Oracle 2011 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2011 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

ORACLE CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

May 31, 2011

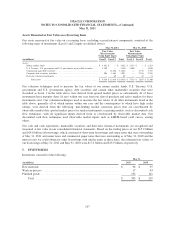

Included in our non-operating income (expense), net for fiscal 2010 was a foreign currency remeasurement loss

of $81 million resulting from the designation of our Venezuelan subsidiary as “highly inflationary” in accordance

with ASC 830, Foreign Currency Matters, and subsequent devaluation of the Venezuelan currency by the

Venezuelan government.

Income Taxes

We account for income taxes in accordance with ASC 740, Income Taxes. Deferred income taxes are recorded

for the expected tax consequences of temporary differences between the tax bases of assets and liabilities for

financial reporting purposes and amounts recognized for income tax purposes. We record a valuation allowance

to reduce our deferred tax assets to the amount of future tax benefit that is more likely than not to be realized.

A two-step approach is applied pursuant to ASC 740 in the recognition and measurement of uncertain tax

positions taken or expected to be taken in a tax return. The first step is to determine if the weight of available

evidence indicates that it is more likely than not that the tax position will be sustained in an audit, including

resolution of any related appeals or litigation processes. The second step is to measure the tax benefit as the

largest amount that is more than 50% likely to be realized upon ultimate settlement. We recognize interest and

penalties related to uncertain tax positions in our provision for income taxes line of our consolidated statements

of operations.

A description of our accounting policies associated with tax related contingencies and valuation allowances

assumed as a part of a business combination is provided under “Business Combinations” above.

Recent Accounting Pronouncements

Presentation of Comprehensive Income: In June 2011, the FASB issued Accounting Standards Update

No. 2011-05, Comprehensive Income (Topic 220)—Presentation of Comprehensive Income (ASU 2011-05), to

require an entity to present the total of comprehensive income, the components of net income, and the

components of other comprehensive income either in a single continuous statement of comprehensive income or

in two separate but consecutive statements. ASU 2011-05 eliminates the option to present the components of

other comprehensive income as part of the statement of equity. ASU 2011-05 is effective for us in our first

quarter of fiscal 2013 and should be applied retrospectively. We are currently evaluating the impact of our

pending adoption of ASU 2011-05 on our consolidated financial statements.

Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements: In May 2011, the

FASB issued Accounting Standards Update No. 2011-04, Amendments to Achieve Common Fair Value

Measurement and Disclosure Requirements in U.S. GAAP and International Financial Reporting Standards (Topic

820)—Fair Value Measurement (ASU 2011-04), to provide a consistent definition of fair value and ensure that the

fair value measurement and disclosure requirements are similar between U.S. GAAP and International Financial

Reporting Standards. ASU 2011-04 changes certain fair value measurement principles and enhances the disclosure

requirements particularly for level 3 fair value measurements (as defined in Note 4 below). ASU 2011-04 is

effective for us in our fourth quarter of fiscal 2012 and should be applied prospectively. We are currently evaluating

the impact of our pending adoption of ASU 2011-04 on our consolidated financial statements.

Disclosure of Supplementary Pro Forma Information for Business Combinations: In December 2010, the

FASB issued Accounting Standards Update No. 2010-29, Disclosure of Supplementary Pro Forma Information

for Business Combinations (Topic 805)—Business Combinations (ASU 2010-29), to improve consistency in how

the pro forma disclosures are calculated. Additionally, ASU 2010-29 enhances the disclosure requirements and

requires description of the nature and amount of any material, nonrecurring pro forma adjustments directly

attributable to a business combination. ASU 2010-29 is effective for us in fiscal 2012 and should be applied

prospectively to business combinations for which the acquisition date is after the effective date. Early adoption is

permitted. We will adopt ASU 2010-29 in fiscal 2012 and do not believe it will have a material impact on our

consolidated financial statements.

102