Nordstrom 2005 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2005 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

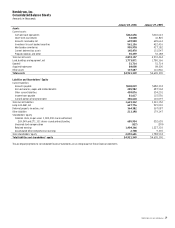

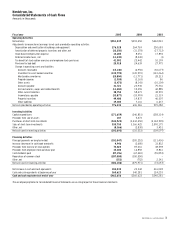

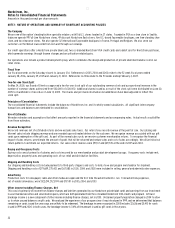

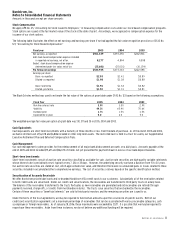

Nordstrom, Inc. and subsidiaries 23

Revenue Recognition

We recognize revenues net of estimated returns and we exclude sales taxes. Our retail stores record revenue at the point of sale. Our catalog

and Internet sales include shipping revenue and are recorded upon estimated delivery to the customer. As part of the normal sales cycle, we

receive customer merchandise returns. To recognize the financial impact of sales returns, we estimate the amount of goods that will be returned

and reduce sales and cost of sales accordingly. We utilize historical return patterns, which have remained consistent year over year, to estimate

our expected returns.

Vendor Allowances

We receive allowances from merchandise vendors for purchase price adjustments, cooperative advertising programs, cosmetic selling expenses and

vendor sponsored contests. Purchase price adjustments are recorded as a reduction of cost of sales after an agreement with the vendor is executed

and the related merchandise has been sold. Allowances for cooperative advertising programs and vendor sponsored contests are recorded in cost

of sales and selling, general and administrative expenses as a reduction to the related cost when incurred. Allowances for cosmetic selling expenses

are recorded in selling, general and administrative expenses as a reduction to the related cost when incurred. Any allowances in excess of actual

costs incurred that are recorded in selling, general and administrative expenses are recorded as a reduction to cost of sales.

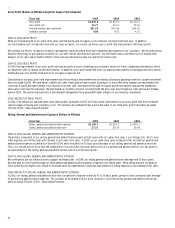

Self Insurance

We retain a portion of the risk for certain losses related to health and welfare, workers’ compensation and general liability claims. Liabilities

associated with these losses include estimates of both losses reported and losses incurred but not yet reported. We estimate our ultimate cost

based on internal analysis of historical data and independent actuarial estimates. We experienced an increase in our California workers’

compensation costs in 2002 and 2003 and declining costs in 2005. Our total workers’ compensation costs over the last three years have

been $12,804, $29,263, and $33,782 in 2005, 2004, and 2003.

Allowance For Doubtful Accounts

Our allowance for doubtful accounts represents our best estimate of the losses inherent in our private label credit card receivable as of the

balance sheet date. We evaluate the collectibility of our accounts receivable based on several factors, including historical trends of aging of

accounts, write-off experience and expectations of future performance. We recognize finance charges on delinquent accounts until the account

is written off. Delinquent accounts are written off when they are determined to be uncollectible, usually after the passage of 151 days without

receiving a full scheduled monthly payment. Accounts are written off sooner in the event of customer bankruptcy or other circumstances

that make further collection unlikely. Our write-off experience and aging trends have improved each of the last three years.

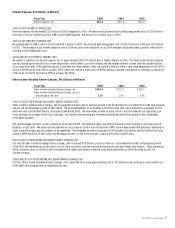

Intangible Asset Impairment Testing

We review our goodwill and acquired tradename annually for impairment in the first quarter or when circumstances indicate the carrying value of

these assets may not be recoverable. The goodwill and acquired tradename associated with our Façonnable business are our largest impairment

risk. In 2005, we engaged an independent valuation specialist to estimate the reporting unit’s fair value.

Leases

We lease the land or the land and building at many of our Full-Line stores, and we lease the building at many of our Rack stores. Additionally, we

lease office facilities, warehouses and equipment. We recognize lease expense on a straight-line basis over the minimum lease term. In 2004,

we corrected our lease accounting policy to recognize lease expense, net of property incentives, from the time that we control the leased property.

We recorded a charge of $7.8 million ($4.7 million net of tax) in the fourth quarter of 2004 to correct this accounting policy. The impact of this

change was immaterial to prior periods. Many of our leases include options that allow us to extend the lease term beyond the initial commitment

period, subject to terms agreed to at lease inception. For leases that contain rent holiday periods and scheduled rent increases, we record the

difference between the rent expense and the rental amount payable under the leases in liabilities. Some leases require additional payments

based on sales and are recorded in rent expense when the contingent rent is probable.

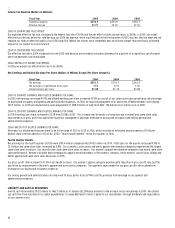

RECENT ACCOUNTING PRONOUNCEMENTS

In November 2004, the FASB issued SFAS No. 151, “Inventory Costs an amendment of ARB No. 43, Chapter 4.” SFAS No. 151 amends ARB No. 43,

Chapter 4, “Inventory Pricing” to clarify that abnormal amounts of idle facility expense, freight, handling costs, and wasted material should be

recognized as current period charges. In addition, this statement requires that fixed overhead production be allocated to the costs of conversion

based on the normal capacity of the production facilities. SFAS No. 151 is effective for inventory costs incurred during fiscal years beginning

after June 15, 2005, and should be applied prospectively. We do not believe the adoption of SFAS No. 151 will have a material impact on our

financial statements.

In December 2004, the FASB issued SFAS No. 123R, “Share-Based Payment.” SFAS No. 123R requires us to measure the cost of employee services

received in exchange for an award of equity instruments based on the grant-date fair value of the award. That cost will be recognized over the

period during which an employee is required to provide services in exchange for the award. We expect to adopt SFAS No. 123R in the first quarter

of 2006 under the modified prospective method. We believe adoption of SFAS No. 123R will reduce our 2006 diluted earnings per share by $0.06.