Avon 2006 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2006 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

2005. During 2006, we increased sequentially the purchases

under our program as we have been accelerating the pace of our

repurchase program.

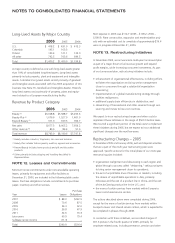

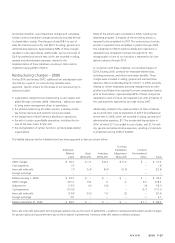

NOTE 10. Employee Benefit Plans

Savings Plan

We offer a qualified defined contribution plan for U.S.-based

employees, the Avon Personal Savings Account Plan, which

allows eligible participants to contribute up to 25% of eligible

compensation through payroll deductions. Prior to February

2005, we matched employee contributions dollar for dollar up to

the first 3% of eligible compensation and fifty cents for each

dollar contributed from 4% to 6% of eligible compensation. In

February 2005, Avon temporarily suspended the matching con-

tribution. The matching contributions were resumed in 2006 at

the pre-February 2005 levels. In 2006, 2005, and 2004, match-

ing contributions approximating $12.7, $1.8 and $14.6,

respectively, were made to this plan in cash, which were then

used by the plan to purchase Avon shares in the open market.

Defined Benefit Pension and

Postretirement Plans

Avon and certain subsidiaries have contributory and non-

contributory retirement plans for substantially all employees of

those subsidiaries. Benefits under these plans are generally based

on an employee's years of service and average compensation

near retirement. Plans are funded based on legal requirements

and cash flow.

We provide health care and life insurance benefits for the

majority of employees who retire under our retirement plans in

the United States and certain foreign countries. In the U.S., the

cost of such health care benefits is shared by us and our retirees

for employees hired on or before January 1, 2005. Employees

hired after January 1, 2005, pay the full cost of the health care

benefits.

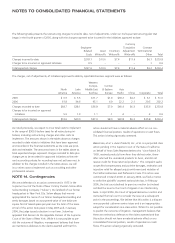

In September 2006, the FASB issued SFAS No. 158, Employers’

Accounting for Defined Benefit Pension and Other Postretire-

ment Plans – an amendment of FASB Statements No. 87, 88,

106 and 132R (“SFAS 158”). SFAS 158 requires, among other

things, the recognition of the funded status of pension and

other postretirement benefit plans on the balance sheet. Each

overfunded plan is recognized as an asset and each underfunded

plan is recognized as a liability. The initial impact of the stan-

dard, due to unrecognized prior service costs or credits and net

actuarial gains or losses, as well as subsequent changes in the

funded status, are recognized as components of accumulated

comprehensive loss in shareholders’ equity. Additional minimum

pension liabilities and related intangible assets were also

derecognized upon adoption of the new standard.

We adopted SFAS 158 as of December 31, 2006. The adoption

of SFAS 158 had no impact on our Consolidated Statement of

Income for the year ended December 31, 2006, or for any prior

period presented, and it will not effect our operating results in

future periods. SFAS 158’s provisions regarding the change in

the measurement date of defined benefit and other postretire-

ment plans had no impact as we were already using a measure-

ment date of December 31 for our pension plans. The following

table summarizes the impact of the initial adoption of SFAS 158:

Effect of Adopting

SFAS 158 at

December 31, 2006

Prior to

SFAS

158 (1)

Effect of

Adoption of

SFAS 158

Increase

(Decrease)

After

Adopting

SFAS 158

Other assets $ 448.8 $(232.8) $ 216.0

Accrued compensation – 35.5 35.5

Employee benefit plans

liability 455.5 (13.4) 442.1

Accumulated other

comprehensive loss, net

of taxes (145.3) (254.7) (400.0)

(1) Includes effects of additional minimum liability that would have been

recognized at December 31, 2006, had we not been required to adopt

SFAS 158.

A V O N 2006 F-19