CarMax 2005 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2005 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

|

|

CARMAX 2005

37

Proceeds from Collections. Proceeds from collections

reinvested in revolving period securitizations represent

principal amounts collected on receivables securitized through

the warehouse facility that are used to fund new originations.

Servicing Fees. Servicing fees received represent cash fees

paid to the company to service the securitized receivables.

Other Cash Flows Received from the Retained Interest.

Other cash flows received from the retained interest represent

cash received by the company from securitized receivables other

than servicing fees. It includes cash collected on interest-only

strip receivables and amounts released to the company from

restricted cash accounts.

Financial Covenants and Performance Triggers

Certain securitization agreements include various financial

covenants and performance triggers. For such agreements, the

company must meet financial covenants relating to minimum

tangible net worth, maximum total liabilities to tangible net

worth ratio, minimum tangible net worth to managed assets

ratio, minimum current ratio, minimum cash balance or

borrowing capacity, and minimum fixed charge coverage ratio.

Certain securitized receivables must meet performance tests

relating to portfolio yield, default rates, and delinquency rates. If

these financial covenants and/or performance tests are not met,

in addition to other consequences, the company may be unable

to continue to securitize receivables through the warehouse

facility or it may be terminated as servicer under the

securitizations. At February 28, 2005, the company was in

compliance with these financial covenants, and the securitized

receivables were in compliance with these performance triggers.

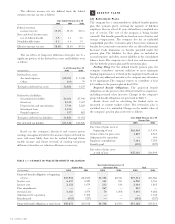

FINANCIAL DERIVATIVES

The company enters into amortizing fixed-pay interest rate swaps

relating to its automobile loan receivable securitizations. Swaps

are used to better match funding costs to the fixed-rate

receivables being securitized by converting variable-rate

financing costs in the warehouse facility to fixed-rate obligations.

The company entered into one 18-month and twenty-six

40-month amortizing interest rate swaps with initial notional

amounts totaling approximately $1.36 billion in fiscal 2005,

twenty-two 40-month amortizing interest rate swaps with initial

notional amounts totaling approximately $1.21 billion in fiscal

2004, and one 20-month and twelve 40-month amortizing

interest rate swaps with initial notional amounts totaling

approximately $1.05 billion in fiscal 2003. The amortized

notional amount of all outstanding swaps related to the

automobile loan receivable securitizations was approximately

$662.1 million at February 28, 2005, and $551.8 million at

February 29, 2004. The fair value of swaps included in prepaid

expenses and other current assets totaled a net asset of $5.4

million at February 28, 2005, and the fair value of swaps included

in accounts payable totaled a net liability of $2.0 million at

February 29, 2004.

The market and credit risks associated with interest rate

swaps are similar to those relating to other types of financial

instruments. Market risk is the exposure created by potential

fluctuations in interest rates.The company does not anticipate

significant market risk from swaps as they are used on a monthly

basis to match funding costs to the use of the funding. Credit

risk is the exposure to nonperformance of another party to an

agreement.The company mitigates credit risk by dealing with

highly rated bank counterparties.

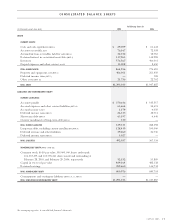

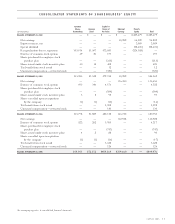

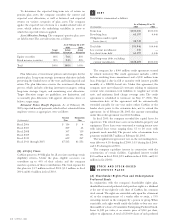

PROPERTY AND EQUIPMENT

Property and equipment, at cost, is summarized as follows:

As of February 28 or 29

(In thousands) 2005 2004

Buildings (25 to 40 years) $ 49,047 $ 30,985

Land 37,650 25,716

Land held for sale 2,664 3,163

Land held for development 6,084 3,580

Construction in progress 198,682 116,639

Furniture, fixtures, and

equipment (5 to 15 years) 125,734 103,787

Leasehold improvements

(8 to 15 years) 45,346 37,533

Capital leases (15 to 20 years) 29,258 —

494,465 321,403

Less accumulated depreciation

and amortization 88,164 69,944

Property and equipment, net $406,301 $251,459

Land held for development represents land owned for future

sites that are scheduled to open more than one year beyond the

fiscal year reported. Leased property meeting certain criteria is

capitalized and the present value of the related lease payments is

recorded as long-term debt. Amortization of capital lease assets

is computed on a straight-line basis over the shorter of the

useful life or the term of the lease and is included in

depreciation expense.

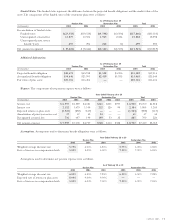

INCOME TAXES

The components of the provision for income taxes on net

earnings were as follows:

Years Ended February 28 or 29

(In thousands) 2005 2004 2003

Current:

Federal $62,662 $65,212 $47,600

State 10,117 8,986 5,415

Total 72,779 74,198 53,015

Deferred:

Federal (1,068) (1,180) 8,614

State (116) (118) 266

Total (1,184) (1,298) 8,880

Provision for income taxes $71,595 $72,900 $61,895

5

6

7