Spirit Airlines 2012 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2012 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

Notes to Financial Statements—(Continued)

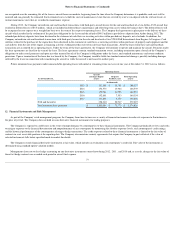

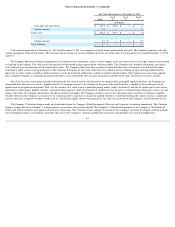

The Company’s principal stockholders provided certain consulting services to the Company for a management fee of $0.8 million in 2010 . For the year ended

December 31, 2011 , the Company expensed $0.3 million related to these consulting services. There were no management fees paid in 2012 .

The Company leases various types of equipment and property, primarily aircraft, spare engines and airport facilities under leases, which expire in various years

through 2032 . Lease terms are generally 3 to 12 years for aircraft and up to 20 years for other leased equipment and property.

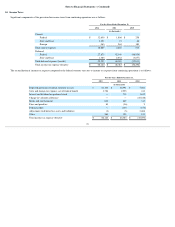

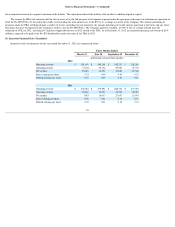

Total rental expense for all leases charged to operations for the years ended 2012 , 2011 , and 2010 was $172.4 million , $139.1 million , and $122.7 million ,

respectively. Total rental expense charged to operations for aircraft and engine operating leases for the years ended December 31, 2012 , 2011 , and 2010 was $143.6

million , $116.5 million , and $101.3 million , respectively.

Some of the Company’s master lease agreements provide that the Company pays maintenance reserves to aircraft lessors to be held as collateral in advance of the

Company’s required performance of major maintenance activities. Some maintenance reserve payments are fixed contractual amounts, while others are based on actual

flight hours. Fixed maintenance reserve payments for these aircraft and related flight equipment, including estimated amounts for contractual price escalations, will be

approximately $10.3 million in 2013 , $10.6 million in 2014 , $11.0 million in 2015 , $11.4 million in 2016 , $11.1 million in 2017 , and $40.4 million in 2018 and beyond .

These lease agreements provide that maintenance reserves are reimbursable to the Company upon completion of the maintenance event in an amount equal to the lesser of

(1) the amount of the maintenance reserve held by the lessor associated with the specific maintenance event or (2) the qualifying costs related to the specific maintenance

event. Substantially all of these maintenance reserve payments are calculated based on a utilization measure, such as flight hours or cycles, and are used solely to

collateralize the lessor for maintenance time run off the aircraft until the completion of the maintenance of the aircraft.

At lease inception and at each balance sheet date, the Company assesses whether the maintenance reserve payments required by the master lease agreements are

substantively and contractually related to the maintenance of the leased asset. Maintenance reserve payments that are substantively and contractually related to the

maintenance of the leased asset are accounted for as maintenance deposits. Maintenance deposits expected to be recovered from lessors are reflected as prepaid maintenance

deposits in the accompanying balance sheets. When it is not probable the Company will recover amounts currently on deposit with a lessor, such amounts are expensed as

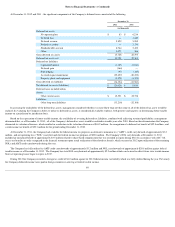

supplemental rent. As of December 31, 2012 and 2011 , the Company had aircraft maintenance deposits of $198.5 million and $168.8 million , respectively, on its balance

sheets of which $76.1 million and $48.2 million , respectively, are included within other current assets on its balance sheets. The Company has concluded that these prepaid

maintenance deposits are probable of recovery primarily due to the rate differential between the maintenance reserve payments and the expected cost for the related next

maintenance event that the reserves serve to collateralize.

The Company’s master lease agreements also provide that most maintenance reserves held by the lessor at the expiration of the lease are nonrefundable to the

Company and will be retained by the lessor. Consequently, any usage-based maintenance reserve payments after the last major maintenance event are not substantively

related to the maintenance of the leased asset and therefore are accounted for as contingent rent. The Company accrues for contingent rent beginning when it becomes

probable and reasonably estimable the Company will incur such nonrefundable maintenance reserve payments. The Company makes certain assumptions at the inception of

the lease and at each balance sheet date to determine the recoverability of maintenance deposits. These assumptions are based on various factors such as the estimated time

between the maintenance events, the date the aircraft is due to be returned to the lessor, and the number of flight hours the aircraft is estimated to be utilized before it is

returned to the lessor. The Company expensed $2.0 million , $1.5 million , and $0.0 million as supplemental rent during 2012 , 2011 , and 2010 , respectively. Maintenance

reserves held by lessors that are refundable to the Company at the expiration of the lease are accounted for as prepaid maintenance deposits on the balance sheet when they

are paid.

At December 31, 2012 , the Company had its entire fleet of 45 aircraft and eight

spare engines financed under operating leases with lease term expiration dates ranging

from 2016 to 2024 . Five of the leased aircraft have variable rent payments, which fluctuate based on changes in LIBOR (London Interbank Offered Rate). The Company

has the option to renew 17 of the leases for three -year periods with contractual notice required in the 10 th year. 16

of the aircraft leases and all of the engine leases were the

result of sale-lease-back transactions. Deferred gains or losses from sale-lease-back transactions are amortized over the term of the lease as a reduction in rent or additional

rent, respectively. Losses are deferred when the fair value of the aircraft or engine is higher than the price it was sold for, in substance, a prepayment of rent. A loss on

disposal is recorded at the time of sale for the excess of the carrying amount over the fair value of the aircraft or engine. The costs of returning aircraft to lessors, or lease

return conditions, are accounted for in a manner similar to the accounting for contingent rent. These costs

76

11.

Leases and Prepaid Maintenance Deposits