Pentax 2006 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2006 Pentax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

|

|

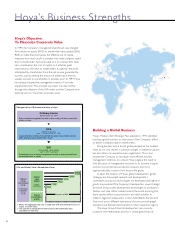

Hoya’s Business Strengths

Reorganization of Business Indicators at Hoya

SVA and Market Value (Shareholder Value)

Ordinary income

Before March 31, 1994

10 years of SVA

ROE

(Return on equity)

April 1, 1994 to March 31, 1997

In 1997, the Company’s management benchmark was changed

from return on equity (ROE) to shareholder value added (SVA).

ROE, an index that emphasizes the effective use of capital,

measures how much profit a company has made using the capital

that its shareholders have entrusted to it. In contrast, SVA takes

into consideration the cost of capital, so it attaches great

importance to the value to shareholders. It subtracts the profit

anticipated by shareholders from the net income generated by

business activity, yielding the amount of added value that has

actually accrued to shareholders. In actuality, prior to 1997 Hoya

had already adopted the management stance of “consider

shareholders first.” This principle was taken one step further

through the utilization of the SVA index, and the Company now

explicitly aims to “maximize corporate value.”

Hoya’s Objective:

To Maximize Corporate Value

Hoya’s Medium-Term Strategic Plan, adopted in 1997, identified

building a global business as a key piece of the Company’s effort

to deliver increased value to shareholders.

Doing business with a broad, global perspective has enabled

Hoya to not only discern in advance changes in market structures

but also reform its overall business organization. This in turn

allowed the Company to introduce more efficient business

management methods. As a result, Hoya outgrew the need to

limit allocation of management resources to its business in Japan,

and can choose the best production locations and most

appropriate sales locations from around the globe.

In Japan, the location of Hoya’s global headquarters, global

strategies are formulated, research and development is

undertaken, production technologies are developed, and high-end

goods are produced. The Company’s headquarters issues strategic

directives and provides development technologies to production

facilities and sales offices located around the world, ensuring that

these quickly reflect local production and sales activities. In

addition, regional headquarters in the United States, Europe and

Asia work across different operational divisions, providing legal

assistance and financial administration to their respective regions.

The Hoya Group Financial Headquarters are currently

located in the Netherlands, and this is where global financial

Building a Global Business

Sales-oriented management focused on how much profit has increased in

relation to sales

Capital efficiency-oriented management focused on how much profit has

been generated using shareholders’ equity

SVA

(Shareholder value added)

April 1, 1997 to present

Shareholder value-oriented management focused on how much profit has

exceeded the cost of capital

(Theoretical

aggregate

market

value)

(MVA)

(Premium)

’

1. MVA is the aggregate each year of single-year SVA discounted by the cost of

capital at current value.

2. The outcome of utilizing SVA will be the same as the shareholder value

calculated from cash flow.