Oracle 2011 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2011 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

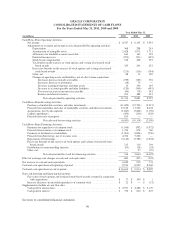

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2011

aforementioned criteria for a separate unit of accounting are not met, the deliverable is combined with the

undelivered element(s) and treated as a single unit of accounting for the purposes of allocation of the

arrangement consideration and revenue recognition. For those units of accounting that include more than one

deliverable but are treated as a single unit of accounting, we generally recognize revenues over the delivery

period. For the purposes of revenue classification of the elements that are accounted for as a single unit of

accounting, we allocate revenue to hardware systems and services based on a rational and consistent

methodology utilizing our best estimate of fair value of such elements.

For our nonsoftware multiple-element arrangements, we allocate revenue to each element based on a selling price

hierarchy at the arrangement inception. The selling price for each element is based upon the following selling

price hierarchy: VSOE if available, third party evidence (TPE) if VSOE is not available, or estimated selling

price (ESP) if neither VSOE nor TPE are available (a description as to how we determine VSOE, TPE and ESP is

provided below). If a tangible hardware systems product includes software, we determine whether the tangible

hardware systems product and the software work together to deliver the product’s essential functionality and, if

so, the entire product is treated as a nonsoftware deliverable. The total arrangement consideration is allocated to

each separate unit of accounting for each of the nonsoftware deliverables using the relative selling prices of each

unit based on the aforementioned selling price hierarchy. We limit the amount of revenue recognized for

delivered elements to an amount that is not contingent upon future delivery of additional products or services or

meeting of any specified performance conditions.

To determine the selling price in multiple-element arrangements, we establish VSOE of selling price using the

price charged for a deliverable when sold separately and for software license updates and product support and

hardware systems support, based on the renewal rates offered to customers. For nonsoftware multiple-element

arrangements, TPE is established by evaluating similar and interchangeable competitor products or services in

standalone arrangements with similarly situated customers. If we are unable to determine the selling price

because VSOE or TPE doesn’t exist, we determine ESP for the purposes of allocating the arrangement by

reviewing historical transactions, including transactions whereby the deliverable was sold on a standalone basis

and considering several other external and internal factors including, but not limited to, pricing practices

including discounting, margin objectives, competition, the geographies in which we offer our products and

services, the type of customer (i.e. distributor, value added reseller, government agency and direct end user,

among others) and the stage of the product lifecycle. The determination of ESP is made through consultation

with and approval by our management, taking into consideration our pricing model and go-to-market strategy. As

our, or our competitors’, pricing and go-to-market strategies evolve, we may modify our pricing practices in the

future, which could result in changes to our determination of VSOE, TPE and ESP. As a result, our future

revenue recognition for multiple-element arrangements could differ materially from our results in the current

period. Selling prices are analyzed on an annual basis or more frequently if we experience significant changes in

our selling prices.

Revenue Recognition Policies Applicable to both Software and Nonsoftware Elements

Revenue Recognition for Multiple-Element Arrangements – Arrangements with Software and Nonsoftware

Elements

We also enter into multiple-element arrangements that may include a combination of our various software related

and nonsoftware related products and services offerings including hardware systems products, hardware systems

support, new software licenses, software license updates and product support, consulting, Cloud Services and

education. In such arrangements, we first allocate the total arrangement consideration based on the relative

selling prices of the software group of elements as a whole and to the nonsoftware elements. We then further

allocate consideration within the software group to the respective elements within that group following the

guidance in ASC 985-605 and our policies as described above. After the arrangement consideration has been

allocated to the elements, we account for each respective element in the arrangement as described above.

94