Blackberry 2003 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2003 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56

|

|

50

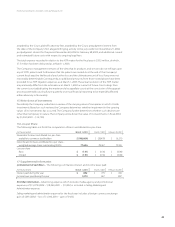

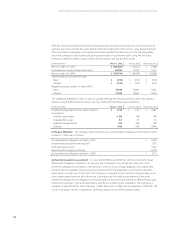

ResearchInMotionLimited|IncorporatedUndertheLawsofOntario(UnitedStatesdollars,inthousandsexceptpersharedataorasotherwiseindicated)

51

FortheyearsendedMarch1,2003,March2,2002andFebruary28,2001

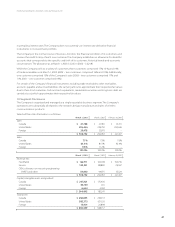

InJuly2002,theFASBissuedSFASNo.146,“AccountingforCostsAssociatedwithExitorDisposal

Activities,”whichrequirescompaniestorecognizecostsassociatedwithexitordisposalactivities

whentheyareincurredratherthanatthedateofacommitmenttoanexitordisposalplan.SFAS

No.146istobeappliedprospectivelytoexitordisposalactivitiesinitiatedafterDecember31,2002.

TherewasnoeffectontheadoptionofSFASNo.146ontheCompany’sresultsofoperationsand

nancialpositionfor2003andprioryears.

InNovember2002,theFASBissuedInterpretationNo.45“Guarantor’sAccountingandDisclosure

RequirementsforGuarantees,IncludingIndirectGuaranteesofIndebtednessofOthers”(“FIN45”),

whichrequirescertaindisclosuresofobligationsunderguarantees.Thedisclosurerequirementsof

FIN45areeffectivefortheCompany’syearendedMarch1,2003.Anadditionaldisclosurerequire-

mentunderFIN45relatestoproductwarrantyasdescribedinnote1and21(f).FIN45alsorequiresthe

recognitionofaliabilitybyaguarantorattheinceptionofcertainguaranteesenteredintoormodied

afterDecember31,2002,basedonthefairvalueoftheguarantee.Therewasnoeffectontheadoption

ofthemeasurementrequirementofFIN45ontheCompany’sresultsofoperationsandnancial

positionfor2003andprioryears.

TheEmergingIssuesTaskForcereachedaconsensusonIssue00-21,addressinghowtoaccountfor

arrangementsthatinvolvethedeliveryorperformanceofmultipleproducts,services,and/orrights

touseassets.Revenuearrangementswithmultipledeliverablesaredividedintoseparateunitsof

accountingifthedeliverablesinthearrangementmeetthefollowingcriteria:(a)thedelivereditemhas

valuetothecustomeronastandalonebasis;(b)thereisobjectiveandreliableevidenceofthefairvalue

ofundelivereditems;and(c)deliveryofanyundelivereditemisprobable.Arrangementconsideration

shouldbeallocatedamongtheseparateunitsofaccountingbasedontheirrelativefairvalues,with

theamountallocatedtothedelivereditembeinglimitedtotheamountthatisnotcontingentonthe

deliveryofadditionalitemsormeetingotherspeciedperformanceconditions.Thenalconsensus

willbeapplicabletoagreementsenteredintoinscalperiodsbeginningafterJune15,2003withearly

adoptionpermitted.TheCompanyiscurrentlyevaluatingtheimpactofadoptionontheconsolidated

nancialstatements.

InDecember2002,theFASBissuedSFASNo.148,“AccountingforStock-BasedCompensation–

TransitionandDisclosure,anamendmentofFASBStatementNo.123.”ThisStatementamendsFASB

StatementNo.123,“AccountingforStock-BasedCompensation,”toprovidealternativemethodsof

transitionforavoluntarychangetothefairvaluemethodofaccountingforstock-basedemployee

compensation.Inaddition,thisStatementamendsthedisclosurerequirementsofStatement

No.123torequireprominentdisclosuresinbothannualandinterimnancialstatements.Certain

ofthedisclosuremodicationsarerequiredforscalyearsendingafterDecember15,2002and

areincludedinthenotestotheseconsolidatednancialstatements.