Blackberry 2003 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2003 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

32

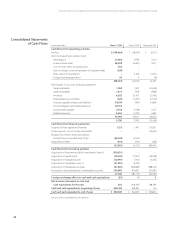

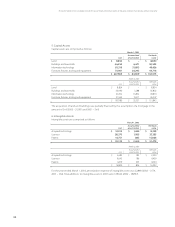

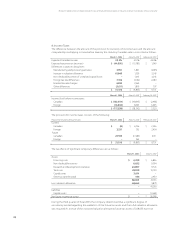

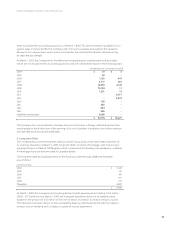

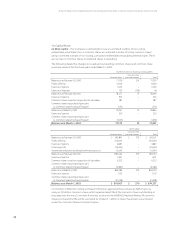

ResearchInMotionLimited|IncorporatedUndertheLawsofOntario(UnitedStatesdollars,inthousandsexceptpersharedataorasotherwiseindicated)

33

FortheyearsendedMarch1,2003,March2,2002andFebruary28,2001

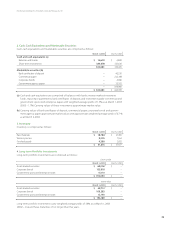

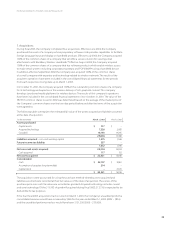

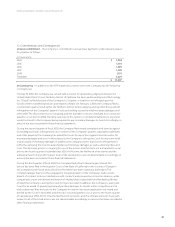

ServiceRevenueisrecognizedrateablyonamonthlybasiswhentheserviceisprovided.Ininstances

wheretheCompanybillsthecustomerpriortoperformingtheservice,theprepaymentisrecorded

asdeferredrevenue.

SoftwareRevenuefromlicensedsoftwareisrecognizedattheinceptionofthelicencetermandin

accordancewithSOP97-2.Revenuefromsoftwaremaintenance,unspeciedupgradesandtechnical

supportcontractsisrecognizedovertheperiodsuchitemsaredeliveredorservicesareprovided.

Technicalsupportcontractsextendingbeyondthecurrentperiodarerecordedasdeferredrevenue.

Non-recurringengineeringcontractsRevenueisrecognizedasspeciccontractmilestonesaremet.

Theattainmentofmilestonesapproximatesactualperformance.

(o)Researchanddevelopment–TheCompanyisengagedatalltimesinresearchanddevelop-

mentwork.Researchanddevelopmentcosts,otherthancapitalassetacquisitions,arechargedasan

operatingexpenseoftheCompanyasincurred,unlesstheymeetgenerallyacceptedaccounting

principlesfordeferral.

(p)Governmentassistance–Governmentassistancetowardsresearchanddevelopmentexpenditures

isreceivedasgrantsfromTechnologyPartnershipsCanadaandintheformofinvestmenttaxcredits

onaccountofeligiblescienticresearchandexperimentaldevelopmentexpenditures.Investmenttax

creditsarerecordedwhenthereisreasonableassurancethattheCompanywillrealizetheinvestment

taxcredits.Assistancerelatedtotheacquisitionofcapitalassetsusedforresearchanddevelopment

iscreditedagainstthecostoftherelatedcapitalassetsandallotherassistanceiscreditedagainst

relatedexpenses,asincurred.

(q)Losspershare–Losspershareiscalculatedbasedontheweightedaveragenumberofshares

outstandingduringtheyear.Thetreasurystockmethodisusedforthecalculationofthedilutive

effectofstockoptionsandcommonsharepurchasewarrants.

(r)Stock-basedcompensationplan–TheCompanyhasastock-basedcompensationplan,which

isdescribedinnote10(b).Theoptionsaregrantedatthefairmarketvalueofthesharesonthe

dayofgrantoftheoptions.Nocompensationexpenseisrecognizedwhenstockoptionsareissued

toemployees.Anyconsiderationpaidbyemployeesonexerciseofstockoptionsiscredited

tosharecapital.

InNovember2001,theCICAissuedHandbookSection3870,StockBasedCompensationandOther

StockBasedPayments.Thisstandardrequiresthatcertaintypesofstock-basedcompensation

arrangementsbeaccountedforatfairvalue,givingrisetocompensationexpense,forgrantsawarded

inscalyearsbeginningonorafterJanuary1,2002.TheCompanyadoptedthisstandardinscal2003

withnoimpacttoretainedearnings.

(s)Warranty–TheCompanyestimatesitswarrantycostsatthetimeofrevenuerecognitionbased

onhistoricalwarrantyclaimsexperienceandrecordstheexpenseinCostofsales.Thewarrantyaccrual

balanceisreviewedquarterlytoassessthatitmateriallyreectstheremainingobligationbasedon

theanticipatedfutureexpendituresoverthebalanceoftheobligationperiod.Adjustmentsaremade

whentheactualwarrantyclaimexperiencediffersfromestimates.