CarMax 2005 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2005 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

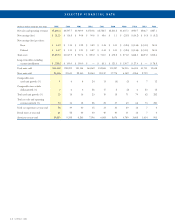

MANAGEMENT’S DISCUSSION AND ANALYSIS

CARMAX 2005

17

The following Management’s Discussion and Analysis of

Financial Condition and Results of Operations (“MD&A”) is

intended to help the reader understand CarMax, Inc. MD&A is

presented in nine sections: Business Overview; Critical

Accounting Policies; Results of Operations; Operations

Outlook; Recent Accounting Pronouncements; Financial

Condition; Contractual Obligations; Market Risk; and

Cautionary Information About Forward-Looking Statements.

MD&A is provided as a supplement to, and should be read in

conjunction with, our consolidated financial statements and the

accompanying notes contained elsewhere in this annual report.

In MD&A,“we,”“our,” “us,”“CarMax,” and “the company”

refer to CarMax, Inc. and its wholly owned subsidiaries, unless

the context requires otherwise. Amounts and percents in tables

may not total due to rounding.

BUSINESS OVERVIEW

General

CarMax is the nation’s largest retailer of used vehicles. The

company was formerly a subsidiary of Circuit City Stores, Inc.

(“Circuit City”). On October 1, 2002, the CarMax business was

separated from Circuit City through a tax-free transaction and

became an independent, separately traded public company. We

pioneered the used car superstore concept, opening our first

store in 1993. Over the next six years, we opened an additional

32 used car superstores before suspending new store

development to focus on improving sales and profits. After a

period of concept refinement and execution improvement, we

resumed used car superstore growth in fiscal 2002, adding two

stores late in the fiscal year, five stores in fiscal 2003, and nine

stores in both fiscal 2004 and fiscal 2005. At the end of fiscal

2005, we had 58 used car superstores in 27 markets, including 8

large markets and 19 mid-sized markets.

We believe the CarMax consumer offer is unique in the

auto retailing marketplace. Our offer gives consumers a way to

shop for cars in the same manner that they shop for items at

other “big box” retailers. Our consumer offer is structured

around four core equities, including low, no-haggle prices; a

broad selection; high quality; and customer-friendly service. We

generate revenues, income, and cash flows primarily by retailing

used vehicles and associated items including vehicle financing,

extended service plans, and vehicle repair service. A majority of

the used vehicles we retail are purchased directly from

consumers. Vehicles purchased through our appraisal process

that do not meet our retail standards are sold at on-site

wholesale auctions.

Sales of new vehicles represented a decreasing percentage of

our total revenues over the last four years as we divested new car

franchises and added used car superstores. We expect to keep

our seven remaining franchises in order to maintain long-term

strategic relationships with automotive manufacturers.

CarMax provides prime-rated financing to qualified

customers through CarMax Auto Finance (“CAF”) and Bank

of America. Nonprime financing is provided through three

third-party lenders, and subprime financing is provided

through a third-party lender under a program rolled out to our

entire store base in August 2004. We periodically test

additional third-party lenders. CarMax has no recourse liability

for loans provided by third-party lenders. Having our own

finance operation allows us to limit the risk of reliance on

third-party finance sources, while also allowing us to capture

additional profit and cash flows. The majority of CAF’s profit

contribution is generated by the spread between the interest

rates charged to customers and our cost of funds. We collect

fixed, prenegotiated fees from the third parties that finance

prime- and nonprime-rated customers. As is customary in the

subprime finance industry, the subprime lender purchases loans

at a discount.

We sell extended service plans on behalf of unrelated third

parties who are the primary obligors. We have no contractual

liability to the customer under these third-party service plans.

Extended service plan revenue represents commissions from the

unrelated third parties.

We are still at an early stage in the national rollout of our retail

concept. We believe the primary driver for future earnings growth

will be vehicle unit sales growth from comparable store sales

increases and from geographic expansion. We target a roughly

similar fixed dollar amount of gross profit per used unit, regardless

of retail price. Used unit sales growth is our primary focus. In

fiscal 2006, we plan to focus our store growth primarily on adding

standard superstores in new mid-sized markets, which we define as

those with television viewing audiences between 1 million and

2.5 million people, and satellite fill-in superstores in established

markets. We also are broadening our store base in the Los Angeles

market, with one additional superstore opened in fiscal 2005 and

two additional superstores opened early in fiscal 2006, which gives

us a total of five stores in the Los Angeles market. We plan to open

used car superstores at a rate of approximately 15% to 20% of our

used car superstore base each year. For the foreseeable future, we

expect used unit comparable store sales increases to average in the

range of 4% to 8%, reflecting the multi-year ramp in sales of newly

opened stores as they mature and continued market share gains at

stores that have reached base maturity sales levels.

The principal challenges we face in expanding our store

base include:

3Our ability to procure suitable real estate at reasonable costs.

3Our ability to build our management bench strength to

support the store growth.

We staff each newly opened store with an experienced

management team, including a location general manager,

operations manager, purchasing manager, and business office

manager, as well as a number of experienced sales managers and

buyers. We must therefore be continually recruiting, training, and

developing managers and associates to fill the pipeline necessary

to support future store openings. If at any time we believed that

the rate of store growth was causing our performance to falter,

we would consider slowing the growth rate.