Spirit Airlines 2012 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2012 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

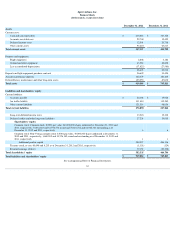

Notes to Financial Statements—(Continued)

restricted stock awards, stock option awards, and performance share awards. Restricted stock awards are valued at the fair value of the shares on the date of grant if vesting

is based on a service or a performance condition. To the extent a market price was not available, the fair value of stock awards was estimated using a discounted cash flow

analysis based on management’s estimates of revenue, driven by assumed market growth rates, and estimated costs as well as appropriate discount rates. These estimates are

consistent with the plans and estimates that management uses to manage the Company’s business. The fair value of share option awards is estimated on the date of grant

using the Black-Scholes valuation model. The fair value of performance share awards is estimated through the use of a Monte Carlo simulation model. See Note 8 for

additional information.

Concentrations of Risk

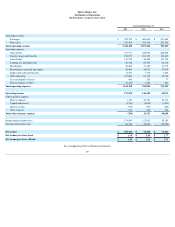

The Company’s business has been, and may continue to be, adversely affected by increases in the price of aircraft fuel, the volatility of the price of aircraft fuel, or

both. Aircraft fuel was the Company’s single largest expenditure representing approximately 41% , 42% , and 35% of total operating expenses in 2012 , 2011 , and 2010 ,

respectively.

The Company’s operations are largely concentrated in the southeast United States with Fort Lauderdale being the highest volume fueling point in the system. Gulf

Coast Jet indexed fuel is the basis for a substantial majority of the Company’s fuel consumption. Any disruption to the oil production or refinery capacity in the Gulf Coast,

as a result of weather or any other disaster or disruptions in supply of jet fuel, dramatic escalations in the costs of jet fuel, and/or the failure of fuel providers to perform

under fuel arrangements for other reasons could have a material adverse effect on the Company’s financial condition and results of operations.

The Company’s operations will continue to be vulnerable to weather conditions (including hurricane season or snow and severe winter weather), which could disrupt

service, create air traffic control problems, decrease revenue, and increase costs.

Due to the relatively small size of the fleet and high utilization rate, the unavailability of one or more aircraft and resulting reduced capacity could have a material

adverse effect on the Company’s business, results of operations, and financial condition.

The Company has three union-represented employee groups that together represent approximately 54% and 52% of all employees at December 31, 2012 and 2011 ,

respectively. A strike or other significant labor dispute with the Company’s unionized employees is likely to adversely affect the Company’s ability to conduct business.

Additional disclosures are included in Note 15.

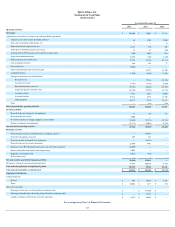

In May 2011, the FASB issued Accounting Standards Update No. 2011-04, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements

in U.S. GAAP and International Financial Reporting Standards (Topic 820)—Fair Value Measurement (ASU 2011-04). This ASU provides a consistent definition of fair

value and ensures the fair value measurement and disclosure requirements are similar between GAAP and International Financial Reporting Standards. ASU 2011-04

changes certain fair value measurement principles and enhances the disclosure requirements particularly for Level 3 fair value measurements. ASU 2011-04 requires public

and non-public companies to disclose the unobservable inputs that are significant to the fair value measurement. Public companies are now required to quantitatively

disclose the unobservable inputs used in their Level 3 measurements. ASU 2011-04 provides examples of information companies might provide to comply with the

disclosure requirements. The requirements include: (1) a description of the group responsible for valuation policies and procedures, to whom the group reports and the types

of internal reporting procedures in place (e.g., interaction between the group and risk management or the audit committee to assess fair value measurements); (2) a

description of the frequency and methods for calibration, back testing and other testing procedures used to evaluate pricing models; (3) a description of the process for

analyzing changes in fair value measurements from period to period; (4) a description of the methods used to evaluate pricing information provided by third-

party brokers or

pricing services; (5) a description of the methods used to develop and substantiate the unobservable inputs used in a fair value measurement; and (6) a narrative description

of the sensitivity of recurring Level 3 fair value measurements to changes in the unobservable inputs used, if changing those inputs would significantly affect the fair value

measurement. On January 1, 2012, the Company adopted ASU 2011-04.

The adoption of ASU 2011-04 resulted in qualitative presentation changes to the Company's disclosures related to fair value measurements as disclosed in Note 8.

These changes were primarily additional language regarding the Company's valuation policies and procedures including the frequency of valuation and testing of valuation

models as well as the sensitivity of the Company's model to changes in unobservable inputs.

In December 2011, the FASB issued amendments to Accounting Standards Update No. 2011-11, Balance Sheet (Topic 210); Disclosures about Offsetting Assets and

Liabilities

(ASU 2011-

11). The amendments in this update are designed to enhance disclosures by requiring improved information about financial instruments and derivative

instruments that are either

69

2.

Recent Accounting Developments