Avon 2006 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2006 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

PART II

sales returns have been in the range of $285.0 to $295.0, or

approximately 3.5% of total revenue. If the historical data we

use to calculate these estimates does not approximate future

returns, due to changes in marketing or promotional strategies,

or for other reasons, additional allowances may be required.

Provisions for Inventory Obsolescence

We record an allowance for estimated obsolescence equal to the

difference between the cost of inventory and the estimated

market value. In determining the allowance for estimated obso-

lescence, we classify inventory into various categories based

upon its stage in the product life cycle, future marketing sales

plans and the disposition process. We assign a degree of obso-

lescence risk to products based on this classification to determine

the level of obsolescence provision. If actual sales are less favor-

able than those projected by management, additional inventory

allowances may need to be recorded for such additional obso-

lescence. Annual obsolescence expense was $173.3, $83.9 and

$76.7 for the years ended December 31, 2006, 2005 and 2004,

respectively. As discussed in the Overview section, 2006 includes

inventory obsolescence charges of $72.6 related to our PLS pro-

gram and $20.5 related to our decision to discontinue the sale of

heavily discounted excess products.

Pension, Postretirement and

Postemployment Benefit Expense

We maintain defined benefit pension plans, which cover sub-

stantially all employees in the U.S. and in certain international

locations. Additionally, we have unfunded supplemental pension

benefit plans for certain current and retired executives (see Note

10, Employee Benefit Plans).

Our calculations of pension, postretirement and postemployment

costs are dependent upon the use of assumptions, including

discount rates, expected return on plan assets, interest cost,

health care cost trend rates, benefits earned, mortality rates, the

number of associate retirements, the number of associates elect-

ing to take lump-sum payments and other factors. Actual results

that differ from assumptions are accumulated and amortized to

expense over future periods and, therefore, generally affect

recognized expense in future periods. At December 31, 2006,

we had actuarial losses of $412.1 and $227.8 for the U.S. and

non-U.S. plans, respectively, that have not yet been charged to

expense. These actuarial losses have been charged to accumu-

lated other comprehensive loss within equity in accordance with

SFAS 158, which was adopted December 31, 2006. While we

believe that the assumptions used are reasonable, differences in

actual experience or changes in assumptions may materially

affect our pension, postretirement and postemployment obliga-

tions and future expense.

For 2006, the weighted average assumed rate of return on all

pension plan assets, including the U.S. and non-U.S. plans was

7.6%. In determining the long-term rates of return, we consider

the nature of the plans’ investments, an expectation for the

plans’ investment strategies, historical rates of return and current

economic forecasts. We evaluate the expected long-term rate of

return annually and adjust as necessary.

The majority of our pension plan assets relate to the U.S. pension

plan. The assumed rate of return for 2006 for the U.S. plan was

8.0%, which was based on an asset allocation of approximately

35% in corporate and government bonds and mortgage-backed

securities (which are expected to earn approximately 5% to 7%

in the long term) and 65% in equity securities (which are

expected to earn approximately 8% to 10% in the long term).

Historical rates of return on the assets of the U.S. plan for the

most recent 10-year and 20-year periods were 7.6% and 9.7%,

respectively. In the U.S. plan, our asset allocation policy has

favored U.S. equity securities, which have returned 8.0% and

11.8%, respectively, over the 10-year and 20-year periods. The

actual rate of return on plan assets in the U.S. was approximately

13.1% and 5.5% in 2006 and 2005, respectively.

The discount rate used for determining future pension obliga-

tions for each individual plan is based on a review of long-term

bonds that receive a high-quality rating from a recognized rating

agency. The discount rates for our more significant plans, includ-

ing our U.S. plan, were based on the internal rates of return for

a portfolio of high quality bonds with maturities that are con-

sistent with the projected future benefit payment obligations of

each plan. The weighted-average discount rate for U.S. and

non-U.S. plans determined on this basis was 5.43% at

December 31, 2006, and 5.2% at December 31, 2005.

Future effects of pension plans on our operating results will

depend on economic conditions, employee demographics,

mortality rates, the number of associates electing to take

lump-sum payments, investment performance and funding deci-

sions, among other factors. However, given current assumptions

(including those noted above), 2007 pension expense related to

the U.S. plan is expected to increase in the range of $3.0 to $5.0.

A 50 basis point change (in either direction) in the expected rate

of return on plan assets, the discount rate or the rate of

compensation increases, would have had the following effect on

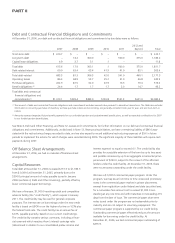

2006 pension expense:

Increase/(Decrease) in

Pension Expense

50 basis point

Increase

50 basis point

Decrease

Rate of return on

assets $ (5.5) $ 5.5

Discount rate (11.2) 11.6

Rate of compensation

increase 3.8 (3.7)