Frontier Airlines 2004 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2004 Frontier Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

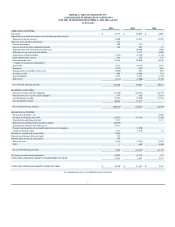

Liquidity and Capital Resources

Historically, we have used internally generated funds and third

-

party financing to meet our working capital and capital expenditure requirements. In June 2004, we completed our initial

public common stock offering, which provided approximately $58.2 million, net of offering expenses and before the repayment of debt. In addition, we completed a follow

-

on offering in

February 2005, which provided approximately $80.8 million, net of offering expenses. As a result of our code

-

share agreements with Delta and United, which require us to significantly increase

our fleet of regional jets, we will significantly increase our cash requirements for debt service and lease payments.

As of December 31, 2004, we had $46.2 million in cash and $16.7 million available under our revolving credit facility. At December 31, 2004, we had a working capital deficit of

$28.1 million primarily due to $47.4 million due for principal payments under long term debt obligations incurred pursuant to the acquisition of our Embraer jets, all coming due within 12 months.

Additionally, we have $47.4 million in aircraft deposits that are classified as non

-

current assets. We have had a working capital deficiency since 1999; however, we have been able to meet all of

our current obligations due to the net cash generated from operating activities and the deficiency has not impaired our ability to implement our growth plan.

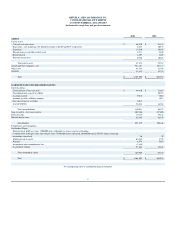

Chautauqua has a credit facility with Bank of America Business Capital, which currently provides it with a $25.0 million revolving credit facility, less the aggregate principal balance of the

term loan and the equipment loans. The equipment loans cannot exceed $5 million. At December 31, 2004, Chautauqua had $3.2 million outstanding under a term loan. At December 31, 2004,

Chautauqua had $4.8 million of outstanding letters of credit. The proceeds of the term loan were obtained in December 2004 for a GE engine purchased in October 2004. The loan is payable in

monthly principal installments of $53,543 through March 2006 with the remaining balance due March 31, 2006. The $3.2 million is classified as a current liability on the balance sheet. The

revolving credit facility expires March 31, 2006.

The revolving credit facility allows Chautauqua to borrow up to 70% of the lower of net book value or appraised orderly liquidation value of spare rotable parts and up to 40% of the

lower of net book value or appraised orderly liquidation value of spare non

-

rotable parts for our regional jet fleet. The revolving credit facility is collateralized by all of Chautauqua's assets,

excluding the owned aircraft and engines. Borrowings under the credit facility bear interest at a rate equal to, at Chautauqua's option, LIBOR plus spreads ranging from 2.0% to 2.75% or the

bank's base rate (which is generally equivalent to the prime rate) plus spreads ranging from 0.25% to 0.75%. Chautauqua pays an annual commitment fee on the unused portion of the revolving

credit facility in an amount equal to 0.375% of the unused amounts. The credit facility limits Chautauqua's ability to incur indebtedness or create or incur liens on our assets. In addition, the credit

facility requires Chautauqua to maintain a specified fixed charge coverage ratio and a debt to earnings leverage ratio. Chautauqua received a waiver from the lender under the revolving credit

facility for non

-

compliance with the debt to earnings leverage ratio for the fourth quarter of 2004. The credit facility can be terminated if WexAir LLC and its affiliates cease to own at least 51%

of the voting control of Republic Airways.

As of December 31, 2004, we currently lease nine spare regional jet engines from General Electric Capital Aviation Services and five spare regional jet engines from RRPF Engine

Leasing (US) LLC.

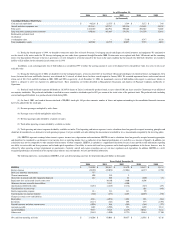

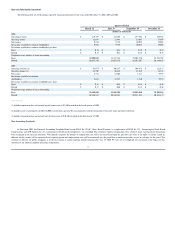

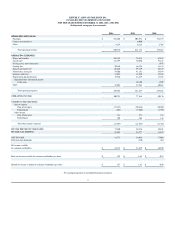

Net cash from operating activities was $50.9 million, $93.1 million and $116.2 million for the years ended December 31, 2002, 2003 and 2004, respectively. The increase from

operating activities is primarily due to the continued growth of our business. For 2004, net cash from operating activities is primarily net income of $44.8 million, depreciation and amortization of

$33.9 million, the change in deferred income taxes of $28.1 million and the increase in accounts payable and other current liabilities of $11.0 million. For 2003, net cash from operating activities

consisted primarily of net income of $34.0 million, depreciation and amortization of $23.4 million, the change in deferred income taxes of $22.0 million, a non

-

cash charge for impairment loss and

accrued aircraft return costs of $10.2 million and an increase in current accrued liabilities of $9.3 million partially offset by increases in receivables and other assets of $(6.9) million. For 2002,

net cash from operating activities represents net income of $17.0 million, a non

-

cash charge for impairment loss and accrued aircraft return costs of $3.8 million, depreciation and amortization of

$11.8 million and change in deferred income taxes of $16.1 million.

Net cash from investing activities was $(33.0) million, $(30.4) million and $(100.8) million for the years ended December 31, 2002, 2003 and 2004, respectively. In 2004, we purchased

24 Embraer regional jets and our aircraft deposits totaled $38.8 million. In 2003, we purchased 20 Embraer regional jets, $4.3 million of spare parts, $2.4 million in aircraft leasehold

improvements and $1.1 million of maintenance equipment. In 2002, we purchased 11 Embraer regional jets.

Net cash from financing activities was $(17.8) million, $(44.5) million and $9.3 million for the years ended December 31, 2002, 2003 and 2004, respectively. For 2004, we made

scheduled debt payments and payments to the debt sinking fund of $26.9 million. Our net cash from financing activities included $58.2 million net cash received from stock offering proceeds in

June 2004. We used $20.4 million to repay WexAir LLC for indebtedness we originally incurred in May 1998 to finance a portion of our purchase of Chautauqua. In 2003, we made

$39.1 million of scheduled debt payments primarily related to the Embraer regional jets, paid $5.4 million to redeem preferred stock to an affiliate of WexAir LLC and paid $2.0 million in fees to

obtain financing for the Embraer regional jets. In 2002, we repaid $7.0 million of the revolving credit facility, paid $3.9 million in fees relating to obtaining permanent financing for the Embraer

regional jets and made $5.4 million of scheduled debt payments related to the Embraer regional jets. These decreases were partially offset by $2.1 million of proceeds from the refinancing of the

Embraer regional jets in January and June of 2002.

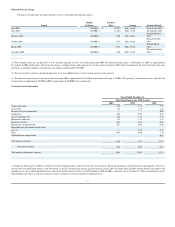

Aircraft Leases and Other Off

-

Balance Sheet Arrangements

We have significant obligations for aircraft and engines that are classified as operating leases and, therefore, are not reflected as liabilities on our balance sheet. These leases expire

between 2009 and 2020. As of December 31, 2004, our total mandatory payments under operating leases aggregated approximately $793.0 million and total minimum annual aircraft rental

payments for the next 12 months under all noncancellable operating leases is approximately $69.7 million, excluding the Saab aircraft.

Other non

-

cancelable operating leases consist of engines, terminal space, operating facilities, office space and office equipment. The leases expire through 2017. As of December 31,

2004, our total mandatory payments under other non

-

cancelable operating leases aggregated approximately $51.4 million. Total minimum annual other rental payments for the next 12 months are

approximately $5.0 million.

32