CVS 2006 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2006 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

2006 Annual Report 25

Inventory

Our inventory is stated at the lower of cost or market on a first-in, first-out

basis using the retail method of accounting to determine cost of sales

and inventory in our stores, and the cost method of accounting to

determine inventory in our distribution centers. Under the retail method,

inventory is stated at cost, which is determined by applying a cost-to-

retail ratio to the ending retail value of our inventory. Since the retail

value of our inventory is adjusted on a regular basis to reflect current

market conditions, our carrying value should approximate the lower of

cost or market. In addition, we reduce the value of our ending inventory

for estimated inventory losses that have occurred during the interim

period between physical inventory counts. Physical inventory counts are

taken on a regular basis in each location (other than the two recently

constructed distribution centers, which perform a continuous cycle

count process to validate the inventory balance on hand) to ensure that

the amounts reflected in the consolidated financial statements are

properly stated.

The accounting for inventory contains uncertainty since we must use

judgment to estimate the inventory losses that have occurred during the

interim period between physical inventory counts. When estimating

these losses, we consider a number of factors, which include but are not

limited to, historical physical inventory results on a location-by-location

basis and current inventory loss trends.

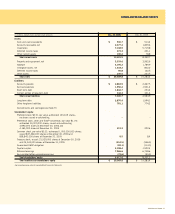

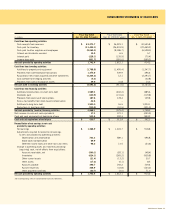

Our total reserve for estimated inventory losses covered by this critical

accounting policy was $125.1 million as of December 30, 2006. Although

we believe we have sufficient current and historical information available

to us to record reasonable estimates for estimated inventory losses, it is

possible that actual results could differ. In order to help you assess the

aggregate risk, if any, associated with the uncertainties discussed above,

a ten percent (10%) pre-tax change in our estimated inventory losses,

which we believe is a reasonably likely change, would increase or decrease

our total reserve for estimated inventory losses by about $12.5 million

during 2006.

We have not made any material changes in the accounting methodology

used to establish our inventory loss reserves during the past three years.

Although we believe that the estimates discussed above are reasonable

and the related calculations conform to generally accepted accounting

principles, actual results could differ from our estimates, and such

differences could be material.

Our total closed store lease liability covered by this critical accounting

policy was $489.4 million as of December 30, 2006. This amount is

net of $246.6 million of estimated sublease income that is subject to

the uncertainties discussed above. Although we believe we have sufficient

current and historical information available to us to record reasonable

estimates for sublease income, it is possible that actual results could

differ. In order to help you assess the risk, if any, associated with the

uncertainties discussed above, a ten percent (10%) pre-tax change in

our estimated sublease income, which we believe is a reasonably likely

change, would increase or decrease our total closed store lease liability

by about $24.7 million during 2006.

We have not made any material changes in the reserve methodology

used to record closed store lease reserves during the past three years.

Self-Insurance Liabilities

We are self-insured for certain losses related to general liability, workers’

compensation and auto liability although we maintain stop loss coverage

with third party insurers to limit our total liability exposure. We are also

self-insured for certain losses related to health and medical liabilities.

The estimate of our self-insurance liability contains uncertainty since we

must use judgment to estimate the ultimate cost that will be incurred to

settle reported claims and unreported claims for incidents incurred but not

reported as of the balance sheet date. When estimating our self-insurance

liability we consider a number of factors, which include, but are not limited

to, historical claim experience, demographic factors, severity factors and

valuations provided by independent third party actuaries.

On a quarterly basis, we review our assumptions with our independent

third party actuaries to determine that our self-insurance liability is adequate

as it relates to our general liability, workers’ compensation and auto liability.

Similar reviews are conducted semi-annually to determine that our self-

insurance liability is adequate for our health and medical liability.

Our total self-insurance liability covered by this critical accounting policy

was $290.4 million during 2006. Although we believe we have sufficient

current and historical information available to us to record reasonable

estimates for our self-insurance liability, it is possible that actual results

could differ. In order to help you assess the risk, if any, associated with

the uncertainties discussed above, a ten percent (10%) pre-tax change

in our estimate for our self-insurance liability, which we believe is a

reasonably likely change, would increase or decrease our self-insurance

liability by about $29.0 million during 2006.

We have not made any material changes in the accounting methodology

used to establish our self-insurance liability during the past three years.