Radio Shack 2013 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2013 Radio Shack annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

44

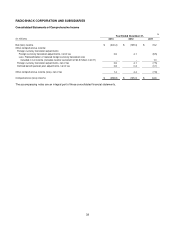

kiosks were transitioned to Sam’s Club by June 30, 2011.

We concluded that the cash flows from these kiosks were

eliminated from our ongoing operations. Therefore, the

results of these operations, net of income taxes, have been

presented as discontinued operations in our Consolidated

Statements of Income for all periods presented.

Net sales and operating revenues related to these

discontinued operations were $72.2 million, $426.5 million

and $408.8 million for 2013, 2012 and 2011, respectively.

The amount of loss before income taxes for these

discontinued operations was $7.9 million, $35.9 million and

$10.5 million for 2013, 2012 and 2011, respectively.

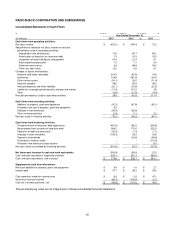

LIQUIDITY

We have experienced losses for the past two years,

primarily attributed to a downturn in our business, which

has impacted our overall liquidity. In response to our

liquidity needs and to continue execution of our Strategic

Plan, we entered into the 2018 Credit Agreement in

December 2013. It is our belief that this will provide the

financial flexibility needed to improve operating results and

provide sufficient liquidity to meet our obligations through

2014.

While we continue to execute our strategic plan and

proposed store closure program, which are designed to

improve operating results and control costs through

operational efficiency, we realize that there are significant

risks due to consumer acceptance of our efforts to

reposition the brand, revamp our product assortment and

reinvigorate our store experience as well as the competitive

nature of the consumer electronics industry.

As we execute the strategic turnaround plan and move

through 2014, we will be tightly managing our cash and

monitoring our liquidity position. We have implemented a

number of initiatives to conserve our liquidity position

including activities such as reducing our capital

expenditures, reducing discretionary spending and selling

surplus property. Many of the aspects of the plan involve

management’s judgments and estimates that include

factors that could be beyond our control and actual results

could differ from our estimates. These and other factors

could cause the strategic turnaround plan and the proposed

store closure program to be unsuccessful which could have

a material adverse effect on our operating results, financial

condition and liquidity.

Store Closure Program: On March 4, 2014, along with our

fourth quarter earnings release, we announced that we

intend to close up to 1,100 underperforming stores. This

program was driven by a comprehensive review of the

existing store base and selection of stores based upon

historical and projected financial performance, lease

termination costs, and impact to the market and nearby

stores. This proposed store closure program is expected to

preserve liquidity by avoiding operating losses and

generating cash by liquidating inventory in those stores.

This will be partially offset by lease termination payments

and liquidation costs. This program resulted in a non-cash

impairment charge of fixed assets in these stores of $11.2

million and inventory write down of $10.1 million, reflected

in the 2013 financial statements. The proposed store

closure program is subject to the consent of the lenders

under our 2018 Credit Agreement and 2018 Term Loan. If

we are unsuccessful in obtaining consent, we believe that

we have sufficient liquidity to meet our obligations through

2014.

NOTE 2 – SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES

Basis of Presentation: The consolidated financial

statements include the accounts of RadioShack

Corporation and all majority-owned domestic and foreign

subsidiaries. All intercompany accounts and transactions

are eliminated in consolidation.

Use of Estimates: The preparation of financial statements

in accordance with accounting principles generally

accepted in the United States requires us to make

estimates and assumptions that affect the reported

amounts of assets and liabilities, related revenues and

expenses, and the disclosure of gain and loss contingencies

at the date of the financial statements and during the periods

presented. We base these estimates on historical results and

various other assumptions believed to be reasonable, all of

which form the basis for making estimates concerning the

carrying values of assets and liabilities that are not readily

available from other sources. Actual results could differ

materially from those estimates.

Cash and Cash Equivalents: Cash on hand in stores,

deposits in banks, credit card receivables, and all highly

liquid investments with a maturity of three months or less at

the time of purchase are considered cash and cash

equivalents. We carry our cash equivalents at cost, which

approximates fair value because of the short maturity of the

instruments. The weighted-average annualized interest

rates were 0.2% and 0.2% at December 31, 2013 and

2012, respectively, for cash equivalents totaling $124.4

million and $408.2 million, respectively.

Outstanding checks in excess of deposits with these banks

totaled $8.0 million and $108.3 million at December 31,

2013 and 2012, respectively, and are classified as accounts

payable in the Consolidated Balance Sheets. The terms of

these bank accounts changed in connection with the

closing of our five-year, $585 million asset-based credit

agreement in December 2013. Prior to the closing of this

credit agreement, changes in these overdrafts were

classified in the Consolidated Statement of Cash Flows as

a financing activity. Subsequent to the closing of the credit

agreement, changes in these overdraft amounts have been

reported in the Consolidated Statements of Cash Flows as

an operating activity.

Restricted Cash: We have pledged cash as collateral for

standby and trade letters of credit issued to our general

liability insurance provider and certain other vendors. Since

December 31, 2013, substantially all of these letters of

credit have either expired or have been issued under our

asset-based revolving credit facility that expires in

December 2018. Restricted cash totaled $66.0 million and

$26.5 million at December 31, 2013 and 2012, respectively,

and is included in other current assets in our Consolidated

Balance Sheets.