Thrifty Car Rental 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 Thrifty Car Rental annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

qualified intermediary) vehicles being disposed of with vehicles being purchased allowing the

Company to carry-over the tax basis of vehicles sold to replacement vehicles, thereby deferring

taxable gains from vehicle dispositions. In addition, the Company has historically elected to

utilize accelerated or “bonus” depreciation methods on its vehicle inventories in order to defer

its cash liability for U.S. income taxes.

As a result of significant reductions in vehicle inventory levels during 2009 and 2010, and low

tax basis in existing vehicle inventories as a result of accelerated depreciation in prior periods,

the Company expected to realize a reversal of prior income tax deferrals during 2010, and

accordingly, made estimated federal and state income tax payments of $74.7 million during

2010. In September 2010, Congress passed and the President signed into law the Small

Business Jobs and Credit Act of 2010 (the “Small Business Act”), which extended 50% bonus

depreciation allowances for assets placed in service in 2010, retroactively to the first of the

year. In December 2010, Congress passed and the President signed into law The Tax Relief,

Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (the “Tax Relief Act”)

which increased the bonus depreciation allowance to 100% for assets placed in service from

September 9, 2010 through December 31, 2011, as well as provided for 50% bonus

depreciation for assets placed in service in 2012. With the enactment of the Small Business

and Tax Relief Acts, the Company’s 2010 cash tax liability is substantially reduced and the

Company has a refundable overpayment for the excess estimated tax payments made in 2010.

The Company’s ability to continue to defer the reversal of prior period tax deferrals will depend

on a number of factors, including the size of the Company’s fleet, as well as the availability of

accelerated depreciation methods in future years. Accordingly, the Company may make

material cash tax payments in future periods.

During 2009, the Company utilized all of the remaining federal net operating loss (“NOL”) and

has no remaining federal NOL carryforwards. The Company has net operating loss

carryforwards available in certain states to offset future state taxable income. A valuation

allowance of approximately $0.1 million existed at both December 31, 2010 and 2009, for state

net operating losses. At December 31, 2010, DTG Canada has net operating loss

carryforwards of approximately $67.9 million available to offset future taxable income in

Canada. The Canadian NOLs will begin expiring in 2014 and will continue to expire through

2030. Valuation allowances have been established for the total estimated future tax effect of

the Canadian net operating losses and other deferred tax assets.

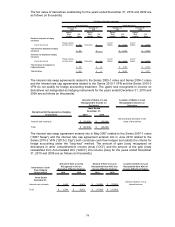

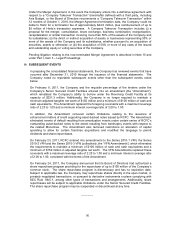

The Company’s effective tax rate differs from the maximum U.S. statutory income tax rate. The

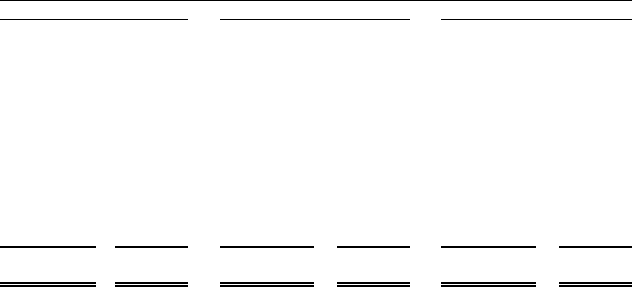

following summary reconciles taxes at the maximum U.S. statutory rate with recorded taxes:

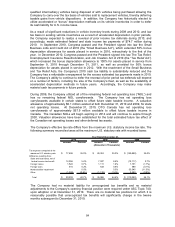

Amount Percent Amount Percent Amount Percent

(Amounts in Thousands)

Tax expense computed at the

maximum U.S. statutory rate

77,496$ 35.0% 28,353$ 35.0% (159,880)$ 35.0%

Difference resulting from:

State and local taxes, net of

federal income tax benefit

12,056 5.4% 7,007 8.6% (12,117) 2.7%

Foreign losses

1,522 0.7% 1,111 1.4% 7,701 (1.7%)

Foreign taxes

416 0.2% 633 0.8% 588 (0.1%)

Nondeductible impairment

- 0.0% - 0.0% 50,045 (11.0%)

Other

(1,288) (0.6%) (1,118) (1.4%) 3,580 (0.8%)

Total

90,202$ 40.7% 35,986$ 44.4% (110,083)$ 24.1%

Year Ended December 31,

2010 2009 2008

The Company had no material liability for unrecognized tax benefits and no material

adjustments to the Company’s opening financial position were required under ASC Topic 740,

upon adoption or at December 31, 2010. There are no material tax positions for which it is

reasonably possible that unrecognized tax benefits will significantly change in the twelve

months subsequent to December 31, 2010.

84