustment

included in accumulated other comprehensive loss on the Consolidated Balance Sheet decreased shareholders’ equity