CarMax 2005 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2005 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

26

CARMAX 2005

We maintain a $300 million credit facility secured by vehicle

inventory. As of February 28, 2005, the amount outstanding

under this credit facility was $165.2 million, with the remainder

fully available to the company. See Note 9 to the company’s

consolidated financial statements for discussion of expiration,

renewals, and covenants associated with this facility.

We expect that proceeds from securitization transactions;

sale-leaseback transactions; current and, if needed, additional

credit facilities; and cash generated by operations will be

sufficient to fund capital expenditures and working capital for

the foreseeable future.

Off-Balance Sheet Arrangements

CAF provides prime auto financing for our used and new car

sales.We use a securitization program to fund substantially all of

the automobile loan receivables originated by CAF. We sell the

automobile loan receivables to a wholly owned, bankruptcy-

remote, special purpose entity that transfers an undivided

interest in the receivables to a group of third-party investors.

This program is referred to as the warehouse facility.

We periodically use public securitizations to refinance the

receivables previously securitized through the warehouse

facility. In a public securitization, a pool of automobile loan

receivables is sold to a bankruptcy-remote, special purpose

entity that in turn transfers the receivables to a special purpose

securitization trust.

Additional information regarding the nature, business

purposes, and importance of our off-balance sheet arrangement

to our liquidity and capital resources can be found in the

CarMax Auto Finance Income, Financial Condition, and

Market Risk sections of this MD&A, as well as in Notes 3 and 4

to the company’s consolidated financial statements.

MARKET RISK

Automobile Installment Loan Receivables

At February 28, 2005, and February 29, 2004, all loans in the

portfolio of automobile loan receivables were fixed-rate

installment loans. Financing for these automobile loan

receivables is achieved through asset securitization programs

that, in turn, issue both fixed- and floating-rate securities.

Interest rate exposure relating to floating-rate securitizations is

managed through the use of interest rate swaps. Receivables

held for investment or sale are financed with working capital.

Generally, changes in interest rates associated with underlying

swaps will not have a material impact on earnings. However,

changes in interest rates associated with underlying swaps may

have a material impact on cash and cash flows.

Credit risk is the exposure to nonperformance of another

party to an agreement. Credit risk is mitigated by dealing with

highly rated bank counterparties. The market and credit risks

associated with financial derivatives are similar to those relating

to other types of financial instruments. Refer to Note 5 to the

company’s consolidated financial statements for a description of

these items.

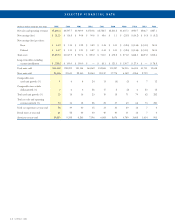

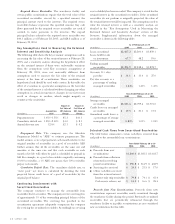

The total principal amount of managed receivables

securitized or held for investment or sale was as follows:

As of February 28 or 29

(In millions) 2005 2004

Fixed-rate securitizations $1,764.7 $1,647.9

Floating-rate securitizations

synthetically altered to fixed 662.1 551.8

Floating-rate securitizations 0.4 0.7

Held for investment(1) 45.5 29.4

Held for sale(2) 22.2 18.8

Total $2,494.9 $2,248.6

(1) The majority is held by a bankruptcy-remote special purpose entity.

(2) Held by a bankruptcy-remote special purpose entity.

CONTRACTUAL OBLIGATIONS

As of February 28, 2005

Less than 1 to 3 3 to 5 More than 5

(In millions) Total 1 Year Years Years Years

Revolving loan $ 65.2 $ 65.2 $ — $ — $ —

Term loan 100.0 — 100.0 — —

Capital leases(1) 64.6 3.2 6.7 6.9 47.9

Operating leases(1) 890.3 61.3 120.8 122.0 586.1

Purchase obligations(2) 71.4 41.2 23.2 7.0 —

Total $1,191.5 $170.9 $250.7 $135.9 $634.0

(1) See Note 12 to the company’s consolidated financial statements.

(2) Purchase obligations include certain enforceable and legally binding obligations related to the purchase of real property, third-party outsourcing services, construction services

related to our new corporate offices, and certain automotive reconditioning products.