Foot Locker 2007 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2007 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

39

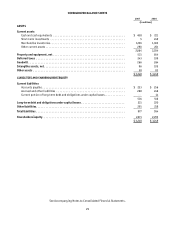

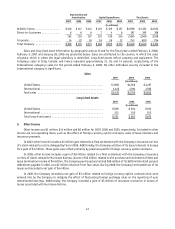

Additionally, in the third quarter of 2007, the Company identified 66 unproductive stores for closure. Accordingly,

the Company evaluated the recoverability of long-lived assets considering the revised estimated future cash flows. The

Company recorded an additional non-cash impairment charge of $7 million as a result of this analysis. Of the total stores

identified for closure in the third quarter of 2007, 13 will remain in operation as the Company was able to negotiate more

favorable lease terms. Exit costs related to 33 stores which closed during 2007, comprising primarily lease termination

costs of $4 million, were recognized in accordance with SFAS No. 146, “Accounting for Costs Associated with Exit or

Disposal Activities.” During 2008, the Company currently expects to close the remaining 20 unproductive stores prior

to normal lease expiration, depending on the Company’s success in negotiating agreements with its landlords. The lease

exit costs associated with these remaining closures is expected to total $5 million to $10 million. These charges will

be recorded during 2008 in accordance with SFAS No. 146. The cash impact of the 2008 store closings is expected to be

minimal, as the related cash lease costs are expected to be offset by associated inventory reductions. Under SFAS No.

144, store closings may constitute discontinued operations if migration of customers and cash flows are not expected.

The Company has concluded that no store closings have met the criteria for discontinued operations treatment.

Included in the Athletic Stores division profit for 2006 is an impairment charge of $17 million related to the

Company’s European operations to write-down long-lived assets in 69 stores to their estimated fair value. During 2006,

division profit declined primarily due to the fashion shift from higher priced marquee footwear to lower priced low-

profile footwear styles and a highly competitive retail environment, particularly for the sale of low-profile footwear

styles. The charge was comprised primarily of stores located in the U.K. and France.

3. Staff Accounting Bulletin No. 108

In September 2006, the SEC issued Staff Accounting Bulletin No. 108 (“SAB 108”) “Considering the Effects of

Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements,” that provides

interpretive guidance on how the effects of the carryover or reversal of prior year misstatements should be considered

in quantifying a current year misstatement. There are two widely recognized methods for quantifying the effects

of financial statement misstatements: the “rollover” or income statement method and the “iron curtain” or balance

sheet method. The SEC staff believes that registrants should quantify errors using both a balance sheet and an income

statement approach (“dual method”) and evaluate whether either approach results in quantifying a misstatement

that, when all relevant quantitative and qualitative factors are considered, is material. The Company had historically

evaluated uncorrected misstatements using the “rollover” method. SAB 108 permits companies to apply its provisions

initially by either (i) restating prior financial statements as if the provisions had always been applied or (ii) recording

the cumulative effect of initially applying SAB 108 as adjustments to the carrying value of assets and liabilities as of

the beginning of 2006 with an offsetting adjustment recorded to the opening balance of shareholders’ equity.

The Company believes its prior period assessments of uncorrected misstatements and the conclusions reached

regarding its quantitative and qualitative assessments of materiality of such items, both individually and in

the aggregate, were appropriate. These items did not significantly affect 2005 as these items originated in earlier

periods. In accordance with SAB 108, the Company has adjusted its opening retained earnings for 2006 for the items

described below.

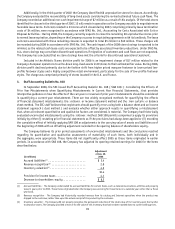

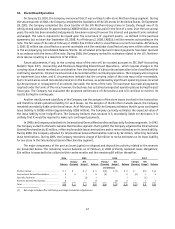

(in millions)

Adjustment

at Jan. 29,

2006

Accrued liabilities(1) . . . . . . . . . . . . . . . . . . . . . . . . $ 3.4

Revenue recognition(2) . . . . . . . . . . . . . . . . . . . . . . 2.8

Inventory valuation(3) . . . . . . . . . . . . . . . . . . . . . . . 4.2

10.4

Provision for income taxes . . . . . . . . . . . . . . . . . . . 4.1

Decrease to shareholders’ equity . . . . . . . . . . . . . . . $ 6.3

(1) Accrued liabilities – The Company understated its accrued liabilities for certain items, such as telecommunications, utilities and property

taxes in years prior to 2003. These items originated when the Company was accruing for these items on a calendar year rather than a fiscal

year basis.

(2) Revenue recognition – The Company had historically recorded revenue from its catalog and Internet operations when the product was

shipped to the customer, rather than upon the actual receipt of the product by the customer.

(3) Inventory valuation – The Company did not properly recognize the permanent reduction of the retail value of its inventory upon the transfer

to clearance stores. The Company provided a reserve for the value of this inventory that had not been marked down to current selling prices.