Macy's 2010 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2010 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

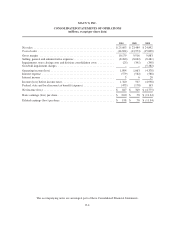

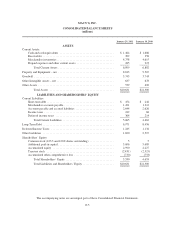

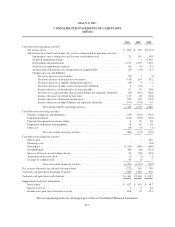

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Company formally documents the relationship between hedging instruments and hedged items, as well as the risk

management objective and strategy for undertaking various hedge transactions. Derivative instruments that the

Company may use as part of its interest rate risk management strategy include interest rate swap and interest rate

cap agreements and Treasury lock agreements. At January 29, 2011, the Company was not a party to any

derivative financial instruments.

The Company records stock-based compensation expense according to the provisions of ASC Topic 718,

“Compensation – Stock Compensation.” ASC Topic 718 requires all share-based payments to employees,

including grants of employee stock options, to be recognized in the financial statements based on their fair

values. Under the provisions of ASC Topic 718, the Company must determine the appropriate fair value model to

be used for valuing share-based payments and the amortization method for compensation cost. See Note 13,

“Stock Based Compensation,” for further information.

In January 2010, the FASB issued Accounting Standards Update No. 2010-06, which provides amendments

and requires new disclosures relating to ASC Topic 820, “Fair Value Measurements and Disclosures,” and also

conforming amendments to guidance relating to ASC Topic 715, “Compensation – Retirement Benefits.” The

Company adopted this guidance on January 31, 2010, except for the disclosure requirement regarding purchases,

sales, issuances and settlements in the rollforward of activity in Level 3 fair value measurements, which the

Company adopted on January 30, 2011. This guidance is limited to the form and content of disclosures, and the

portion thereof that has been adopted did not have a material impact on the Company’s consolidated financial

position, results of operations or cash flows. The Company does not anticipate that the full adoption of this

guidance will have a material impact on the Company’s consolidated financial position, results of operations or

cash flows.

In July 2010, the FASB issued Accounting Standard Update No. 2010-20, which amends various sections of

ASC Topic 310, “Receivables,” relating to a company’s allowance for credit losses and the credit quality of its

financing receivables. The amendment requires companies to provide disaggregated levels of disclosure by

portfolio segment and class of financing receivable to enable users of the financial statements to understand the

nature of credit risk, how the risk is analyzed in determining the related allowance for credit losses and changes

to the allowance during the reporting period. The Company adopted this guidance as of January 29, 2011, except

as it relates to disclosures regarding activities during a reporting period, which is effective for interim and annual

periods beginning on or after December 31, 2010. This guidance is limited to the form and content of disclosures.

The initial adoption did not have, and the full adoption is not expected to have, an impact on the Company’s

consolidated financial position, results of operations or cash flows.

In December 2010, the FASB issued Accounting Standard Update No. 2010-28, which amends ASC Topic

350, “Goodwill and Other,” relating to the goodwill impairment test of a reporting unit with zero or negative

carrying amounts. This guidance is effective for interim and annual periods beginning after December 15, 2010.

The Company does not anticipate that the adoption of this guidance will have a material impact on the

Company’s consolidated financial position, results of operations or cash flows.

F-13