Spirit Airlines 2012 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2012 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

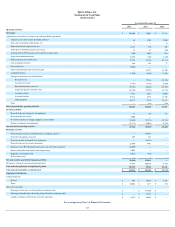

|

|

Notes to Financial Statements—(Continued)

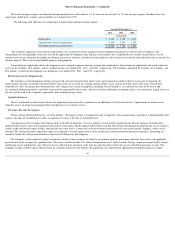

Frequent Flier Program

Flown Miles. The Company records a liability for mileage credits earned by passengers, including mileage credits for members with an insufficient number of mileage

credits to earn an award, under its FREE SPIRIT program based on the estimated incremental cost of providing free travel for credits that are expected to be redeemed.

Incremental costs include fuel, insurance, security, ticketing, and facility charges reduced by an estimate of fees required to be paid by the passenger when redeeming the

award.

Original Affinity Card Program. The Company also sells mileage credits to companies participating in the FREE SPIRIT program (or affinity card program). Under

the original affinity card program, funds received from the sale of mileage credits were accounted for as a multiple element arrangement and allocated to a marketing

component and a transportation component (mileage credits) using the residual method. The fair value of the transportation component was deferred and recognized ratably

as passenger revenue over the estimated period the transportation was expected to be provided which was estimated at 16 months . The difference between the funds

received and the fair value of the transportation component was recognized in non-ticket revenue at the time of sale as non-ticket marketing revenue. The marketing

component represented the Company’s compensation for use of its trademark, customer lists and placement of marketing materials to encourage application for credit cards.

Because there were no undelivered elements other than the mileage credits, the Company recorded the revenue from the marketing component when funds were received.

The Company also received bonuses from companies participating in the FREE SPIRIT program that are driven by the volume of the usage of the Company’s co-branded

credit cards. The Company recognized these bonuses as non-ticket revenue when payment was received (milestone method) as the milestones are substantive.

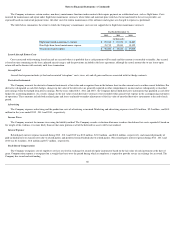

During the fourth quarter of 2010, the Company determined not to renew its agreement with the administrator of the FREE SPIRIT affinity credit card program at the

scheduled expiration in February 2011. In connection with that non-renewal, the Company entered into an agreement with the former administrator regarding the transition

of the program to a new provider and the remittance to the Company of compensation due to the Company for card members obtained through the Company’s marketing

services in the amount of $5.0 million , of which $4.6 million was recognized in the fourth quarter of 2010 and $0.4 million was recognized in the first quarter of 2011.

New Affinity Card Program. The Company entered into a new affinity card program that became effective April 1, 2011. The agreement calls for the marketing of a

co-branded Spirit credit card and the delivery of award miles over the five -year contract term. At the inception of the arrangement, the Company evaluated all deliverables

in the arrangement to determine whether they represent separate units of accounting using the criteria as set forth in ASU No. 2009-13. The Company determined the

arrangement had three separate units of accounting: (i) travel miles to be awarded, (ii) licensing of brand and access to member lists, and (iii) advertising and marketing

efforts. Under ASU No. 2009-13, arrangement consideration should be allocated based on relative selling price. At inception of the arrangement, the Company established

the relative selling price for all deliverables that qualified for separation. The manner in which the selling price was established was based on a hierarchy of evidence that the

Company considered. Total arrangement consideration was then allocated to each deliverable on the basis of the deliverable’s relative selling price. In considering the

hierarchy of evidence under ASU No. 2009-13, the Company first determined whether vendor specific objective evidence of selling price or third-party evidence of selling

price existed. It was determined by the Company that neither vendor specific objective evidence of selling price nor third-

party evidence existed due to the uniqueness of the

Company’s program. As such, the Company developed its best estimate of the selling price for all deliverables. For the award miles, the Company considered a number of

entity-specific factors when developing the best estimate of the selling price including the number of miles needed to redeem an award, average fare of comparable

segments, breakage, restrictions, and other charges. For licensing of brand and access to member lists, the Company considered both market-specific factors and entity-

specific factors including general profit margins realized in the marketplace/industry, brand power, market royalty rates, and size of customer base. For the advertising

element, the Company considered market-specific factors and entity-specific factors including, the Company’s internal costs (and fluctuations of costs) of providing

services, volume of marketing efforts, and overall advertising plan. Consideration allocated based on the relative selling price to both brand licensing and advertising

elements is recognized as revenue when earned and recorded in non-ticket revenue. Consideration allocated to award miles is deferred and recognized ratably as passenger

revenue over the estimated period the transportation is expected to be provided which is estimated at 16 months . The Company used entity-specific assumptions coupled

with the various judgments necessary to determine the selling price of a deliverable in accordance with the required selling price hierarchy. Changes in these assumptions

(e.g., cost of fare, number of miles to redeem awards, marketing plan, and approval rate of credit cards) could result in changes in the estimated selling prices. Determining

the frequency to reassess selling price for individual deliverables requires significant judgment. Mileage credits that expire under the terms of the Company's policy or are

not likely to be redeemed are collectively referred to as breakage. The Company estimates and recognizes breakage on its frequent flier miles in proportion to actual mileage

redemptions, in accordance with the redemption recognition method.

66