Pizza Hut 2003 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2003 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

58.

of franchise contract rights which will be amortized over

thirty years, the typical term of a YGR franchise agreement

including renewals. Of the $212 million in trademarks/

brands approximately $191 million and $21 million

were assigned to the U.S. and International operating

segments, respectively. Of the remaining $38 million

in intangible assets, approximately $31 million and

$7 million were assigned to the U.S. and International

operating segments, respectively.

The $209 million in goodwill was assigned to the

U.S. operating segment. As we acquired the stock of

YGR, none of the goodwill is expected to be deductible

for income tax purposes.

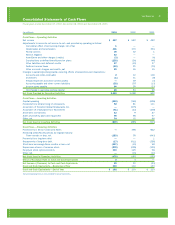

Liabilities assumed included approximately $48 million

of bank indebtedness that was paid off prior to the

end of the second quarter of 2002 and approximately

$11 million in capital lease obligations. We also assumed

approximately $168 million in present value of future rent

obligations related to three existing sale-leaseback agree-

ments entered into by YGR involving approximately 350

LJS units. As a result of liens held by the buyer/lessor on

certain personal property within the units, the sale-lease-

back agreements were accounted for as financings upon

acquisition. As discussed further in Note 14, two of these

sale-leaseback agreements were amended during 2003 and

are now being accounted for as operating leases.

As of the date of acquisition we recorded approxi-

mately $49 million of reserves (“exit liabilities”) related

to our plans to consolidate certain support functions,

and exit certain markets through store refranchisings and

closures, as presented in the table below. The consolida-

tion of certain support functions included the termination of

approximately 100 employees. Our remaining exit liabilities,

as well as amounts utilized through cash payments during

2003 and 2002, are presented below.

Lease and

Other

Severance Contract Other

Benefits Terminations Costs Total

Total reserve at

acquisition $ 13 $ 31 $ 5 $ 49

Amounts utilized in 2003 (5) (5) (3) (13)

Amounts utilized in 2002 (8) — (1) (9)

Total reserve as of

December 27, 2003 $ — $ 26 $ 1 $ 27

We expensed integration costs of approximately $4 million

in 2003 and $6 million in 2002 related to the acquisi-

tion. These costs were recorded as AmeriServe and

other charges (credits). See Note 7 for further discussion

regarding AmeriServe and other charges (credits).

The results of operations for YGR have been included

in our Consolidated Financial Statements since the date

of acquisition. If the acquisition had been completed as of

the beginning of the years ended December 28, 2002 and

December 29, 2001, pro forma Company sales and fran-

chise and license fees would have been as follows:

2002 2001

Company sales $ 7,139 $ 6,683

Franchise and license fees 877 839

The impact of the acquisition, including interest expense on

debt incurred to finance the acquisition, on net income and

diluted earnings per share would not have been significant in

2002 and 2001. The pro forma information is not necessarily

indicative of the results of operations had the acquisition

actually occurred at the beginning of each of these periods

nor is it necessarily indicative of future results.

ACCUMULATED OTHER COMPREHENSIVE INCOME

(LOSS)

note

5

Accumulated other comprehensive income (loss) includes:

2003 2002

Foreign currency translation adjustment $ (107) $ (176)

Minimum pension liability adjustment, net of tax (101) (71)

Unrealized losses on derivative instruments,

net of tax (2) (2)

Total accumulated other comprehensive income

(loss) $ (210) $ (249)

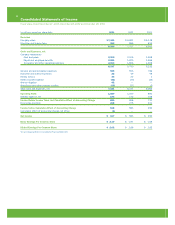

EARNINGS PER COMMON SHARE (“EPS”)

note

6

2003 2002 2001

Net income $ 617 $ 583 $ 492

Basic EPS:

Weighted-average common shares

outstanding 293 296 293

Basic EPS $ 2.10 $ 1.97 $ 1.68

Diluted EPS:

Weighted-average common shares

outstanding 293 296 293

Shares assumed issued on exercise

of dilutive share equivalents 52 56 55

Shares assumed purchased with

proceeds of dilutive

share equivalents (39) (42) (44)

Shares applicable to diluted earnings 306 310 304

Diluted EPS $ 2.02 $ 1.88 $ 1.62

Unexercised employee stock options to purchase approxi-

mately 4 million, 1.4 million and 5.1 million shares of our

Common Stock for the years ended December 27, 2003,

December 28, 2002 and December 29, 2001, respec-

tively, were not included in the computation of diluted EPS

because their exercise prices were greater than the average

market price of our Common Stock during the year.