Tesco 2015 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2015 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

Area of focus How our audit addressed the area of focus

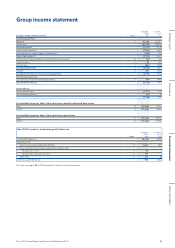

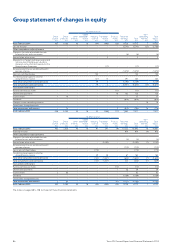

Commercial income – impact on prior periods

Refer to page 37 (Audit Committee Report), page 88 (Accounting

Policies) and page 99 (notes).

The Group has stated in its financial statements that commercial

income recognised in previous periods was overstated by £53

million in 2013/14 and by £155 million in the periods prior to

2013/14. The directors have concluded that it is not possible to

determine the exact amounts relating to prior periods and exactly

which periods are affected. Management has however produced

a quantitative and qualitative estimate of the amounts relating

to prior periods.

Having estimated the amounts of potential misstatement relating

to prior periods, the directors then assessed whether these

amounts are material such that the prior period financial

statements would require restatement. The directors concluded

that the amounts relating to prior periods, whilst significant, were

not, from an accounting perspective, material and consequently

that it is not necessary to restate the 2013/14 financial statements.

We challenged and evaluated management’s quantitative and

qualitative analysis of amounts relating to prior periods and, whilst

judgemental, we considered that assessment to be reasonable.

The estimated impact on 2013/14 profits was £53 million, which was

below our profit based materiality of £150 million that we

determined applicable for the 2013/14 audit. The estimated impact

on the 22 February 2014 and 23 February 2013 balance sheets was

£208 million and £155 million respectively, both of which are less

than 0.5% of the Group’s total assets at each respective period end.

The basis on which we considered materiality relating to prior period

items is explained further below.

After considering carefully the nature and the quantum of the

estimated amounts relating to prior periods we concurred with the

directors that these amounts, whilst significant, were not material

and the prior period financial statements did not require restating.

The estimated impact on prior periods has been charged to the

income statement in the current period and the Group has

separately identified this as a one-off item. We concurred with this

accounting treatment and are supportive of the detailed disclosures

made in the Annual Report about the impact of the misstatement on

the prior periods’ financial statements.

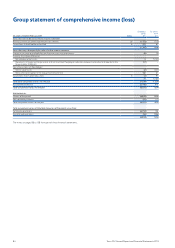

Impairment of property, plant and equipment

Refer to page 37 (Audit Committee Report), page 88 (Accounting

Policies) and page 108 (notes).

The directors have recorded an impairment charge of £4,292

million against the carrying value of property, plant and

equipment across the Group.

We focused on this area because the determination of whether

or not an impairment charge for property, plant and equipment

was necessary involved significant judgements by the directors

about the future results of the business and assessment of future

plans for the Group’s property portfolio in a number of territories.

In particular we focused on the reasonableness and impact of key

assumptions including:

• the cash flow forecasts derived from internal forecasts and

the assumptions around the future performance;

• the discount rate and the long term growth rate including

the assessment of risk factors and growth expectations

of the relevant territory; and

• the assumptions used in the valuations prepared to support

the fair value of certain assets and also the assessment of

the external valuers as management’s expert.

We evaluated management’s impairment calculations in local

territories, assessing the future cash flow forecasts used in the

models, and the process by which they were drawn up, including

comparing them to the latest Board approved budgets, and

we tested the mechanics of the underlying calculations. We

understood and challenged:

• the assumptions used in the Group’s five-year Plan and the

long term growth rates by comparing them to economic and

industry forecasts;

• the discount rate by assessing the cost of capital and other

inputs and comparable organisations; and

• the assumptions used by the external valuers to determine

the fair market value of the assets.

In performing the above work we utilised our specialist forecasting

and valuations knowledge to provide challenge and external market

data points to assess the reasonableness of the assumptions used

by management.

We performed sensitivity analysis around the key drivers of growth

rates within the cash flow forecasts to ascertain the extent of

change in those assumptions that either individually or collectively

would be required for the assets to be further impaired and also

considered the likelihood of such a movement in those key

assumptions arising.

Whilst recognising that cash flow forecasting, impairment modelling

and property valuations are all inherently judgemental, we concluded

that the assumptions used by management were within an acceptable

range of reasonable estimates.

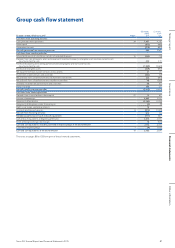

77Tesco PLC Annual Report and Financial Statements 2015

Other informationGovernance Financial statementsStrategic report