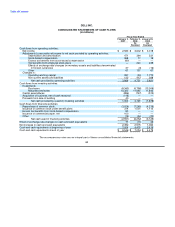

Dell 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 Dell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

Table of Contents

includes obtaining an understanding of internal control over financial reporting, evaluating management's assessment,

testing and evaluating the design and operating effectiveness of internal control, and performing such other procedures as

we consider necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinions.

A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the

reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally

accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures

that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and

dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to

permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and

expenditures of the company are being made only in accordance with authorizations of management and directors of the

company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or

disposition of the company's assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also,

projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate

because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

A material weakness is a control deficiency, or combination of control deficiencies, that results in more than a remote

likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected. The

following material weaknesses as of February 2, 2007 have been identified and included in management's assessment:

Control environment — The Company did not maintain an effective control environment. The control environment, which is

the responsibility of senior management, sets the tone of the organization, influences the control consciousness of its people,

and is the foundation for all other components of internal control over financial reporting. Specifically:

-

The Company did not maintain a tone and control consciousness that consistently emphasized strict adherence to

accounting principles generally accepted in the United States of America. This control deficiency, in some instances,

included inappropriate accounting decisions and entries that appear to have been largely motivated to achieve desired

accounting results and management override of controls. In a number of instances, information critical to an effective

review of transactions and accounting entries was not disclosed to internal and external auditors.

-

The Company did not maintain a sufficient complement of personnel with an appropriate level of accounting knowledge,

experience, and training in the application of accounting principles generally accepted in the United States of America

commensurate with the Company's financial reporting requirements and business environment.

The control environment material weaknesses described above contributed to the material weaknesses related to the

Company's period-end financial reporting process described below.

Period-end financial reporting process — The Company did not maintain effective controls over the period-end financial

reporting process, including controls with respect to the review, supervision, and monitoring of accounting operations.

Specifically:

-

Journal entries, both recurring and nonrecurring, were not always accompanied by sufficient supporting documentation

and were not adequately reviewed and approved for validity, completeness and accuracy;

-

Account reconciliations over balance sheet accounts were not always properly and timely performed, and the

reconciliations and their supporting documentation were not consistently reviewed for completeness, accuracy and timely

resolution of reconciling items; and

59