CarMax 2005 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2005 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

|

|

CARMAX 2005

35

SECURITIZATIONS

The company uses a securitization program to fund

substantially all of the automobile loan receivables originated by

CAF. The company sells the automobile loan receivables to a

wholly owned, bankruptcy-remote, special purpose entity that

transfers an undivided interest in the receivables to a group of

third-party investors. The special purpose entity and investors

have no recourse to the company’s assets. The company’s risk is

limited to the retained interest on the company’s consolidated

balance sheets. The investors issue commercial paper supported

by the transferred receivables, and the proceeds from the sale of

the commercial paper are used to pay for the securitized

receivables. This program is referred to as the warehouse facility.

The company periodically uses public securitizations to

refinance the receivables previously securitized through the

warehouse facility. In a public securitization, a pool of

automobile loan receivables is sold to a bankruptcy-remote,

special purpose entity that in turn transfers the receivables to a

special purpose securitization trust. The securitization trust

issues asset-backed securities, secured or otherwise supported by

the transferred receivables, and the proceeds from the sale of the

securities are used to pay for the securitized receivables. The

earnings impact of refinancing receivables in a public

securitization has not been material to the operations of the

company. However, because securitization structures could

change from time to time, this may not be representative of the

potential impact of future securitizations.

The transfers of receivables are accounted for as sales in

accordance with SFAS No. 140. When the receivables are

securitized, the company recognizes a gain or loss on the sale of

the receivables as described in Note 3.

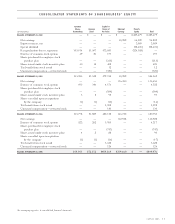

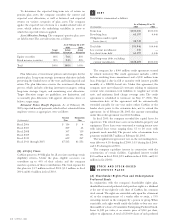

Years Ended February 28 or 29

(In millions) 2005 2004 2003

Net loans originated $1,490.3 $1,407.6 $1,189.0

Loans sold $1,534.8 $1,390.2 $1,185.9

Gains on sales of loans $ 58.3 $ 65.1 $ 68.2

Gains on sales of loans as a

percentage of loans sold 3.8% 4.7% 5.8%

Retained Interest

The company retains an interest in the automobile loan

receivables that it securitizes. The retained interest, presented as a

current asset on the company’s consolidated balance sheets,

serves as a credit enhancement for the benefit of the investors in

the securitized receivables. The retained interest includes the

present value of the expected residual cash flows generated by

the securitized receivables, or “interest-only strip receivables,”

the restricted cash on deposit in various reserve accounts, and an

undivided ownership interest in the receivables securitized

through the warehouse facility and certain public securitizations,

or “required excess receivables,” as described below. On a

combined basis, the cash reserves and required excess receivables

are generally 2% to 4% of managed receivables. The special

purpose entities and the investors have no recourse to the

company’s assets. The company’s risk is limited to the retained

interest on the company’s consolidated balance sheets. The fair

value of the retained interest may fluctuate depending on the

performance of the securitized receivables.

The fair value of the retained interest was $148.0 million as

of February 28, 2005, and $146.0 million as of February 29,

2004. The retained interest had a weighted average life of 1.5

years as of February 28, 2005, and as of February 29, 2004. As

defined in SFAS No. 140, the weighted average life in periods

(for example, months or years) of prepayable assets is calculated

by multiplying the principal collections expected in each future

period by the number of periods until that future period,

summing those products, and dividing the sum by the initial

principal balance.The following is a detailed explanation of the

components of the retained interest.

Interest-Only Strip Receivables. Interest-only strip receivables

represent the present value of residual cash flows the company

expects to receive over the life of the securitized receivables. The

value of these receivables is determined by estimating the future

cash flows using management’s assumptions of key factors, such as

finance charge income, default rates, prepayment rates, and

discount rates appropriate for the type of asset and risk. The value

of interest-only strip receivables may be affected by external

factors, such as changes in the behavior patterns of customers,

changes in the strength of the economy, and developments in the

interest rate markets; therefore, actual performance may differ

from these assumptions. Management evaluates the performance

of the receivables relative to these assumptions on a regular basis.

Any financial impact resulting from a change in performance is

recognized in earnings in the period in which it occurs.

Restricted Cash. Restricted cash represents amounts on

deposit in various reserve accounts established for the benefit of

the securitization investors. In the event that the cash generated

by the securitized receivables in a given period was insufficient

to pay the interest, principal, and other required payments, the

balances on deposit in the reserve accounts would be used to pay

those amounts. In general, each of the company’s securitizations

requires that an amount equal to a specified percentage of the

initial receivables balance be deposited in a reserve account on

the closing date and that any excess cash generated by the

receivables be used to fund the reserve account to the extent

necessary to maintain the required amount. If the amount on

deposit in the reserve account exceeds the required amount, an

amount equal to that excess is released through the special

purpose entity to the company. In the public securitizations, the

amount required to be on deposit in the reserve account must

equal or exceed a specified floor amount. The reserve account

remains at the floor amount until the investors are paid in full, at

which time the remaining reserve account balance is released

through the special purpose entity to the company. The amount

required to be maintained in the public securitization reserve

accounts may increase depending upon the performance of the

securitized receivables. The amount on deposit in restricted cash

accounts was $33.5 million as of February 28, 2005, and $34.8

million as of February 29, 2004.

4