Office Depot 2012 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2012 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174

|

|

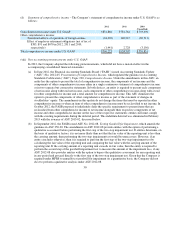

NIF B-4, Statement of Changes in Stockholders’ Equity, establishes the general principles for the presentation and structure of

the statement of changes in stockholders’ equity, such as showing retrospective adjustments due to accounting changes and

correction of errors that affect the beginning balances of stockholders’ equity and presenting comprehensive income (loss) in a

single line item, presenting detail of all items comprising comprehensive income (loss) based on the requirements of NIF B-3.

NIF B-6, Statement of Financial Position, specifies the structure of the statement of financial position as well as the rules of

presentation and disclosure.

NIF B-8, Consolidated or Combined Financial Statements, modifies the definition of control, which is the basis for requiring

that the financial information of that entity is consolidated with the reporting entity. Based on this new definition of control,

certain investments which did not previously require consolidation may now be consolidated while other investments that were

previously consolidated may no longer require consolidation. This NIF establishes that an entity controls another when it has

power to direct the investees relevant activities; it is exposed or entitled to variable returns from such participation in the

investee; and it has the ability to use its power to affect its returns. This standard introduces the concept of protective rights,

defined as the rights that protect the involvement of the investor but do not necessarily give the investor control. This standard

incorporates the principal-agent concept, whereby a decision-maker who has the authority to decide on the relevant activities of

the investee is considered a principal, while an agent merely makes decisions on behalf of the principal and thus does not

exercise control over the investee. The standard also replaces the concept of a special-purpose entity with a structured entity,

which is an entity designed in such a way that voting or other similar rights are not the determining factor for deciding controls

over the structured entity.

NIF C-7, Investments in Associates, Joint ventures and Other Permanent Investments, establishes that investments in joint

ventures should be recognized through the application of the equity method and that the participation of an investor in the

income or loss of investments in associated companies, joint ventures and others permanent investment should be recognized in

results in a single line item representing participation in the results of such investments. It requires additional disclosures aimed

at providing enahanced financial information of the associates and joint ventures and eliminates.

NIF C-21, Joint Control Arrangements, defines a joint arrangement as an arrangement in which two or more parties have joint

control. These types of arrangements can be in the form of 1) joint operations, whereby the parties to the arrangement have

direct rights to the assets and obligations for the liabilities of the arrangement or 2) joint ventures, whereby the parties have

rights to participate only in the residual value of the net assets of the arrangement. This standard establishes that participation in

a joint venture must be recognized as a permanent investment, and accounted for using the equity method.

Improvements to Mexican Financial Reporting Standards 2013—The main improvements that generate accounting changes that

should be recognized retroactively in fiscal years beginning on January 1, 2013 are:

Bulletin C-9, Liabilities, Provisions, Assets and Contingent Liabilities and Commitments and Bulletin C-12, Financial

Instruments with Characteristics of Liabilities,Equity or Both, establish that debt issuance costs must be presented net

against the corresponding liability and applied to results based on the effective interest method.

Bulletin C-15, Accounting for Impairment and Disposal of Long-lived Assets, eliminates the obligation to restate, for

comparative purposes, statements of financial position of prior periods for the effects of assets held for sale.

Bulletin D-5, Leases, establishes that non-refundable payments related to leasehold rights must be deferred during the lease

term and applied to results in proportion to the recognition of income or expense relating to the lessor or lessee,

respectively.

As of the date of these consolidated financial statements, the Company is still in the process of determining the effects of

adoption of these new standards.

22