Classmates.com 2007 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2007 Classmates.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

|

|

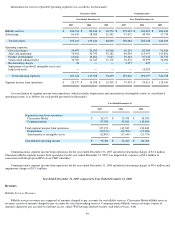

which is recognized upon a disqualified disposition; and (6) the benefit of federal tax exempt interest income.

Cumulative Effect of Accounting Change, Net of Tax

In the year ended December 31, 2006, we recorded a $1.1 million pre-tax benefit ($1.0 million, net of tax) as the cumulative effect of

accounting change upon the adoption of SFAS No. 123R to recognize the effect of estimating the number of equity awards granted prior to

January 1, 2006 that are not ultimately expected to vest.

Year Ended December 31, 2006 compared to Year Ended December 31, 2005

Comparability

On January 1, 2006, we adopted Statement of Financial Accounting Standards, or SFAS, No. 123R (revised 2004), Share-Based Payment ,

which requires the measurement and recognition of compensation expense for all share-based payment awards made to employees and directors

including employee stock options, stock awards and employee stock purchases related to our employee stock purchase plan based on the grant-

date fair values of the awards. SFAS No. 123R supersedes our previous accounting under Accounting Principles Board, or APB, Opinion No. 25,

Accounting for Stock Issued to Employees

. In March 2005, the SEC issued Staff Accounting Bulletin, or SAB, No. 107 relating to SFAS

No. 123R. We have applied the provisions of SAB No. 107 in our adoption of SFAS No. 123R.

We adopted SFAS No. 123R using the modified prospective transition method, and the Company's consolidated financial statements at and

for the years ended December 31, 2007 and 2006 reflect the impact of SFAS No. 123R. In accordance with the modified prospective transition

method, our consolidated financial statements for prior periods have not been restated to reflect, and do not include, the impact of SFAS

No. 123R. Stock

-

based compensation recognized under SFAS No. 123R for the years ended December 31, 2007 and 2006 was $19.5 million and

$19.2 million, respectively, which was primarily related to restricted stock, stock options and the discount on purchases related to our employee

stock purchase plan. Stock-based compensation, recorded in accordance with APB Opinion No. 25, for the year ended December 31, 2005 was

$10.0 million, which was primarily related to restricted stock.

SFAS No. 123R requires companies to estimate the fair value of share-based payment awards on the grant date using an option-pricing

model. Under SFAS No. 123, we used the Black-Scholes option-pricing model for valuation of share-based awards for our pro forma

information. Upon adoption of SFAS No. 123R, we elected to continue to use the Black-Scholes option-pricing model for valuing share-based

payment awards. The value of the portion of the award that is ultimately expected to vest is recognized as an expense over the requisite service

periods in our consolidated statements of operations. Prior to the adoption of SFAS No. 123R, we accounted for share-based payment awards to

employees and directors using the intrinsic value method in accordance with APB Opinion No. 25 as allowed under SFAS No. 123, Accounting

for Stock

-Based Compensation . Under the intrinsic value method, no stock-based compensation related to stock options had been recognized in

our consolidated statements of operations, other than as related to acquisitions, because the exercise price of our stock options granted to

employees and directors equaled the fair market value of the underlying stock at the grant date.

SFAS No. 123R requires forfeitures to be estimated at the time of grant in order to calculate the amount of share-based payment awards

ultimately expected to vest. The forfeiture rate is based on historical rates. Stock-based compensation recognized in our consolidated statement

of operations for the year ended December 31, 2006 includes (i) compensation expense for share-based payment awards granted prior to or on,

but not yet vested at, December 31, 2005 based on the grant-date fair value estimated in accordance with the pro forma provisions of SFAS

No. 123 and (ii) compensation expense

55